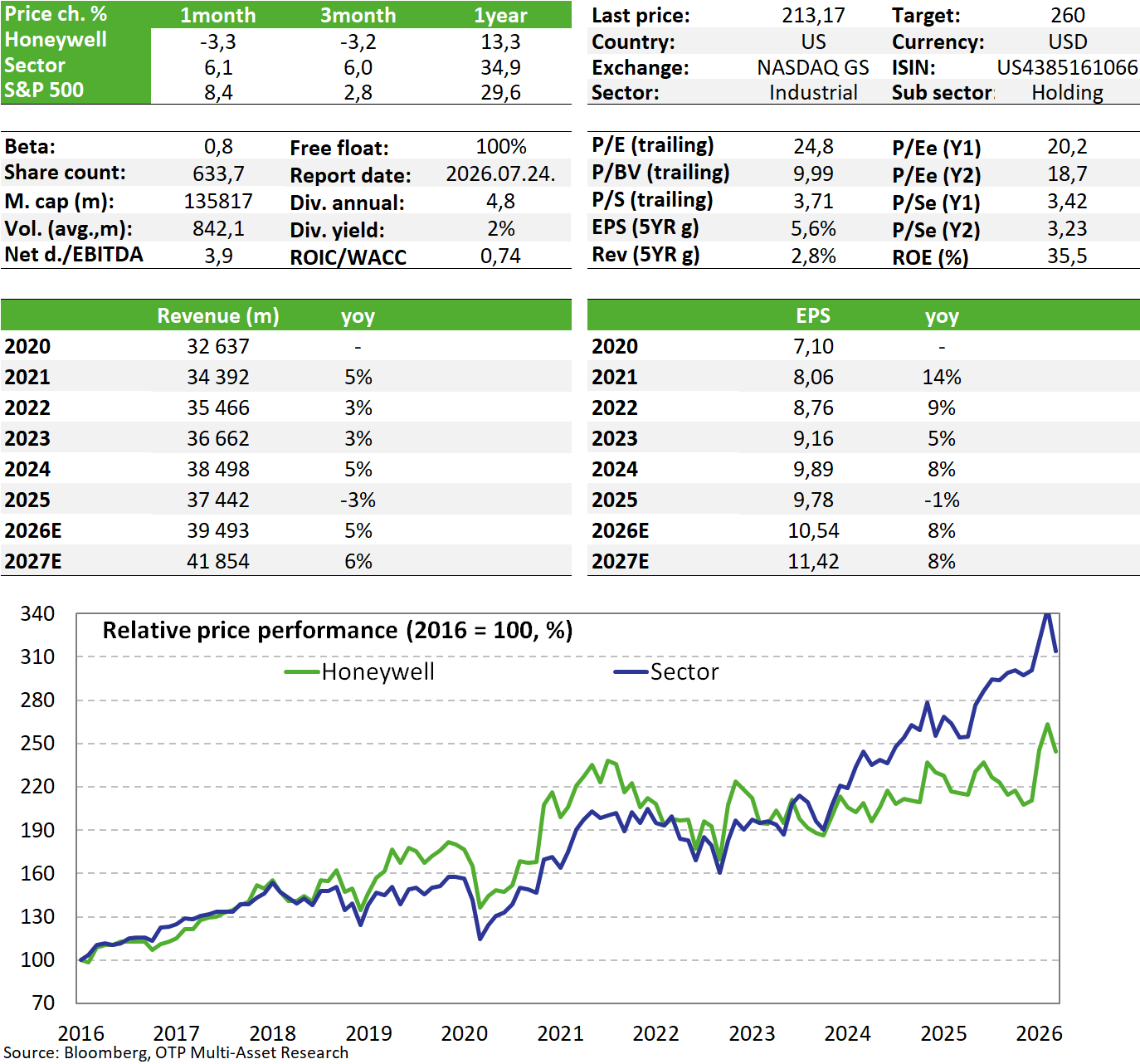

Honeywell: The spin-off is proceeding smoothly

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

Honeywell reported a slightly negative first-quarter flash report overall compared to expectations, with the negative effects of the war in the Middle East also playing a role. Since this will result in further revenue losses in the second quarter as well, the company may continue to face some headwinds in the short term. However, as the situation stabilizes, these postponed purchases could quickly return, a trend already evident in rising order backlogs; consequently, management has not revised its full-year forecasts. The spin-offs driving the primary investment thesis are progressing well; asset sales took place during the quarter, and the spin-off of the Aerospace division could occur as early as the end of June, ahead of the previously planned schedule. For all these reasons, we maintain our positive view and our previous fair value estimate of $260 per share.

Quarterly report

The company failed to meet first-quarter revenue expectations; the $9.14 billion figure represents organic growth of just 2.4% year-over-year, compared to the consensus estimate of $9.3 billion. A factor contributing to the shortfall was the negative 0.5% impact on revenue in the process automation and technology segment (solutions focused on the energy industry) due to the war in the Middle East and the company’s business exposure there; however, even excluding this, there would still be a slight shortfall. In terms of profit, however, the company delivered a positive surprise, reporting EPS of $2.45 compared to the expected $2.34.

The process automation segment saw the sharpest decline in organic growth, at 6%, largely due to the situation in the Middle East, which has caused delays in both refinery catalyst shipments and automation services. Overall, however, revenue managed to remain stable, partly due to increased demand from U.S. LNG projects, which was partly related to the situation. Although the problems in the Middle East may still have a temporary negative impact, the company believes that once they are resolved, deferred demand could begin to drive growth, as the order backlog continued to grow by 3% during the quarter.

