Our Fixed Income Top Picks

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

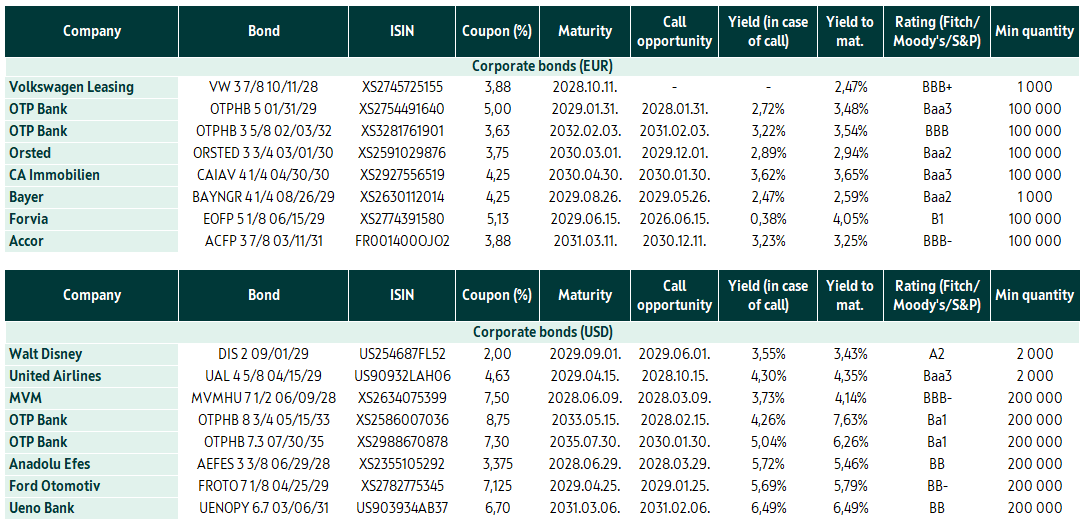

Although forint-denominated assets are currently performing exceptionally well, we still consider it important to diversify the bond portfolio by currency, which should be achieved through euro- and dollar-denominated regional government bonds, as well as euro- and dollar-denominated securities issued by highly rated companies. Currency diversification is not a stance against forint-denominated assets, but is necessary to reduce concentration risk. In our analysis, we have selected instruments linked to fundamentally stable issuers that offer acceptable yields in the current market environment.

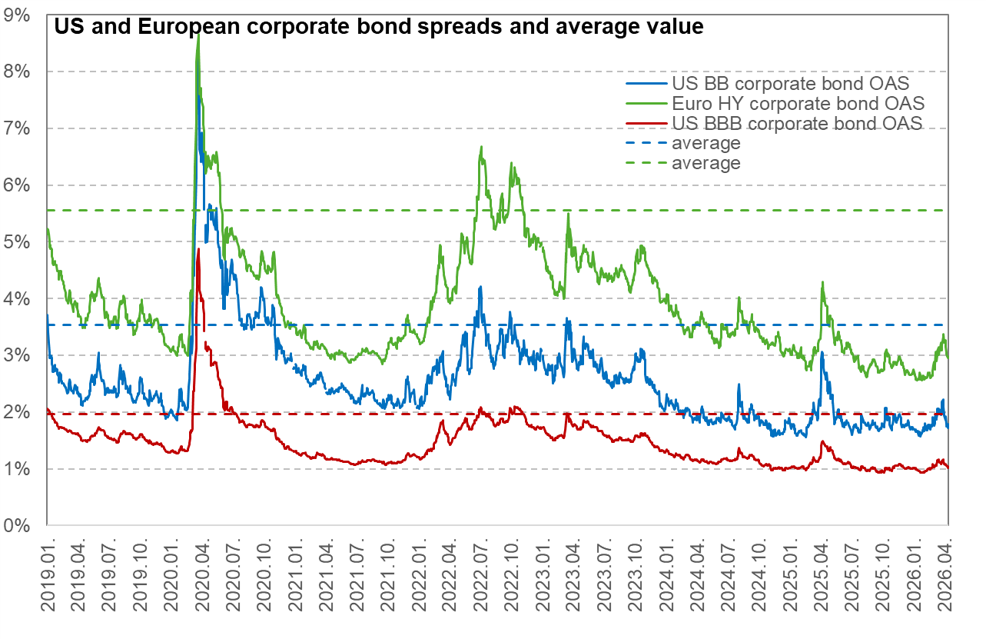

Historically, U.S. corporate bond spreads remain at very low levels, although they have risen slightly recently due to the conflict in Iran. Spreads for investment-grade (BBB) bonds are hovering just above 1%, while those for BB-rated bonds (1.72%) are also close to their lows (1.56%). We saw similar movements in the European high-yield bond segment; the spread rose from 2.60% in February to as high as 2.96% by mid-April, but it remains well below the long-term average.

Euro-Denominated Corporate Bonds

Yields on corporate bonds remain at low levels, even though the conflict in Iran has caused a slight increase. At the same time, as we get closer to the end of the war, risk appetite is returning to the capital markets. There is only a very minimal yield premium, if any at all, for euro-denominated high-yield (HY) securities compared to the investment-grade category. Therefore, one must consider whether it is worth taking on greater risk for a relatively small premium.

Dollar-Denominated Corporate Bonds

Companies in the region typically issue bonds in euros, so the supply available in dollars is much more limited. The list includes two bonds linked to OTP, a subordinated instrument maturing in 2033 and another in 2035, as well as a Hungarian-issued bond, namely MVM’s note maturing in June 2028.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more