These companies can benefit from favorable cybersecurity trends

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

The outlook for the cybersecurity sector is supported by several structural growth factors. The most significant catalyst is the accelerating demand for AI-based solutions and cloud services, which is generating significant market expansion. In addition, the increase in the number and complexity of cyberattacks, as well as escalating geopolitical tensions, may sustain demand for the sector's services in the longer term. In the short term, a potential cycle of interest rate cuts could also have a positive impact on the industry's valuation and investor sentiment. In our analysis, we focus on which companies are best positioned to benefit from these key growth drivers. We highlight three players: a large company (Palo Alto Networks), a medium-sized player (Datadog), and a smaller-cap company (SentinelOne).

One of the most important structural tailwinds for cyber defense is AI, which supports the industry in a number of ways. On the one hand, there has been an increase in demand for cloud services and, with it, for the monitoring and protection of cloud and cloud-based workflows. Furthermore, the dynamic growth in the number of AI agents could also be a catalyst for certain areas of cyber defense, as agents access data and applications in the course of their operations, and authentication and identity security solutions are needed to ensure that they can do so securely.

In addition, artificial intelligence enables cybercriminals to carry out more sophisticated attacks, which require more complex defenses, thereby increasing demand for cybersecurity services. Gartner predicts that by 2027, attacks using generative AI could account for 17% of all cyberattacks. In addition, it is worth mentioning the increase in the number of cyberattacks—in the first quarter of 2025, there were almost three times as many cyberattacks per company per week as there were five years ago. Furthermore, due to stricter regulations and greater transparency, companies may be even more motivated to prevent data breaches, as these can pose a serious reputational risk for them, so they are willing to spend more resources on prevention, which ultimately translates into increased demand for cyber security companies.

Beyond AI, growing geopolitical tensions around the world may also contribute to impressive growth in the industry, especially in the future as hybrid warfare becomes more prevalent. Partly as a result of this, NATO's new defense spending plan no longer focuses solely on traditional defense functions but also allocates 1.5% of GDP to infrastructure and cyber defense (albeit with a distant deadline of 2035). This could give the industry a major boost in the longer term, as only 0.1% of US GDP is currently spent on cybersecurity (more details here).

The industry is in a growth phase, with many smaller companies that entered the market a few years ago and are not yet profitable, or have only been profitable for a few years, so the greater cash flows for companies are likely to be further in the future (more details here). As a result, the industry is more sensitive to interest rate cycles, and a looser monetary policy carries strong upside potential for the industry. Many companies in the sector can benefit from the growth drivers mentioned above, especially those involved in artificial intelligence. In our opinion, the following players are best positioned to take advantage of the favorable industry trends:

Palo Alto

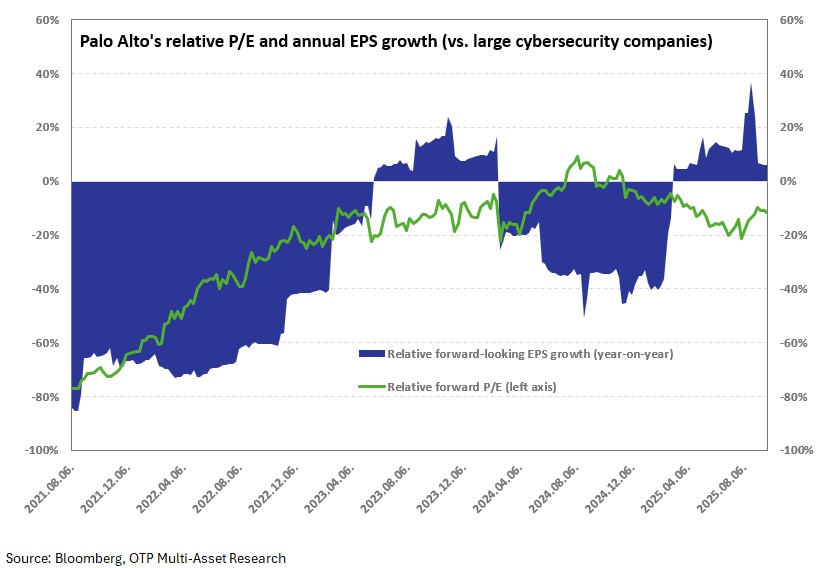

Palo Alto Networks is the largest pure-play cybersecurity company (with a market capitalization of $140 billion), offering solutions in areas such as network security, cloud security, and threat detection. The company is well positioned for the transformation brought about by artificial intelligence and, following the completion of the CyberArk transaction, will have the most comprehensive platform in the industry. The acquisition will expand the company's product offering with identity protection and authentication services, which may be particularly important areas in the future in terms of secure access to data for AI agents. In addition, Palo Alto has assembled one of the best cloud-based tool portfolios in its category, featuring next-generation firewalls (SASE), cloud-based workflows, security automation, and endpoint protection services.

The company's strong market position contributes to cost-effective operations and relatively high pricing power, resulting in the strongest margins in the industry. Nevertheless, it trades at a discount of around 10% in P/E-based valuation compared to large cyber security companies, while its profit dynamics outlook is slightly better than that of its competitors. Although it lags somewhat behind in revenue growth, the acquisition and integration of CyberArk could help accelerate growth. It is one of the best in terms of cash flow margin (~40%) and growth (~30%), and with its strong market position, a premium valuation would be entirely justified, but this is not currently reflected in the valuation multiples, so there may still be upside potential.

Overall, the CyberArk transaction positions Palo Alto as a leading artificial intelligence security platform and supports its favorable growth prospects. Among the main risks, it is worth mentioning the possible intensification of competition with next-generation cybersecurity companies. Furthermore, the CyberArk acquisition cannot be considered a cheap acquisition at all, as the company was acquired at 23 times its revenue, compared to an industry average of 8 times for similar deals. Therefore, it is essential for Palo Alto to realize the benefits of synergies if they want to create value, and thanks to good cross-selling opportunities, they have every chance of doing so.

Datadog

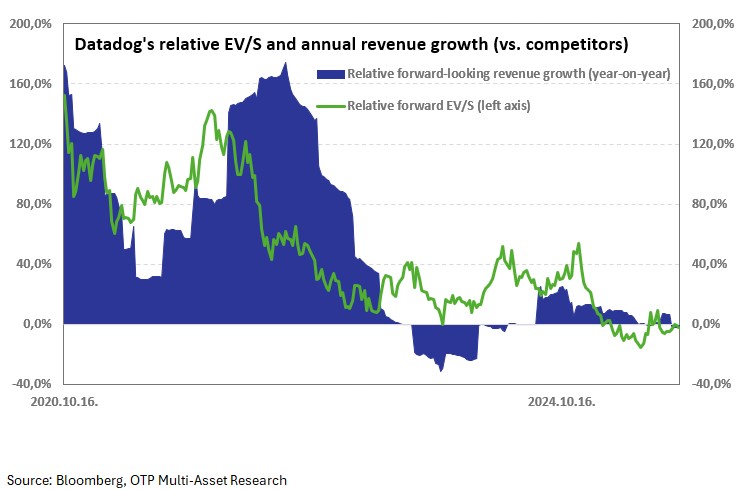

Datadog is a US-based cybersecurity company with a market capitalization of $50 billion and a leading player in cloud and on-premises application monitoring. It delivers its services through a comprehensive, unified platform. The company works with major cloud providers such as AWS, Microsoft Azure, and Google Cloud to offer integrated monitoring solutions. These partnerships enable Datadog's customers to leverage multi-cloud architectures, which increase operational flexibility and mitigate unilateral exposure to large technology providers.

The company's technologies integrate and automate infrastructure monitoring, application performance monitoring, and log management to provide seamless observability, cloud security, and developer use cases. The cloud infrastructure segment represents the greatest growth potential for Datadog, as the company benefits directly from the increase in demand generated by cloud migration and digital transformation, particularly the megatrend of artificial intelligence. The continuous operation of AI solutions and large language models (LLMs) requires constant monitoring and performance management, which directly increases demand for the company's services. AI-focused companies already account for 11% of Datadog's revenue, up from 8% in the first quarter of 2025, indicating rapid expansion in this customer segment. The largest such partner is OpenAI, which accounts for approximately 3.5% of the company's revenue.