In the building automation segment, revenue grew by a healthy 8% organically, while the order backlog increased by 9%, driven in part by data center developments (primarily in the U.S.). In contrast, the industrial automation segment posted modest revenue growth; moreover, in April the company announced the sale of the PSS and WSS units classified under this segment, meaning that the weight of this segment will decrease.

Revenue in the aerospace technologies segment also came in lower than the expected $4.54 billion, at $4.32 billion (3% organic growth year-over-year), which the company attributes in part to temporary supply chain issues affecting January and February. Defense and aerospace orders performed well, and commercial aircraft orders also increased. The spin-off of the division is progressing faster than the original schedule; the company aims to achieve this important milestone by the end of June, ahead of the previously indicated third-quarter timeline.

Write-downs related to the sale of the PSS and WSS segments also contributed to the 14% year-over-year decline in operating profit. As a result, segment margins fell by 320 basis points; however, excluding this impact, we would see a 90-basis-point increase due to improving pricing power. This duality is also evident in the net profit line: EPS fell by 35%, but excluding one-time items, the adjusted figure rose by 11% (which is what the market is focusing on). Free cash flow also declined, though the increase in accounts receivable due to tensions in the Middle East also played a role in this.

Other events

Although it is important for the company to deliver consistently good performance (which, in our view, it did in the quarter), as we discuss below, from an investor perspective, the ongoing separation of the company's segments represents the most significant potential. This process is progressing according to the announced schedule:

- On October 30, ahead of the previously announced deadline of late 2025 to early 2026, the chemical and materials segment, Solstice Advanced Materials, was spun off and listed on the stock exchange. All of Solstice's common shares were received by Honeywell's owners, who received one new Solstice share for every four shares they held, the price of which rose by around 60% after the listing. This was the smaller part of the company's spin-off, with the separation of the aerospace segment, which promises to release significant value, due to take place this year.

- Based on the updated milestones, the next step in the spin-off of the segments—namely, the separation of the larger aerospace division—will take place slightly earlier than previously indicated, by the end of June 2026 (this is an earlier date than the third quarter previously indicated). The new entity will be named Honeywell Aerospace, and Jim Currie, who currently leads the segment, will continue to head it; appointments have already been made to several key management positions. However, three new segments will be created for the remaining automation-related units, and reporting will be done accordingly from the beginning of 2026: Building Automation, Process Automation & Technology, and Industrial Automation.

- In April, the company announced that it would sell its Productivity Solutions and Services (PSS) unit to Brady Corp in a $1.4 billion cash transaction. PSS, which is expected to generate approximately $1.1 billion in revenue in 2025, is a leading provider of mobile computers, barcode scanners, and printing solutions for the warehousing and logistics market. In addition, the company is selling its Workflow Solutions division to a private equity firm (for an undisclosed price), with these transactions set to close in the second half of the year. This cash inflow could help the company finance its planned $1.8 billion acquisition of Johnson Matthey (which develops catalysts and technologies for the chemical industry) in August.

- Quantinuum, a quantum computing company in which the firm holds a majority stake (which develops quantum computers and offers not only hardware but also software and middleware), successfully raised $600 million in funding last September, with Nvidia now among its investors. In mid-January, the company began preparing for Quantinuum’s initial public offering (IPO); the details (price, number of shares) remain unknown for now. For investors, the market entry was partly expected, though in terms of timing, it was anticipated to occur later, in 2027, which could have a slightly positive impact on the stock, as it could further reinforce the potential inherent in the revaluation effect expected from the spin-offs. Quantinuum, which is currently operating at a loss and is likely to have a negative impact on Honeywell’s ultimate enterprise value, was valued at $10 billion in the most recent funding round—a significant amount (~7%) even relative to Honeywell’s market capitalization.

Valuation

Compared to its peers, there appears to be a slight discount on a P/E (~20) and EV/EBITDA (~15) basis (although it is difficult to find suitable peers due to its large industrial conglomerate nature). Although risks surrounding the stock have increased in the short term, the longer-term outlook remains positive, and the spin-off is proceeding smoothly for now, which could unlock value for shareholders; therefore, we maintain our previous fair value estimate of $260.

Investment story

- Honeywell is an industrial conglomerate whose key segments are automation (building, industrial, process and technology) and aerospace, which account for roughly half of its revenue each. The company primarily secures U.S. defense contracts through its aerospace division, which accounts for approximately 10% of revenue; North America accounts for 52% of sales, while Europe accounts for 18%.

- Honeywell plans to focus on high-growth regions (Latin America, Asia, Africa, India, and Central and Eastern Europe) and innovation in the future, while selling off its non-core assets to streamline operations, in addition to making targeted acquisitions (e.g., Johnson Metthey).

- In order to divest assets that did not align with the company’s strategy, the spin-off of Advanced Materials, a chemical and raw materials manufacturer, was announced in October, followed by the sale of its PSS and WSS units this year. In addition, the two key business segments—aerospace and automation—are expected to be spun off in 2026, a move also recommended by the well-known activist investor Elliott Investment to unlock value for shareholders (according to them, the spin-off could also have significant upside potential for the stock price).

- The structure will be simplified; all three spin-off companies are market leaders in their respective sectors, and their independence could lead to more flexible operational and financial options, better capital allocation decisions, and a faster ability to respond.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more