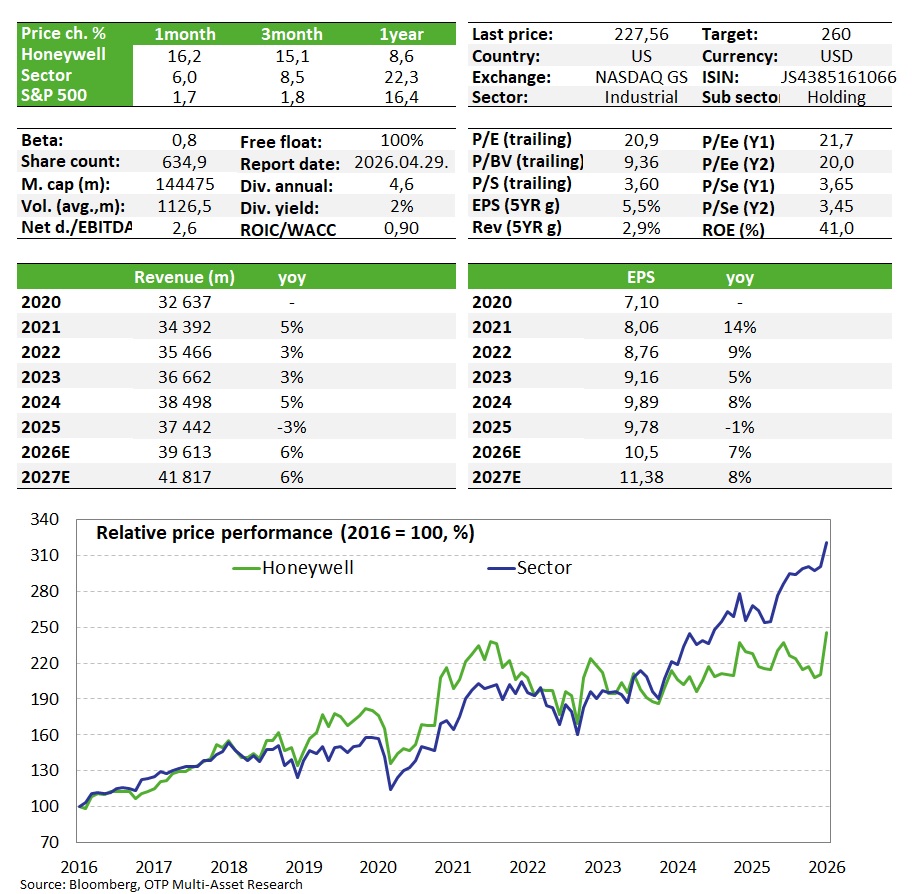

Honeywell: strong year-end results, encouraging outlook

Related content

Honeywell's stock price may be on the verge of a breakout

Major indices began to fall at the end of last week, but the movements were news-driven, and there has been significant volatility, which has resulted in a low number of opportunities indicating a quality breakout for the past two weeks. This week, one of the stocks from our Equity Top Pick List, Honeywell, also ranked high on the momentum list. After a minor pullback, the technical picture could indeed be supportive.

Uber Falls on Negative News

Uber shares failed to follow through on their breakout attempt, and on Friday, negative news concerning the company’s robotaxi business pushed the share price down to the stop-loss level specified in our trading idea.

Honeywell ended 2025 with a stronger-than-expected quarter, and with its order backlog growing nicely, this sets the stage for continued growth this year. With underlying fundamentals looking encouraging, investors' focus may increasingly turn to the pending breakup, planned for the third quarter (further details on the June investor days), which could further help the re-rating of the shares that we expect to continue (as the spin offs are likely to unlock value). Due to the more favorable earnings figures and strong outlook, we are raising our previous fair value estimate of $248 to $260, while maintaining our optimistic view, and keep the stocks on our Equity Top Pick List.

Quarterly report

The company generated nearly $10 billion in revenue in the fourth quarter, representing 11% organic growth year-on-year, slightly exceeding both the analyst consensus (+8.4%) and the upper end of management's updated December expectations (USD 9.8-10 billion and 8-10% growth). Growth was also impressive in the order backlog, which grew by 23% to USD 37 billion, laying a solid foundation for further growth in 2026.

At the segment level, Aerospace Technologies were the biggest driver of growth, with organic growth of 21%, but the impact of the previous Bombardier agreement is also included as a major one-off driver (which also increased margins, resulting in significant growth on the profit side). Even excluding this, growth was 11%, supported by strong performance in both the commercial aircraft division and the defense and space division. The order backlog in this segment has also grown significantly. Orders are similarly strong in the Energy and Sustainability Solutions segment, which will be necessary, as this was the only segment in the fourth quarter where revenue declined by around 7%, mainly due to weaknesses in the chemical industry segment. Industrial Automation increased revenue by 4%, while the Building Automation segment increased revenue by 8%, with margins also expanding in the latter, which translated into profit growth.

