Short-term uncertainties in the copper market

Related content

Honeywell's stock price may be on the verge of a breakout

Major indices began to fall at the end of last week, but the movements were news-driven, and there has been significant volatility, which has resulted in a low number of opportunities indicating a quality breakout for the past two weeks. This week, one of the stocks from our Equity Top Pick List, Honeywell, also ranked high on the momentum list. After a minor pullback, the technical picture could indeed be supportive.

Uber Falls on Negative News

Uber shares failed to follow through on their breakout attempt, and on Friday, negative news concerning the company’s robotaxi business pushed the share price down to the stop-loss level specified in our trading idea.

Ero Copper, which is included on our Equity Top Pick List, recently released its Q4 earnings report, which largely met analysts’ expectations. The company delivered very strong financial results, driven primarily by higher copper prices and a significant jump in production. At the same time, however, some clouds are casting a shadow over the short-term outlook for the copper market. Global inventory levels have surged to multi-decade highs, while the war in Iran that erupted at the end of February could lead to rising operating costs and a slowdown on the demand side. We are therefore removing Ero Copper shares from our Equity Top Pick List. We originally added the company’s stock to our list at the end of 2023 at a price of USD 13.5, which has since risen by more than 90% over just two years.

Quarterly Report

Ero Copper recently released its Q4 earnings report, which was largely in line with analysts’ expectations. Full-year revenue was $786 million (+67% YoY), EBITDA was $410 million (+89% YoY), and earnings per share was $2.12 (+172% YoY). Operating cash flow also strengthened significantly, reaching nearly $400 million in 2025 (+172% YoY). The company thus delivered very strong financial performance last year, primarily due to higher copper prices and production.

In 2025, Ero produced a total of 64,300 tons of copper, representing a year-over-year increase of nearly 60%. The company’s existing Caraíba copper mine delivered stable performance with 36,000 tons (+1.6% YoY), while the ramp-up of the new Tucuma copper mine was also successful, resulting in production of 28,300 tons last year (vs. 5,200 tons in 2024). The increase in production is therefore almost entirely attributable to the new mine, where production costs are also quite low. At the same time, gold production at Ero declined significantly on an annual basis (37,300 ounces vs. 57,200 ounces in 2024), primarily due to the relatively lower ore grade.

This year, the company expects to produce 67,500–77,500 tons of copper, which would represent an annual increase of approximately 13% based on the midpoint of the guidance. Costs are expected to remain low this year as well (average cash cost of $2.15–2.35 per lbs). A slight improvement is also expected in gold production, which could reach 40,000–50,000 ounces, although production costs here may remain high ($2,000–2,500 per ounce AISC).

On the positive side, capital expenditures will not be too high, ranging between $275 million and $320 million, with the bulk of that amount likely to be allocated to the improvement of the Caraíba copper mine. Net debt stood at $502 million at the end of 2025, which is not particularly high (net debt/EBITDA ratio of 1.22). In this regard, however, we note that the copper market is quite cyclical, so both EBITDA and cash flow can fluctuate widely depending on economic conditions.

The company’s valuation remains low; based on the 2025 EPS, the P/E ratio stands at 12.5, while based on the expected 2026 EPS, it is 6.2. However, we also note that this could easily change depending on the trend in copper prices.

The copper market and the war in Iran

Copper prices remain at relatively high levels, although a moderate correction can be seen in recent weeks compared to the historical peaks reached in January. Several factors contributed to the earlier rise, including severe mining accidents last year, large capital investments flowing into data centers, as well as interest rate cuts and the weakening of the dollar. The longer-term (multi-year) outlook appears strong due to the potential for strategic stockpiling, tight supply, and demand-side trends (e.g., electrification, data centers, electric vehicles, renewables, cooling/heating needs, etc.). Moreover, increasing production in the case of copper is no simple task and requires significant investment.