The company's valuation multiples (EV/S and EV/FCF) are similar to those of its competitors, as are its revenue growth and cash flow expansion. What sets it apart from other fast-growing cybersecurity companies are its above-average cash flow margins, which could even justify a premium valuation. In addition, the company's management has performed excellently in the past, which will continue to be necessary in the future to maintain its market leadership in the field of observability and monitoring and to sustain strong growth in its fundamentals.

SentinelOne

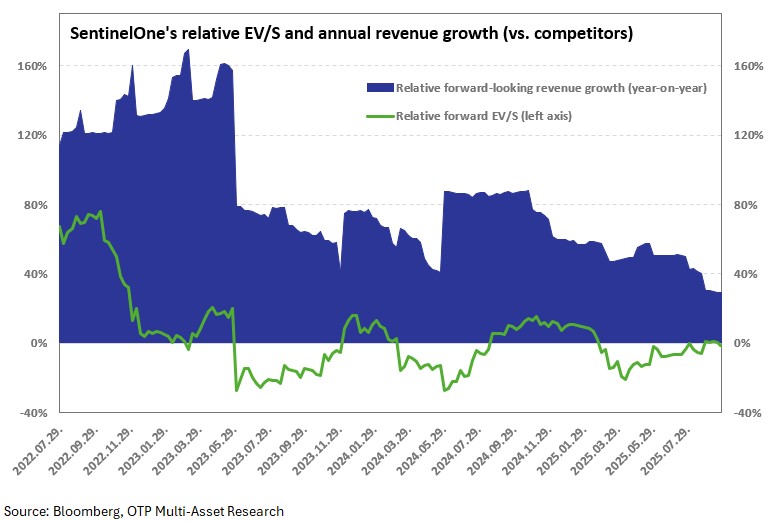

SentinelOne is a small American cybersecurity company that develops AI-based, automated defense solutions to protect against modern cyber threats. The company offers comprehensive, primarily endpoint and cloud-based defense solutions through its Singularity platform. SentinelOne is a leader in this field, performing activity monitoring, threat detection, and response autonomously in real time.

The company is at the forefront in terms of technology offerings, with Purple AI, one of the industry's most advanced artificial intelligence security analysts, helping customers perform detailed analysis of cyber-attacks, reducing manual tasks and improving efficiency. The company can benefit in two ways from the spread of the AI ecosystem. On the one hand, artificial intelligence technologies are closely integrated into the development and operation of cybersecurity solutions. On the other hand, demand for cloud security is expected to grow dynamically in the coming years as an increasing proportion of data and applications move to cloud-based environments. This trend could provide significant growth momentum for the company in the medium term.

SentinelOne is a company in the early stages of growth, with revenue growth of around 20% exceeding that of its competitors, but we see discounts in terms of valuation compared to similar companies. This is primarily due to weak operating and cash flow margins, which are the result of exceptionally high sales and marketing costs associated with the market acquisition phase, accounting for 60% of total revenue and thus putting pressure on profitability. However, the company's business model is highly scalable, which is expected to help widen margins in the future. According to analyst estimates, the cash flow margin could approach that of its competitors by 2027, while the stock is trading at a discount of nearly 15-20% on an EV/S and EV/FCF basis for 2027. Meanwhile, it is expected to continue to outperform similar companies in terms of growth (revenue growth: 20%, FCF growth: 80% in 2027).

Overall, SentinelOne is a smaller company with a market capitalization of $6 billion and higher risks. Key risks include intense competition from larger industry peers, which could keep margins under pressure, and weaker management performance, which could limit growth opportunities. However, some of these risks are already priced in, making it an exciting choice for investors with a higher risk appetite due to its significant potential.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more