All eyes on the SpaceX IPO

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

SpaceX’s IPO has entered the home stretch, in what promises to be one of the year’s biggest market events. The company has set a fixed share price of USD 135 and is preparing to raise USD 75 billion. The initially low free float, the unusual lock-up structure and the prominent role of retail investors could together create a situation in which extreme volatility may occur in the first few trading days.

The big day is approaching

Further information has emerged in recent days regarding SpaceX’s stock market listing, and here again we are not seeing a conventional structure. Last week, ahead of the roadshow, the company set a fixed price of USD 135 per share and plans to sell 555.6 million shares at this price, raising around USD 75 billion and implying a total company valuation of roughly USD 1,770 billion.

In most IPOs, the issuer first provides a price range, with the final price then determined based on the roadshow and bookbuilding process. SpaceX, by contrast, entered the marketing phase with a fixed price of USD 135, suggesting that management and the banks expect strong demand. Elon Musk would, in any case, retain more than 82% of the voting control in the company after the IPO as well, although his actual ownership stake is much smaller, as he holds shares with preferential voting rights.

The banks participating in the offering may purchase an additional roughly 83.33 million shares at the IPO price under the so-called greenshoe option, which could represent a further supply of around USD 11.2 billion. The purpose of the greenshoe is to stabilize the share price in the days following the IPO. If the share price falls, the banks buy back shares in the market, thereby providing support to the price; if the share price rises, they do not buy back shares at a higher price in the market, but instead exercise the greenshoe option, meaning they purchase the additional shares from the issuer at the original IPO price. Importantly, this is only an option, not an obligation.

The first trading day may still be Friday, 12 June, and it will be highly interesting to watch what the share price does then, as well as over the following weeks and months. On the one hand, the question is how much liquidity it could absorb from other technology and AI stocks; on the other hand, it could provide a useful benchmark for the other mega-IPOs planned for this year, including the listings of OpenAI or Anthropic. Many have already partly attributed last Friday’s decline in the technology sector to this, as investors need to free up funds from somewhere ahead of a historically large IPO.

Index inclusion and lock-up

Another special feature of the offering is that a significant portion of the capital raise, potentially as much as 30%, is intended for retail investors. This is roughly three times the level typically seen in a large IPO and, since these investors generally do not buy for the long term, it increases the likelihood of significant volatility.

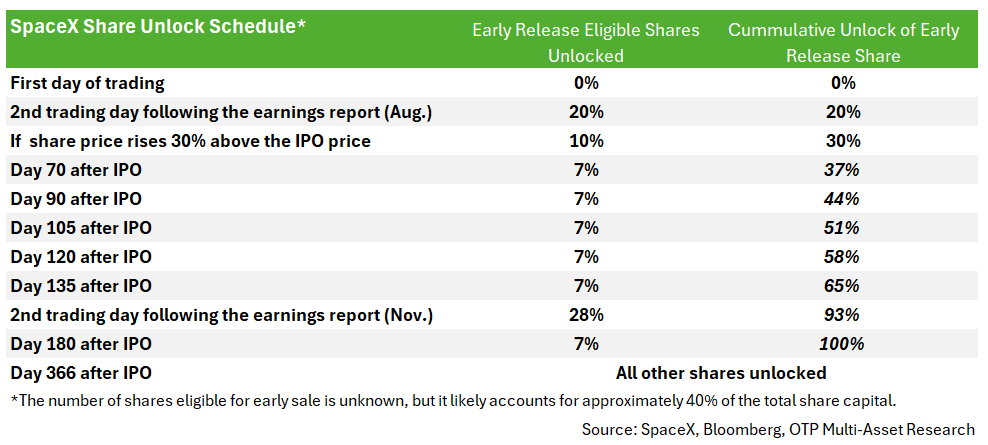

As we already discussed in our previous analysis, the lock-up structure differs from the traditional model. Although Elon Musk and several other early shareholders are subject to the customary one-year selling restriction, this may apply to around 60% of the total shares, while the remaining roughly 40% will be released gradually over the next 180 days.

This lock-up story is interesting because it is linked to the timing of the stock’s inclusion in the most important indices. Different index providers treat early inclusion differently. It now appears that the stock may enter the Nasdaq 100 after 15 trading days, the FTSE Russell indices after as few as 5 trading days, and the MSCI indices during the quarterly reviews. By contrast, it is expected to be included in the S&P 500 only after one year, as the index provider has indicated that it will not modify its inclusion requirements. In other words, passive demand from funds tracking the S&P 500 may only arrive later, even though many had assumed that they would also join the queue and include the stock sooner.

In any case, the initial free float in SpaceX shares will be only around 4%, meaning supply will be limited. Together with the hype that has built up, this could push the share price significantly higher in the first day or days. However, as an increasingly large percentage of the shares gradually becomes available, selling pressure could also emerge. It is also important that even if the stock is included in an index early, its weight will initially be small, since index providers look at free-float-adjusted market capitalization, which will also limit purchases by index-tracking funds at the outset. It will be interesting to watch whether the continuous expansion of supply and demand tilts the share price in one direction or the other over the remainder of the year.

Many had already bought in earlier

It should also not be overlooked that although SpaceX is only now becoming a listed company, its shares had already been tradable to some extent earlier. Of course, this did not mean traditional trading: an average retail investor could not simply place a buy order with their broker. Pre-IPO trading takes place on an over-the-counter secondary market, where an existing shareholder — for example an early investor, employee, SPV or hedge fund — sells their stake to a buyer.

The most common route was to buy through an SPV, or special purpose vehicle, which is a separate legal entity created for the purpose of purchasing, for example, SpaceX shares. Thus, the investor did not become a direct shareholder of SpaceX, but acquired a participation right in the SPV. These investors were accredited investors like big institutions, or wealthy private individuals. This is worth taking into account because it shows that many may have been able to get into the SpaceX story early, and they may now see the time as ripe to take profits, which again could be negative for the share-price performance. The story is complicated, however, by the fact that the lock-up may also apply, for example, to SPVs, and the SPV manager may even decide to transfer the shares to investors only several months later.

A huge acquisition on the horizon

We have already written about the company’s business units previously, so we will not repeat ourselves here, but the expected Cursor acquisition will be interesting. The structure had already been known earlier: SpaceX may acquire Cursor, an AI coding startup, for USD 60 billion 30 days after the IPO. If the transaction does not take place, SpaceX must pay the company USD 10 billion so that they can continue working together. Cursor is a competitor to Claude Code and OpenAI Codex, and could give a boost to the Grok model developed by xAI, which has recently fallen behind in the AI race. Coding is the area currently running very hot among AI models, as it is presently where the largest revenues can be generated in the shortest period of time. Of course, the big question is how quickly and efficiently the startup can be integrated into this mammoth company.

On June 5th, it was announced that SpaceX had also entered into an agreement with Google to sell AI compute capacity. Under the contract, Google may pay SpaceX USD 920 million per month from October 2026 to June 2029 for the use of roughly 110,000 Nvidia GPUs, as well as CPUs, memory and other related infrastructure. The capacity will be built up gradually until September 2026, at a reduced fee. If SpaceX is unable to provide the committed GPU volume by 30 September 2026, Google may terminate the contract or accept less capacity at a proportionally lower fee. According to an earlier announcement, SpaceX entered into a similar agreement with Anthropic as well, which was for USD 1.25 billion per month, also running until 2029. If we assume that these contracts run their full course, this would represent USD 26 billion in annual revenue for the company, whose total revenue last year was USD 18.6 billion. This would provide a very substantial boost to the company’s financial performance.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more