However, the short-term outlook (over the next few months) is currently clouded by several factors, and investors would be wise not to overlook them:

- High inventory levels: one of the interesting developments in recent months has been that global copper inventories have surged to a multi-decade high, which is typically a negative sign for a commodity. This was mainly driven by a wave of stockpiling in the U.S., as it cannot be ruled out that the Trump administration will impose tariffs on refined copper starting in 2027, though there are uncertainties here (especially given the ongoing war in Iran). A potential reduction in the speculative component of U.S. inventories could temporarily push copper prices lower.

- The impact of the Iran war: another problematic development recently has been the USA-Iran war, which has led to a significant spike in energy prices. Higher oil and gas prices, coupled with disruptions in certain supply chains (e.g., chemical products), could deal a double blow to miners. On the one hand, this could increase miners’ costs through higher prices for fuel, electricity, materials (e.g., explosives, chemicals, sulfur, etc.), and transportation. On the other hand, all of this could slow global economic growth, which in turn could undermine demand. Overall, the longer the conflict drags on, the greater the impact of these factors will be on mining companies’ margins. Another headwind is that the dollar is strengthening again as a result of the war, and interest rate cuts may also be pushed back, which is typically negative for commodities.

Given the uncertainties surrounding the conclusion of the war in Iran and the high inventory levels, we are removing Ero Copper shares from our Equity Top Pick List. However, we note that the stock price has more than surpassed our previous target price of $27 in recent weeks. We originally added the company’s stock to our list at the end of 2023 at a price of USD 13.5, which has since risen by more than 90% over just two years.

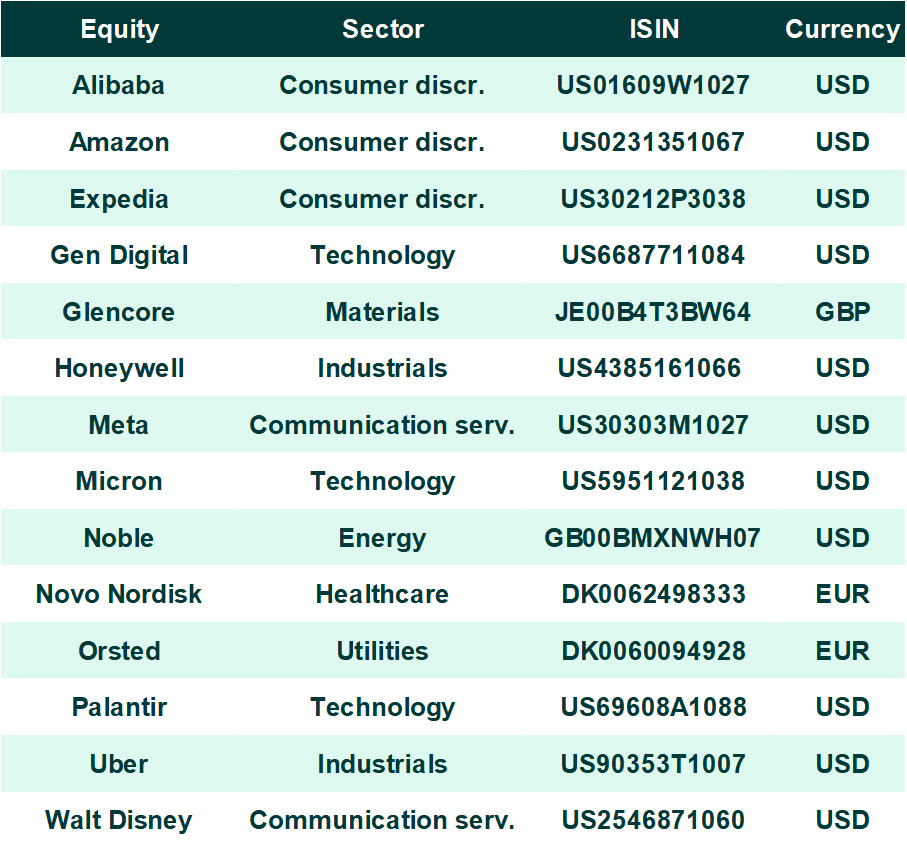

Equity Top Pick List

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more