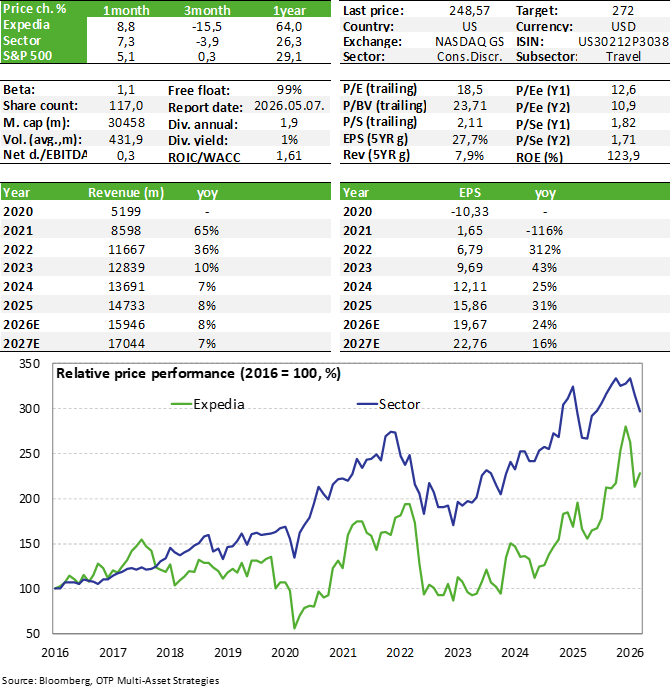

Expedia is performing strongly, but even that wasn't enough

Related content

Honeywell's stock price may be on the verge of a breakout

Major indices began to fall at the end of last week, but the movements were news-driven, and there has been significant volatility, which has resulted in a low number of opportunities indicating a quality breakout for the past two weeks. This week, one of the stocks from our Equity Top Pick List, Honeywell, also ranked high on the momentum list. After a minor pullback, the technical picture could indeed be supportive.

Uber Falls on Negative News

Uber shares failed to follow through on their breakout attempt, and on Friday, negative news concerning the company’s robotaxi business pushed the share price down to the stop-loss level specified in our trading idea.

Expedia posted strong growth across its key metrics at the end of last year, significantly exceeding analysts’ expectations. However, the bar had been set high for 2026, and the company fell short of those expectations, causing the stock price to drop in response to the report. At the start of the year, however, management typically sets more conservative outlooks, meaning the company may eventually be able to deliver better-than-expected results again, while the stock price remains at comfortable levels. For now, we are keeping the stock on our Equity Top Pick List, but the future growth challenges posed by AI agents must be treated as an additional risk.

Quarterly Report

The number of nights booked through Expedia rose by 9% during the quarter, and total spending reached $27 billion, meaning that even the unusually long government shutdown did not cause a slowdown. Since the average booking value also rose, total revenue grew by 11%, driven primarily by the B2B segment—that is, corporate partners (24%)—compared to 4% growth in the consumer segment. However, these increases were positive surprises compared to expectations in both cases, so the total revenue of $3.5 billion also beat the consensus estimate of $3.4 billion.

In addition to revenue growth, on the cost side, while marketing-related expenses continued to rise (+10%), the company managed to exercise tighter control over headcount (the workforce did not grow compared to the base period), resulting in a 370-basis-point improvement in the EBITDA margin, which was entirely driven by the direct retail segment. EBITDA grew by 32% year-over-year, a level of growth not seen in a long time, and the $848 million figure far exceeds the $759 million consensus. At $3.78, EPS also surpassed the $3.37 expectation, representing a 58% increase.

The company continues to generate strong cash flow while maintaining a low level of debt. Free cash flow (FCF) reached $3.1 billion last year, representing nearly 11% of market capitalization. Of this amount, $1.7 billion was used to repurchase shares, while the company paid out $0.2 billion in dividends.

Based on trends to date, the outlook for 2026 remains fundamentally optimistic, and the projected expectations reflect this. Revenue is expected to grow by 6–8%, while the EBITDA margin is projected to improve further by 100–125 basis points. The quarterly dividend was raised by 20% from $0.40 per share to $0.48 per share.

Despite the very strong performance, the stock price still reacted negatively, and there may be several reasons behind this. For one thing, Expedia has outperformed its peers in recent months, meaning market expectations were already quite high, and the management’s 2026 forecast failed to deliver a sufficiently compelling impact against that backdrop. It is important to note, however, that the company is typically more conservative with its outlook at the beginning of the year; thus, given that U.S. economic data is once again showing signs of improvement, the company may be able to deliver positive surprises relative to expectations this year as well. The bigger question is to what extent developments in the AI sector will put pressure on investor sentiment, as the emergence of AI agents could call into question the very rationale for travel intermediaries, and over time, fundamentally reshape the industry’s growth prospects if these new solutions take on a more direct role in travel planning and booking. We consider these risks to warrant close attention, but since both fundamental performance and valuation remain favorable for now, we are maintaining the stock on our Equity Top Pick List.

Valuation

The stock has significantly outperformed its peers in the recent period; while the previously substantial valuation discount has narrowed, it still presents an attractive picture overall. This is especially true given that performance continues to exceed expectations, and earnings growth remains particularly strong. The P/E ratio of 13 and the EV/EBITDA ratio of around 8 are thus still somewhat depressed, considering that EPS is expected to continue growing by around 20%, while EBITDA is projected to increase by approximately 11%. As the company’s fundamental performance improves, we maintain our previous fair value estimate of $272, determined using the multiple-based method.

Investment thesis

- Expedia is one of the world’s leading online travel marketplaces (most comparable to Booking). Three-quarters of its revenue comes from accommodation booking fees earned for acting as an intermediary, with the remainder coming from airline ticket sales, advertising, and other services.

- Expedia’s commission revenue is largely influenced by trends in tourism spending. Rising real wages driven by falling inflation also have a positive impact, while geopolitical tensions pose a risk.

- The company recently launched a single global loyalty program (One Key) to tap into the potential for cross-selling across its platforms. This cross-brand loyalty program is unique compared to competitors, which partly explains the recent growth in revenue and margin expansion—a trend that is expected to continue having positive effects in the future. Ariane Gorin, the former head of the B2B segment, took over as CEO in May 2024. Since then, the transformation has proven successful; the company has achieved solid growth, and with the AI-based solutions introduced, it has managed to keep pace with the market, with the first signs of this already visible in terms of efficiency.

- Earnings and cash flow are strong, and the company has resumed dividend payments this year after suspending them due to COVID-19, although this amounts to an annualized yield of less than 1%. The most significant item remains the share buyback program: last year, the company spent $1.7 billion of its $3.1 billion in free cash flow, which represents ~6% of market capitalization. Given the strong performance, this trend is likely to continue; the buyback program would allow for nearly $3 billion in purchases, providing strong support for the stock price. In recent quarters, the pace of share buybacks has stagnated and is rising slightly.

- The activist hedge fund Starboard Value acquired a 9% stake in Tripadvisor, a close industry peer of Expedia, during the summer of 2025. The investor’s move may have been influenced by the relatively low valuation of TripAdvisor shares, which could indirectly draw attention to Expedia, which is trading at similarly depressed valuation metrics.

- However, the concerns among software service providers regarding AI developments may also raise questions about Expedia’s business model. If the role of AI agents in travel planning and booking begins to grow, it could significantly undermine the growth prospects of intermediary companies. This is a serious risk that could negatively impact investor sentiment toward the stock and the sector even within the next year or two.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more