Adjusted EPS rose by 17%, although margins declined, excluding the Bombardier project, resulting in a 3% decline in adjusted profit. However, the $2.59 level is still above market expectations of $2.54. However, this did not have such a negative impact on free cash flow, which grew by 48%, but even excluding the one-off project, this line item grew by 13% to $2.5 billion (well above the expected $1.35 billion). In 2025, free cash flow totaled $5.1 billion, of which $6.8 billion was returned to shareholders in the form of dividends and share buybacks, representing a total payout yield of 4.8%.

Management's expectations for 2026 have also been announced, which continue to assume stable, strong figures, supported by high order backlogs. Revenue could grow organically by 3-6%, with the driving force coming from the aerospace division, where orders have grown significantly and demand is strong from both the commercial and defense sectors. In addition, growth may continue in the building automation segment, driven by AI data centers in healthcare and hospitality in several regions. Overall, management is forecasting a 20-60 basis point increase in segment margins (to 22.7-23.1%), primarily due to the two high-demand segments mentioned above, which could bring 6-9% growth in EPS, with free cash flow generation of USD 5.3-5.6 billion. Management's expectations for the main lines are in line with market consensus.

Other events

Although it is important for the company to deliver consistently good performance (which, in our view, it did in the quarter), as we discuss below, from an investor perspective, the ongoing separation of the company's segments represents the most significant potential. This process is progressing according to the announced schedule:

- On October 30, ahead of the previously announced deadline of late 2025 to early 2026, the chemical and materials segment, Solstice Advanced Materials, was spun off and listed on the stock exchange. All of Solstice's common shares were received by Honeywell's owners, who received one new Solstice share for every four shares they held, the price of which rose by around 30% after the listing. This was the smaller part of the company's spin-off, with the separation of the aerospace segment, which promises to release significant value, due to take place this year.

- Based on the updated milestones, the next step in the separation of the segments, namely the spin-off of the larger aerospace division, will take place somewhat earlier than previously indicated, in the third quarter of 2026 under the name Honeywell Aerospace, with Jim Currie, who currently heads the segment, continuing in his role, and appointments already made in several key management positions. However, three new segments will be created for the remaining automation-related units, and reporting will be done accordingly from the beginning of 2026: Building Automation, Process Automation & Technology, and Industrial Automation.

- Quantinuum, a quantum computing company majority-owned by the company (which develops quantum computers and offers not only hardware but also software and middleware), successfully raised $600 million in capital in September, with Nvidia among its investors. In mid-January, the company began preparations for Quantinuum's IPO, although the parameters (price, number of shares) are not yet known. For investors, the market entry was partly expected, although in terms of timing, it was expected to be later, in 2027, which could have a slightly positive effect on the stock, as it could further strengthen the potential for revaluation expected from the spin-offs. Quantinuum, which is currently loss-making at the operational level and is likely to have a negative impact on Honeywell's final enterprise value, could reach a market value of around USD 10 billion based on the market value of its peer IonQ, which is a significant amount (~7%) compared to Honeywell's market capitalization of USD 145 billion.

Valuation

Compared to its peers, there appears to be a slight discount on a P/E (~21) and EV/EBITDA (~15) basis (although it is difficult to find suitable peers due to its large industrial conglomerate nature). Due to the slightly higher pricing multiples, and better than expected quarterly performance, we are raising our previous fair value estimate of $248 (based on multiples) to $260.

Investment story

- Honeywell is an industrial conglomerate with key segments in automation (43% of revenue), aerospace (40%), and energy transition (17%). The company primarily has US military orders through its aerospace business, which accounts for ~10% of revenue, with North America accounting for 52% of sales and Europe for 18%.

- Honeywell will focus on higher-growth regions (Latin America, Asia, Africa, India, CEE) and innovation in the future, while selling off non-core assets for simplification purposes, in addition to targeted acquisitions (last March, they bought Sundyne, a company operating in the sustainable energy segment, for USD 2.2 billion).

- In order to separate elements that do not fit into the corporate strategy, the spin-off of Advanced Materials, a chemical and raw materials manufacturer, was announced in October. In addition, the two key business segments, aerospace is expected to be spun off in the third quarter of 2026, as recommended by renowned activist investor Elliott Investment, in order to unlock value (according to them, the spin-off could have a 50% to 75% upside potential).

- The structure will be simplified, with all three spin-off companies playing a leading role in their respective markets, and their independence could mean more flexible operational and financial opportunities, better capital allocation decisions, and faster response times. The transactions are expected to be completed in the second half of 2026.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more