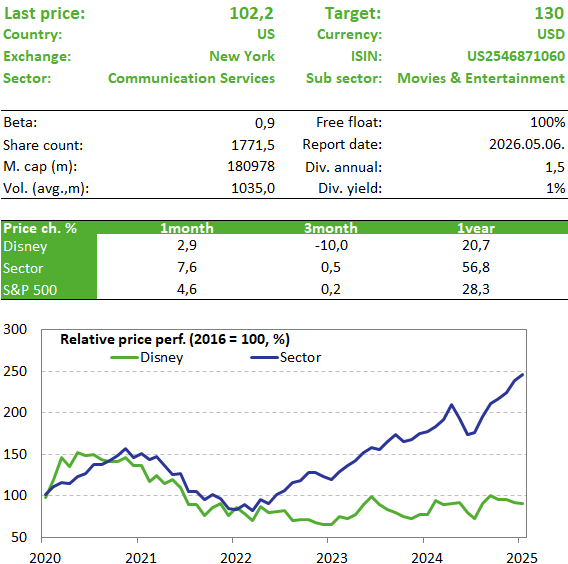

Succession issues are weighing on Disney shareholders

Related content

Honeywell's stock price may be on the verge of a breakout

Major indices began to fall at the end of last week, but the movements were news-driven, and there has been significant volatility, which has resulted in a low number of opportunities indicating a quality breakout for the past two weeks. This week, one of the stocks from our Equity Top Pick List, Honeywell, also ranked high on the momentum list. After a minor pullback, the technical picture could indeed be supportive.

Uber Falls on Negative News

Uber shares failed to follow through on their breakout attempt, and on Friday, negative news concerning the company’s robotaxi business pushed the share price down to the stop-loss level specified in our trading idea.

Disney exceeded expectations across all key metrics in the most recent quarter. The streaming business generated record profits, the traditional TV division continued to struggle, and the dispute with YouTube also weighed on profits. In contrast, the Disneylands remain the engine of the company’s profitability. However, investors’ attention is increasingly focused on the upcoming CEO succession, which has caused headaches in the past, so the stock price reacted negatively after the market open.

Quaterly report

Disney beat expectations across its key metrics for the most recent quarter. The company reported revenue of nearly $26 billion (+5% year-over-year), while net income came in at $2.4 billion (-6% year-over-year).

The streaming division performed exceptionally well, although the company no longer discloses subscriber numbers—similar to Netflix—so that investors focus instead on revenue and profit figures. The streaming division generated a record $450 million in operating profit (vs. $375 million expected), with a margin of 8.4 percent. Management also reaffirmed its plan to achieve a 10% margin by the end of this fiscal year.

The film studio also had a strong quarter, with Zootopia 2 and the new Avatar each grossing well over $1 billion at the box office. However, the segment’s profit figures were dragged down by significant marketing costs, as the expenses for films released during the holiday season (especially Avatar) were already accounted for in December, but a significant portion of the box office revenue carried over into the following year.

The linear TV business continues to struggle, with advertising revenue falling by 6 percent due to steadily declining viewership; moreover, the same quarter a year earlier had been particularly strong due to the election campaign at the time. This did not come as a major surprise to shareholders, however, as it is part of a multi-year downward trend. Management did not sugarcoat the results, instead placing the emphasis on keeping expenses under control.

The sports division’s results were hurt by the dispute with YouTube TV, during which Disney channels were unavailable on the platform for 15 days. As a result, quarterly operating income fell 23% to $191 million, with $110 million of that decline attributable to the YouTube dispute.

The Parks and Products division generated $10 billion in revenue and accounted for 72 percent of operating profit, indicating that the holiday season was particularly strong at the Disneylands. For the current quarter, however, management expects weaker numbers, with only “modest” growth anticipated, primarily due to lower international visitor numbers. And since this segment is primarily responsible for profit growth, a significant negative reaction in the stock price is evident.

But the CEO succession could also weigh on shareholders; the board is expected to decide on Bob Iger’s successor in the coming days or weeks. The last CEO change took place in 2020, but it was so unsuccessful that Iger had to be brought back at the end of 2022. Now, two internal candidates are in the running. Josh D’Amaro, head of the parks division, or Dana Walden, co-head of the entertainment division. Overall, the quarterly results weren’t bad, and the stock price drop due to the subdued quarterly outlook seems excessive, so the stock remains on our Equity Top Pick List.

Investment thesis

- Disney is one of the strongest brands in the media sector, and its diversified portfolio provides it with a long-term competitive advantage. Streaming is only now beginning to yield real results, and a major overhaul of the sports division could also help drive growth.

- The film studio’s success is also essential, although it’s quite unpredictable how the year will unfold in that regard. As for the Disneylands, the company is planning major investments in the coming years, and there are still no signs of a decline in spending at the parks in this segment, though management has slightly lowered expectations for the current quarter. The traditional TV business, as we saw in the latest report, is struggling, but the negative effects can be mitigated through cost-cutting measures or a potential sale.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more