Copper price remains near historic highs

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

Following the outbreak of the Iran war in late February, the price of copper first fell and then rose to new all-time highs and it is currently still not far from those levels. This is relatively surprising, as the prolonged closure of the Strait of Hormuz may have numerous negative economic consequences, which, at least in theory, are unfavorable for industrial metals such as copper. In our view, this is due not only to optimism surrounding the data center construction boom but also to disruptions in supply chains caused by the conflict in the Middle East, specifically the shortage of sulfuric acid. In our analysis, we explore the latter topic in detail and examine its potential implications for the copper market.

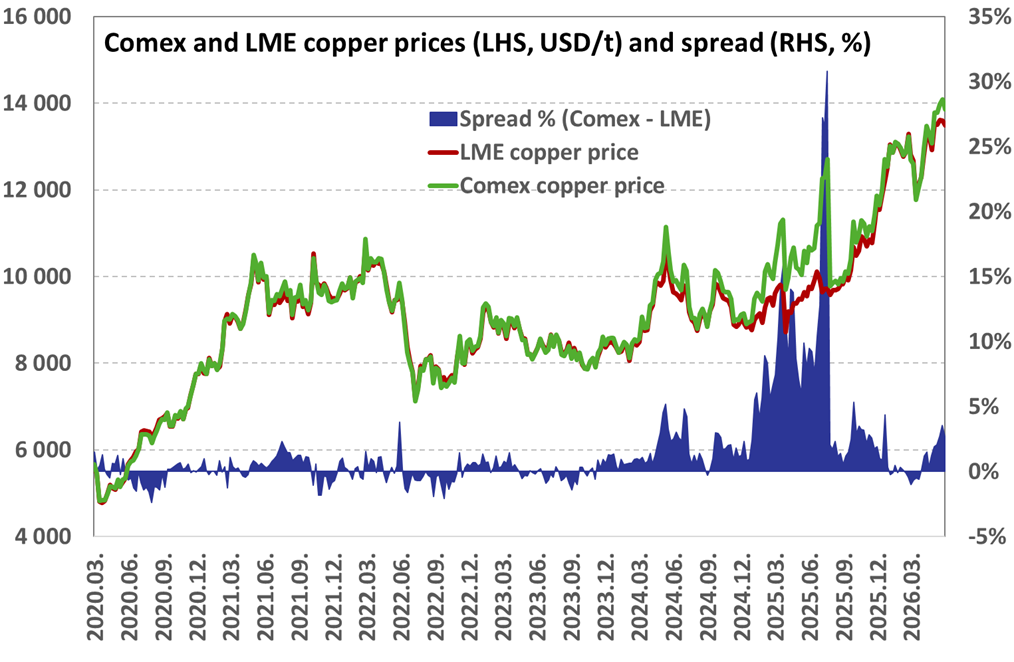

Copper price near record highs

Copper got off to a particularly strong start this year, rising to a new record high in January, but prices fell following the outbreak of the Iran war in late February. Subsequently, however, copper began to rise again, with the U.S. (Comex) price reaching a new all-time high, while the London (LME) price came close to doing so.

The question naturally arises as to what is driving the current high copper price, given that the war’s potential demand-destroying effect should, in theory, be pushing prices down, and global inventories are also near historic highs, which is another negative factor. In our view, the supply disruption of sulfuric acid caused by the closure of the Strait of Hormuz plays an important role here, as it dealt another blow to a supply side that was already tight due to last year’s serious mining accidents. Furthermore, the optimism surrounding data centers can also be considered a positive tailwind.

Disturbance in the Force: the sulfuric acid problem

To understand the essence of the “sulfuric acid problem,” we will first briefly review the sulfuric acid market and its relationship with copper. We will then examine how the war in Iran affects all of this and what the potential consequences might be.

Sulfuric acid is one of the most widely used chemicals in the world, primarily used in fertilizer production, various chemical processes, and metal processing (e.g., for certain types of copper, nickel, and lithium). This substance does not really occur naturally in the environment, so it is generally produced through industrial processes. This requires sulfur as a raw material, which is largely supplied by the oil and gas industry, where it is produced as a by-product in refineries and processing plants during the desulfurization process.

It is worth noting that different types of oil and gas have varying sulfur contents, meaning that the potential for sulfur production varies by region (e.g., oil from the Middle East typically contains more sulfur). Another important source of sulfuric acid is metal processing, where sulfur dioxide is produced during the refining process when sulfide ores are heated (e.g., certain types of copper, nickel, and zinc), which can also be converted into sulfuric acid through further chemical processes.

