Glencore: performance may improve despite the war

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

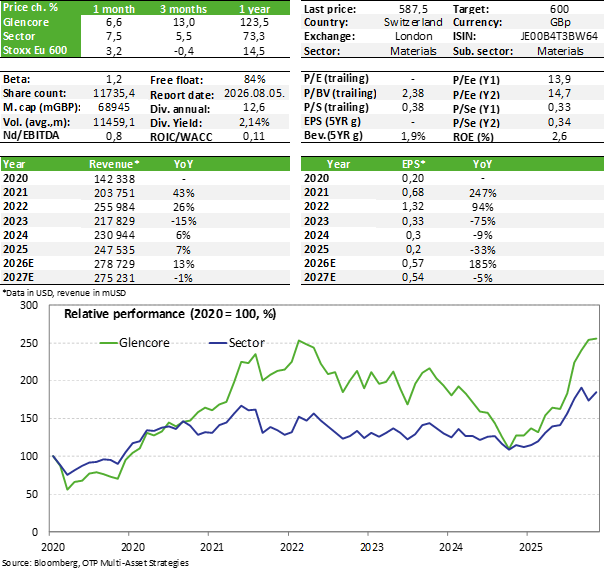

Glencore, one of the world’s largest diversified mining companies, recently released its Q1 production report, which was in line with expectations. In light of this, management reaffirmed its previously published production targets for 2026. The company was less affected by supply chain disruptions caused by the war in the Middle East, as it also has a significant trading and logistics division. With relatively high commodity prices and favorable trading activity, even an expansion of margins is conceivable, while the outlook for the coal market is also improving. For now, we are keeping Glencore shares on our Equity Top Pick List and have moderately raised our price target.

Quarterly production report

Regarding the conflict in the Middle East, the company emphasized that its trading and logistics division (marketing) ensured the fuel supply for its mining assets. They also noted that Glencore holds a net long position in sulfuric acid supply, which is important because more than 40% of the global sulfur supply passes through the Strait of Hormuz, where shipping traffic has fallen to a fraction of its previous levels since late February (sulfuric acid is used extensively in mining and fertilizer production, among other sectors). These are important factors for maintaining uninterrupted production, but regardless, production costs are expected to rise as energy and raw material prices have also increased (e.g., diesel, sulfuric acid). However, according to management, this can be more than offset by persistently high commodity prices (e.g., copper, zinc, and coal), so margins may even expand. Furthermore, the EBIT of Glencore’s trading division is also expected to be strong, potentially exceeding the upper limit of the long-term average annual range of $2.3–2.5 billion.

In terms of segment performance, copper production in Q1 was approximately 200,000 tons, up 19% year-over-year. Zinc production, however, fell by 17% to 177,000 tons (this decline was already anticipated in previous guidances, so it comes as no surprise). This is primarily because one of the company’s mines reached the end of its useful life, resulting in the termination of production there (Lady Loretta, Australia). Regarding coal production, coking coal output was 22% lower year-over-year, but the second half of the year is expected to be stronger, while thermal coal volumes remained flat.

Looking at the full-year forecasts, copper production is expected to be 810,000–870,000 tons (852,000 tons in 2025), zinc production 700,000–740,000 tons (970,000 tons in 2025), coking coal production at 30–34 million tons (32.5 million tons in 2025), while thermal coal production could reach 95–100 million tons (98 million tons in 2025). A significant decline is therefore expected only in zinc production, which, however, was already a known factor previously.

It is also worth noting that gold production totaled 68,000 ounces, down 53% year-over-year, while silver production reached 4.87 million ounces (+15% year-over-year). The decline in gold production is primarily due to a decline in ore quality, with most of Glencore’s production (through its subsidiary Kazzinc) taking place in Kazakhstan.

Valuation

In terms of valuation, Glencore still cannot be considered expensive as based on the expected EPS for 2026, the P/E ratio stands at 13.9x, while for 2027 it is 14.7x. Similarly, the valuation does not appear high on an EV/EBITDA basis (6.3x for 2026, 6.34x for 2027). Furthermore, the outlook remains favorable, primarily regarding the coal market. In the longer term, the copper sector also appears strong, although in the shorter term there are uncertainties on the demand side due to the war in Iran. We are therefore raising our target price slightly from 550 pence to 600 pence (6 British pounds) and are keeping the stock on our Equity Top Pick List.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more