Balance of Payments: Despite a slight deterioration, Hungary’s external position remained sustainable

Related content

The earnings season is picking up speed in Europe as well

Next week, the second quarter earnings season will continue in full swing: In the US, market participants will likely focus primarily on the latest figures from major technology companies, while in Europe, several banks and several automaker companies will also report. As for Hungarian blue-chip companies, Magyar Telekom and OTP will publish their second quarter earnings on August 5, followed by Mol and Richter on August 7.

Commodities - Technical Analysis

Gold and silver have begun a minor correction; however, no far-reaching conclusions can be drawn from this movement at this time, as there has not yet been a significant change in the trend structure. The price of oil has reached the 87.5 target price, which is a key watershed level; a breakout above this level could result in a shift in the price range. Natural gas broke below the important upward trendline two weeks ago, though no significant selling pressure has been observed so far. Copper has been showing a strong upward trend since the recent long signal. Wheat’s uptrend also remains intact, and there is still some room before reaching the next key resistance level. Corn prices have also broken out of their downtrend, paving the way for a new swing high to form.

Hungary’s external position remained sustainable in Q4 and in full year 2025, despite a slight deterioration. The C/A surplus moderated from around 2% of GDP to 1.6% in 2025 and to 1.1% in Q4 as exports remained under pressure and machinery imports rose. As EU fund inflow was subdued (0.5% of GDP) and the NEO remained deeply negative (-2.5%), the net financing capacity (including NEO) turned modestly negative (-0.5 / -1% of GDP). With positive FDI and outflows in portfolio equities, the economy accumulated external debt in net terms in both Q4 and 2025 (1.6% of GDP). External debt ratios followed stagnating or slightly declining trends; gross external debt remained below 65% of GDP, in line with the regional average. FX reserves rose significantly, exceeding the adequate level by EUR 15-20 bn.

Looking ahead, higher energy prices will be a drag again on the external position. In our baseline, we expect the C/A balance to remain above zero (0.7% of GDP), but net external financing capacity remains negative. Hungary’s external debt indicators could stagnate, looking ahead. Risks tilted to the downside, due to the uncertainty around the duration and the scale of the new energy price shock. Should oil and gas prices remain at current levels, the C/A balance may reach a deficit this year and next. Nevertheless, FX reserves reached really high levels by now, so the MNB’s room for manoeuvre to mitigate the effects of external shocks on the exchange rate has increased notably.

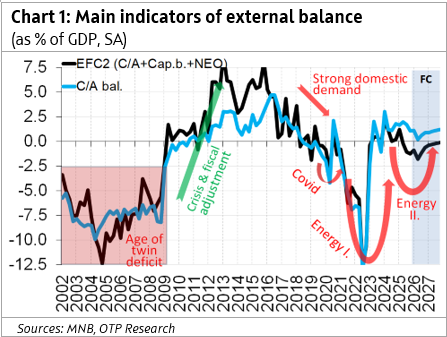

Indicators of external balance: ?The current account surplus moderated to around 1% of GDP, while the external financing capacity deteriorated to -1% (Charts 1—4)

· Current account balance deteriorated from 2% of GDP to 1%: In Q4 2025, Hungary's current account balance reached EUR +0.3 bn, exceeding the preliminary data of 0; however, it fell behind the Q4 2024 figure of EUR 0.9 bn. In seasonally adjusted terms, the surplus was EUR 0.6 bn, or 1.1% of GDP, which is a slight deterioration compared to the recent figures just below of 2% of GDP. In 2025 as a whole, the C/A balance had a surplus of EUR 3.5 bn (1.6% of GDP), in line with the 2024 figure. In Q4, the deterioration was driven by the balance of goods, more precisely machinery and transport equipment, where after a longer period of contraction, exports started to pick up, but not as fast as imports. This could be an early sign of recovery (rising demand for inputs) or might be related to ongoing big-ticket investments (like BMW, BYD, or CATL). From a sectoral saving perspective, however, the picture is less rosy, as the deterioration was mainly the consequence of lower household savings (Chart 2).

· EFC1: between 2-3% of GDP. Hungary’s external financing capacity (the sum of the current account and the capital balance) fell to 1.7% of GDP in Q4, due to the deterioration of the current account from the 2-2.5% range of recent quarters. The surplus of the capital balance has been fluctuating around 0.5% of GDP since 2022, while it reached 2% of GDP before.