But what does this have to do with the price of copper and the supply chain?

As mentioned earlier, sulfuric acid is used, among other things, in metal processing, making it a chemical commonly used in the processing of certain types of copper. Copper ores can basically be classified into two main types: sulfide and oxide. In the former case, copper forms a chemical bond with sulfur, while in the latter case, it forms a bond with oxygen; consequently, the ore processing methods are completely different in the two cases. An interesting aspect of sulfuric acid is that it can be produced as a by-product during the processing of sulfide copper, whereas the processing of oxide copper requires significant amounts of sulfuric acid.

Approximately 80–85% of global copper production is sulfide-based, while the remaining 15–20% is oxide-based (considering only primary mining and excluding reprocessing). It should also be noted that oxide copper is typically processed locally, whereas in the case of sulfide copper, the copper concentrate is often shipped to another country (primarily China), where smelters and refineries are located, as this is an energy-intensive process. This is important because, as a result, sulfuric acid production does not necessarily take place where sulfide copper is mined, whereas in the case of oxide copper, sulfuric acid demand arises locally within the producing country.

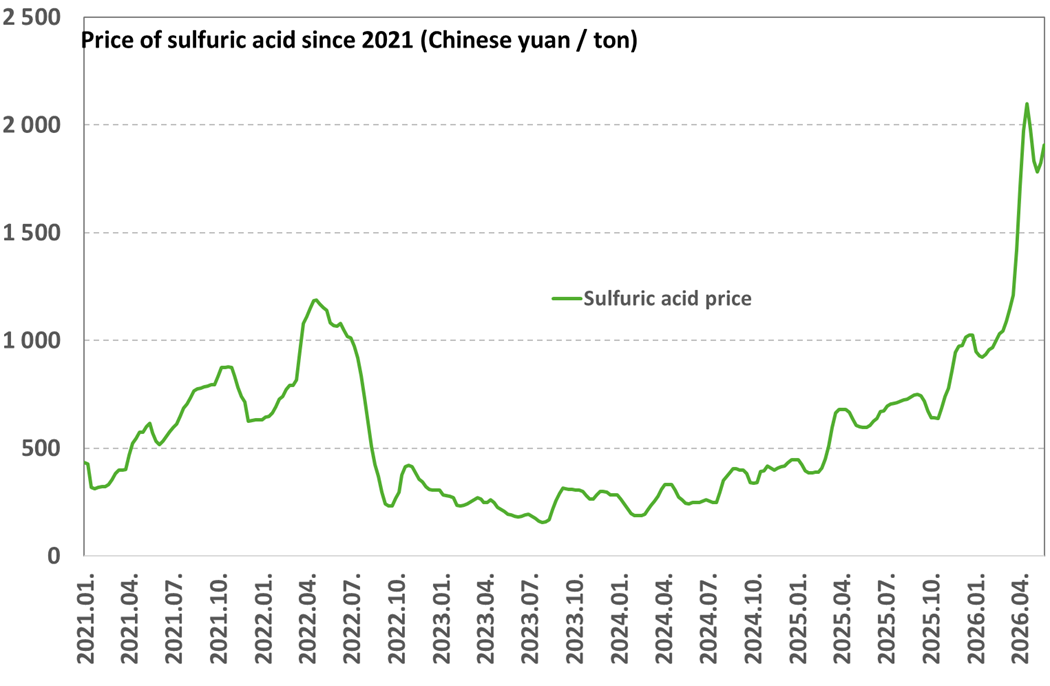

The conflict in Iran and the closure of the Strait of Hormuz have caused significant disruption to this fragile ecosystem. Nearly half of the world’s sulfur exports pass through this hub (as a by-product of significant oil and gas processing in the Middle East), and the vast majority of this sulfur is used to produce sulfuric acid, often in the consumer/importing country (e.g., China, Congo, India, Indonesia, etc.). The sulfur price reacted strongly to the disruption in the supply chain, more than doubling since the start of the year and rising to about ten times its 2023 lows. This is due to individual end-users beginning to outbid one another due to the tight supply. The price of sulfuric acid has risen by a similar magnitude in parallel.

One of the regions most exposed to the conflict in Iran is Africa, where, according to Argus research firm, more than 90% of the sulfur imports of major copper-producing countries originate from the Middle East. This is important because these regions produce a significant amount of copper oxide, the processing of which requires large quantities of sulfuric acid. According to Fastmarkets research firm, for example, the Democratic Republic of Congo accounts for more than 50% of global copper oxide production (which represents ~8–10% of global copper production and more than half of the country’s copper output). It is therefore possible that if the conflict in Iran and the closure of the Strait of Hormuz drags on for a long time, disruptions in the supply of sulfur and sulfuric acid could affect a significant portion of global copper production.

