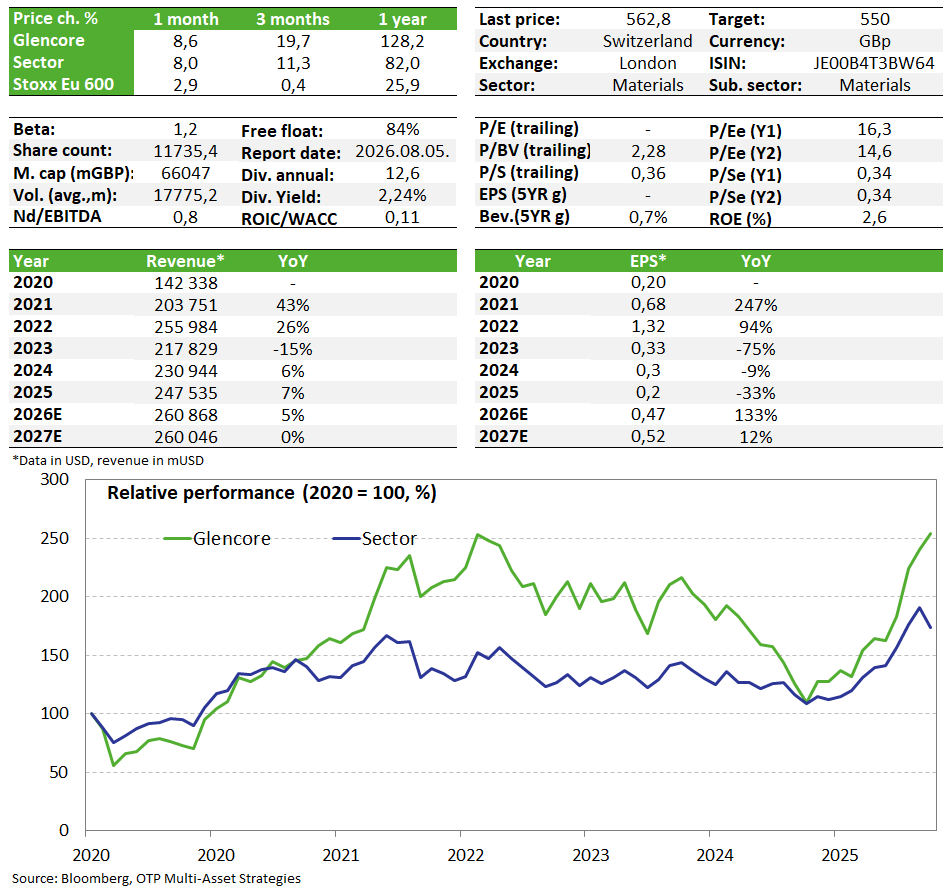

Glencore: metals supported results, but coal is not yet strong

Related content

Honeywell's stock price may be on the verge of a breakout

Major indices began to fall at the end of last week, but the movements were news-driven, and there has been significant volatility, which has resulted in a low number of opportunities indicating a quality breakout for the past two weeks. This week, one of the stocks from our Equity Top Pick List, Honeywell, also ranked high on the momentum list. After a minor pullback, the technical picture could indeed be supportive.

Uber Falls on Negative News

Uber shares failed to follow through on their breakout attempt, and on Friday, negative news concerning the company’s robotaxi business pushed the share price down to the stop-loss level specified in our trading idea.

Glencore’s annual results exceeded analysts’ expectations, but the picture was still weaker on a YoY basis. Performance was driven primarily by industrial and precious metals, while low prices held back profit generation in the coal production segment. In the latter case, however, the market outlook has improved in recent months, with prices rising slightly. Valuation is still not particularly high and we see some further room for possible earnings improvement. We are therefore keeping the stock for now on our Equity Top Pick List.

Quarterly earnings

Glencore’s 2025 annual results exceeded analysts’ expectations on basically every key metric, with earnings per share of $0.20 compared to the expected $0.17, while EBITDA came in at $13.5 billion versus the estimated $13.2 billion. Year-over-year, the picture is somewhat weaker: while revenue rose by 7%, EBITDA fell by 6% and operating cash flow by 17%. This is primarily due to lower coal prices, while the metals division performed well.

In terms of individual operating segments, mining contributed nearly $10 billion to EBITDA in 2025. Metals accounted for approximately 65% of this, while coal production accounted for 35%. In terms of metals, prices for copper, zinc, aluminum, as well as gold and silver improved last year, while for coal, both thermal and coking coal prices declined significantly (on an annual average basis).

Although annual copper production fell by 11% to 852,000 tons, its contribution to EBITDA was still nearly $4 billion, representing a 5% year-over-year increase thanks to higher prices. The segment stands out in terms of EBITDA margin, which was 47% in 2025. Zinc production was similarly strong, with improvements in both volume and pricing.

In contrast, EBITDA for total coal production was $3.4 billion last year, representing a 31% year-over-year decline (the EBITDA margin fell from 36% to 26%). Here, the production volume of coking coal, which is required for steelmaking actually increased by 63% year-over-year (thanks to the EVR acquisition), while thermal coal—used primarily for heating and power generation—showed stagnation in this regard. However, this was not enough to offset the decline in prices. It should be noted, however, that the price of coking coal has generally trended upward in recent months, and thermal coal prices have also risen, but historically, both remain at lower levels.

The company’s other major business segment, “marketing”—which encompasses the trading and logistics of raw materials produced in-house and sourced from third parties, as well as several other activities—also posted weaker annual EBITDA performance ($3.56 billion; -6% year-over-year).

Glencore is expected to produce 810,000–870,000 metric tons of copper in 2026, which is approximately 1.5% lower year-over-year, but an increase is anticipated starting in 2027 (2027: 930,000 metric tons; 2028: 1 million metric tons). At the same time, zinc production will decline (-26% year-over-year) and may remain at similar levels in the coming years. Coal production (coking and thermal) may stagnate around current volumes.

The company proposed a payout of 17 cents per share this year (a base dividend of 10 cents per share and a 7-cent bonus based on the value of the company’s 16.5% stake in Bunge, which has appreciated significantly). This amounts to a total payout of approximately $2 billion, to be distributed in two installments in June and September (corresponding to a dividend yield of approximately 2.2%).

Finally, it is worth noting that in recent months there were reports that Rio Tinto was considering acquiring the company (its copper portfolio would have been of particular interest to Rio), but these negotiations ended unsuccessfully. According to industry rumors, Glencore wanted a higher premium for its assets, and the parties were also unable to reach an agreement on management changes.

Valuation and debt

The company’s net debt stands at $11.2 billion, which corresponds to a net debt / EBITDA ratio of roughly 0.83x, which is relatively low, so there are no debt-related issues (Glencore’s credit rating is also in the investment-grade category according to both Moody’s and S&P).

Despite the recent price increase the valuation is still not considered high, but it is no longer cheap either. The share price has already reached our current 550 pence target (5.5 GBP), which we will reconsider after the company’s next production report. Coal prices have also risen recently (partially due to the USA-Iran war), and we continue to view the copper market as strong in the long term, where the company also has a significant presence (though there are short-term risks here due to high USA inventory levels and the USA-Iran war), and its growth portfolio is particularly good in this area. This means there is still room for profit growth in the coming years. We are therefore keeping Glencore shares on our Equity Top Pick List.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more