· EFC2: in a slightly negative territory. (EFC2 = EFC1 plus net errors and omissions). The net financing capacity, which we consider the best and most stable indicator of external imbalances, fell to -1% in Q3 and Q4 from around +0.5 / +1% of GDP, so the annual figure was also negative in 2025 (EUR -1 bn, or -0.4% of GDP; 2024: +0.6%). As usual, the NEO remained deeply negative (-2%/-2.5% % of GDP). The negative NEO could be the consequence of hidden imports through online retail trade and/or capital outflows under the radar (most likely the latter in recent years).

Capital flows: FDI remained modestly positive, the incurrence of foreign debt was modestly positive.

· Net FDI inflow was slightly positive both in Q4 (EUR 0.7bn) and in 2025 (EUR 1.1 bn 2024: 0), as corporate FDI exceeded 1.3% of GDP, and it was negative in the finance sector. Portfolio equities registered capital withdrawals (1.7% of GDP in 2025), so non-debt generating inflows were negative.

· As the economy as a whole had negative net financing capacity and non-debt generating inflows were negative, the Hungarian economy accumulated foreign debt both in Q4 (EUR 2.2 bn) and in 2025 (EUR 3.5bn or 1.6% of GDP).

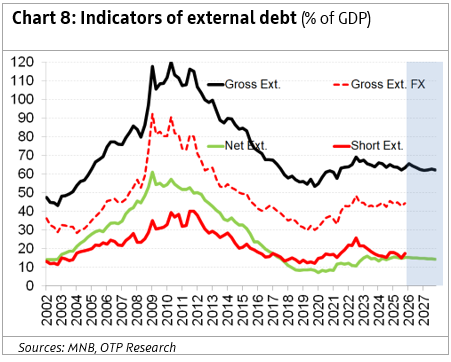

Indebtedness and reserves: unchanged stagnating/slightly decreasing patterns in debt ratios, while FX reserves finally soared well above the adequate levels

·First, we emphasise that we use the BoP and external debt figures without SPVs. In our view, the figures that contain special-purpose vehicles are heavily distorted by entities that do not have much to do with the Hungarian economy. Therefore we rely on data cleaned from SPVs, as these data are much more consistent with the Hungarian macro-trajectory, and give us reliable information on indebtedness and vulnerability. We also filter out intercompany loans, which we consider to be more FDI-like than debt.

· Indicators of external indebtedness have been stagnating, or very slightly decreasing, for a while. Net external debt stagnates just below 15% of GDP, gross external debt fell to 62%, the lowest level in four years, after topping out near 70% of GDP in 2022. Gross external FX debt has been fluctuating around 45% of GDP and short-term external debt between 15% and 20% for many quarters.

· Hungary's FX reserves soared to EUR 50 billion in Q4 (or 22% of GDP) and to EUR 60 bn in February. This means that FX reserves exceed the level suggested by the reserve adequacy rules by EUR 15-20 bn, providing a comfortable room for the national bank to be active on the FX market, if needed.

Outlook:

· With the war in Iran, the outlook turns out to be more challenging. Higher energy prices mean higher energy import bill for Hungary. A 10 USD/barrel increase in oil prices would increase the energy bill by 0.2% of GDP, while a 10 EUR/MWh rise in gas prices has an effect of 0.5% (of GDP), which is expected to be mitigated somewhat by price hedges of the MVM (the energy company) and lower consumption.

· In our baseline scenario (assuming an average oil price of 80 USD/barrel and gas prices of 44 EUR/MWh), we expect the external position to deteriorate by -0.6 ppts (of GDP) in the remaining part of the year, so the C/A balance would remain in a small surplus of 0.7% of GDP in 2026, and bounce back to around 1% in 2027. The net financing capacity could reach -1% of GDP this year and improve to around -0.2% in 2027. We expect FDI inflow to remain slightly positive, so foreign debt accumulation could be modest and external debt ratios could remain on their stagnating trajectory.

· Risks are tilted to the downside due to the uncertainty around the scale and duration of the energy price shock. Should prices remain on their current level (oil: 110 USD, gas: 54 EUR), the deterioration would reach 1.5 ppts this year and 2ppts in 2027, pushing the C/A balance into the slightly negative territory. But the scale of the shock is expected to remain well below the crisis in 2021/2022. And there is a significant difference between the crisis in 2022 and the current situation: in 2022 FX reserves just reached the adequate level, now they exceed it by EUR 15-20 bn.

· There is an additional risk, a positive one, related to the parliamentary elections. Historical patterns suggest that after elections, fiscal policy is usually adjusted, which could result in a lower fiscal and a better external position, in 2027 the latest.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more