Problems at the world's largest producer

Furthermore, sulfuric acid supply issues are not limited to Africa; they could also affect production in Chile, the world’s largest copper producer. The country produces approximately 5.4–5.6 million tons of copper annually, accounting for about 23–24% of the global market. A significant portion of production there is also oxide copper; according to a recent analysis by JP Morgan, its share was approximately 23% in March (about 4–5% of global copper production). According to the investment bank, supply disruptions caused by sulfuric acid were not yet apparent in Chile during the first month of the war, but they noted that production data for the coming months may provide a clearer picture in this regard.

The situation is further complicated by the fact that, according to several news sources, China has banned sulfuric acid exports since early May—a significant development, given that the country was the world’s largest exporter in 2025. In fact, this is a direct consequence of the war in Iran, as exports of sulfur by-products from oil and gas production there were a key input for Chinese sulfuric acid production. In addition, the country is also the world’s largest metal processor, so the significant amount of sulfuric acid generated as a by-product of this processing can no longer be exported in principle either. Given that roughly half of sulfuric acid consumption is related to fertilizer production, it is likely that China is seeking to protect its own agricultural industry with this seemingly drastic measure.

For Chile, this is particularly bad news, as according to an analysis by S&P Global, the country is the world’s largest importer of sulfuric acid, and nearly 40% of its supply came from China (Indonesia, another major metal producer, fared even worse, as 62% of its imports previously came from China). The irony of the situation is that a significant portion of Chile’s sulfide copper production ends up in China, where further processing generates a substantial amount of sulfuric acid by-product, some of which Chile then purchases and imports to process its own oxide copper production locally. This virtuous cycle could be disrupted by the Chinese export ban if Chile is unable to secure some form of exemption.

It should be noted that Chilean copper production has not performed particularly well so far this year, even without the sulfuric acid supply disruptions. The country’s copper production in March was down 9% year-over-year, while the first quarter saw a decline of nearly 6% compared to the same period last year. A January presentation by the Chilean Copper Commission had forecast a 3.7% increase in production in 2026 (in our experience, these are typically optimistic estimates that are often revised downward during the year). In contrast, they now expect a 2% decline for this year (approximately 5.3 million tons).

We would also like to note that in mid-April, reports emerged regarding India suggesting that the country was considering restricting sulfur exports (presumably with the primary aim of protecting the agricultural sector). India produces large quantities of sulfur as a by-product of oil refining, but it is also a significant importer (sources were mainly in the Middle East before the closure of the Strait of Hormuz). Of course, if oil supplies are also disrupted and refineries consequently operate at lower capacity, this could result in further shortfalls in sulfur and sulfuric acid, which could further incentivize the introduction of export restrictions.

Not everything supports higher copper prices

In our view, one of the key factors supporting the current high price of copper is the fact that investor concerns regarding the aforementioned sulfuric acid supply disruption have been at least partially priced in. It is important to note, however, that these supply issues have not yet materialized at the level of copper production, so to a large extent this reflects expectations (and is thus partly speculative in nature). Regardless, this is a significant disruptive factor, as it could potentially affect 15–20% of global copper production in some form (with strong regional variations). Moreover, this impact could be amplified if even more countries begin to restrict sulfur or sulfuric acid exports to protect their domestic agricultural sectors.

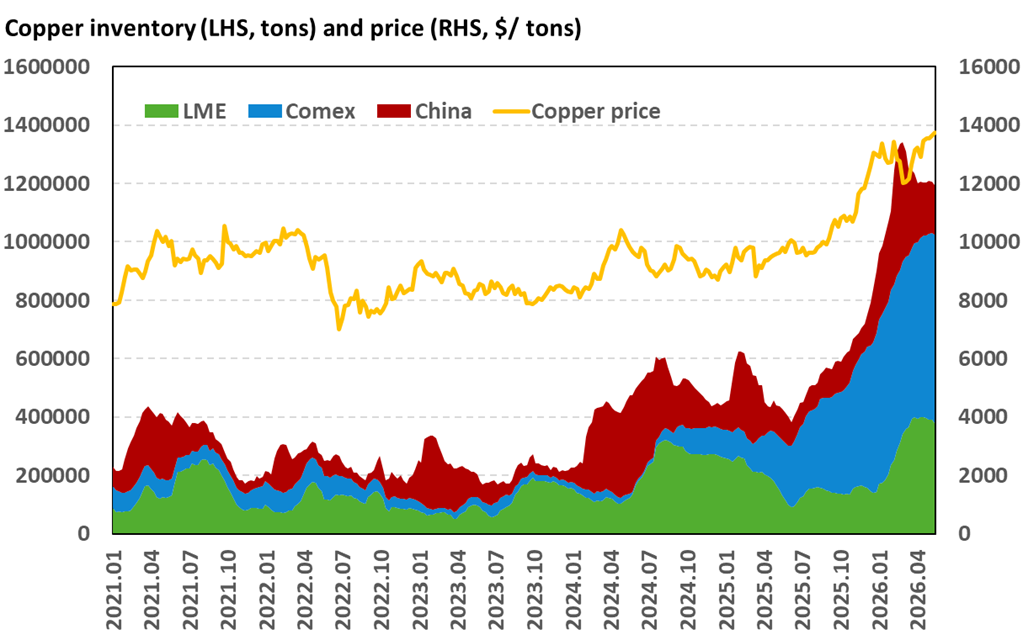

Another negative factor for the price, which reflects current conditions rather than expectations, is global inventory, which has surged to levels not seen in over 20 years over the past two years. However, there are marked regional differences here, as the United States holds about half of current inventories, where stock levels have never been this high and are well above the historical average. At the same time, inventories in London and China have also risen, but not to such a drastic extent.

When it comes to raw materials, high inventory levels typically indicate weak demand, as inventories generally rise when there is an oversupply in the market (though this is, of course, partly due to seasonal factors). In addition, the rapid growth in inventories in the United States was partly driven by speculation regarding potential import tariffs (it cannot be ruled out that the Trump administration will extend these tariffs to refined copper starting in 2027; news on this is expected in June).

Meanwhile, Chinese economic data does not look particularly encouraging either: retail sales rose by only 0.2% year-over-year in April, although the year-over-year increase for the first four months of the year was still 1.9%. At the same time, industrial production rose by 4.1% in April, while annual growth for the first four months of the year stood at 5.6%. Both economic figures fell significantly short of analysts’ expectations and indicate a weakening trend for now.

Finally, it is also worth noting that the longer the war in Iran and the closure of the Strait of Hormuz drags on, the greater the potential global economic consequences could be, and in some cases, a recession cannot be ruled out. Of course, data centers and electrification trends provide significant tailwinds for copper, but the price would likely still come under serious pressure as a result of an economic slowdown, as this would inevitably have a demand-destroying effect. Moreover, if a stagflationary environment were to develop, central bank interest rates would likely not fall; in fact, rate hikes could even occur, which would also be unfavorable for commodities.

Overall, it can be said that the price of copper currently reflects supply-side concerns as well as investor optimism regarding data centers and electrification. It is highly questionable, however, whether—in the event of a prolonged war—supply-side disruptions (the sulfuric acid supply problem on top of the already weak Chilean production and last year’s very serious mining accidents) would be able to offset a potential decline in demand, which is coupled with historically high inventory levels. In our view, the short- and medium-term outlook is thus surrounded by significant uncertainty, while in the long term (2–4 years), the outlook for the copper market remains extremely favorable (e.g., structural demand tailwinds, deteriorating ore quality, and a lack of major projects coming to completion in the next few years).

Implications for copper producers

We note that it is even more difficult to assess the outlook for copper producers, as margins remain very favorable due to high copper prices for the moment. However, due to the war in Iran, cost pressures may weigh on miners in the coming quarters, as expenses related to fuel, logistics, raw materials (e.g., sulfuric acid, explosives), and electricity may rise. The extent of this, however, depends on numerous factors, so it will not affect every producer in the same way.

To give a simple example: if a miner operates in North America and has access to relatively cheap fuel and electricity, and if processing costs are lower due to high-grade ore, then their cost structure is less vulnerable to disruption in the Middle East (of course, due to supply disruptions in sulfuric acid, it is worth being extra cautious regarding oxide producers). Naturally, it also matters whether the production is open-pit or underground, whether it involves oxide or sulfide copper, whether the mine’s location is favorable from a logistical and infrastructural standpoint, and so on. In the event of a drop in the copper price, these factors could become even more critical in terms of margins and earnings. Overall, our view here is similar: it is worth being cautious in the short and medium term, while the longer-term outlook remains extremely positive.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more