Alibaba: The cloud business is performing well

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

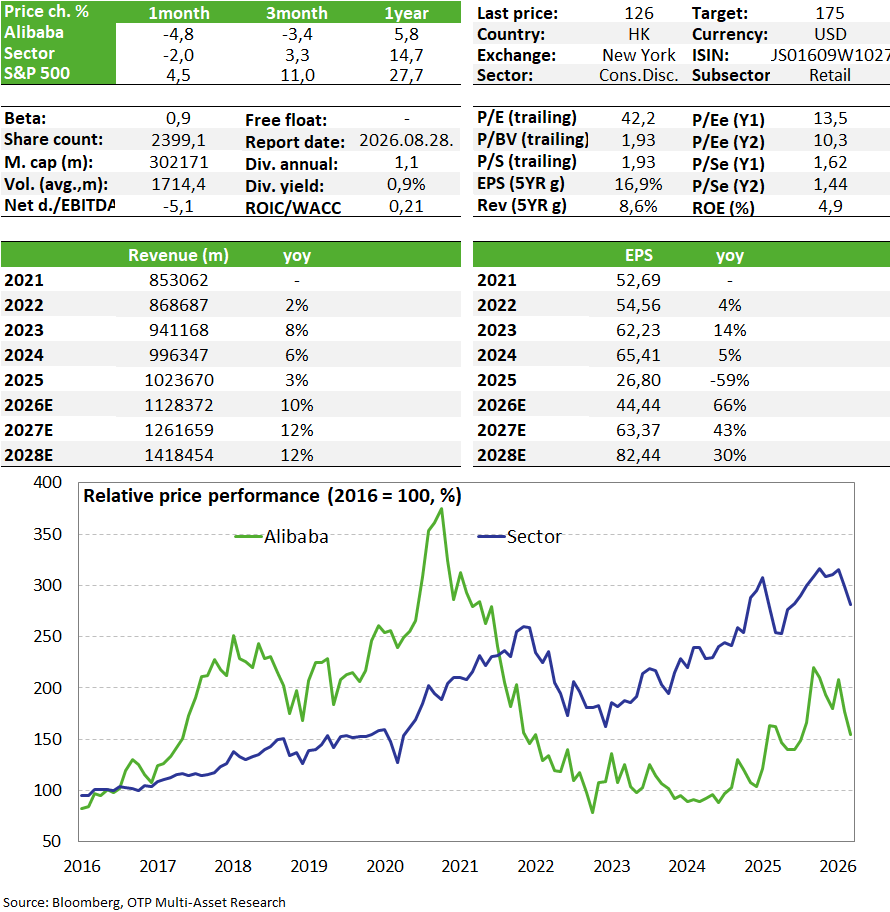

Alibaba released the quarterly earnings report in May that could best be described as mixed, which may be why the stock price has not been able to sustain its initial sharp rise by now. At the time, investors were very pleased with the continued strong growth of the cloud business, driven in part by AI services, which is expected to persist in the coming quarters. However, competition in the Chinese e-commerce market and significant expenses continue to be downward pressures, as does the slowing growth of retail sales, and the May Trump-Xi meeting did not yield any substantive new developments.

Quarterly Report

Alibaba reported revenue of 243.4 billion yuan for the first calendar quarter of this year (which is the company’s fourth fiscal quarter), representing a 2.9% year-over-year increase, falling short of analysts’ expectations of 246.5 billion yuan. The shortfall is primarily attributable to the Chinese e-commerce segment, as revenue in both international e-commerce and the cloud business exceeded expectations. Adjusted for one-time effects (with Sun Art and Intime having been divested in the meantime), revenue shows an 11% increase, which represents strengthening momentum compared to the 9% growth rate in the previous quarter.

The cloud business plays a key role in this, and investors are paying increasing attention to it. Revenue from external users has grown by 40% year-over-year, while revenue specifically related to AI services has been growing at a triple-digit percentage rate for 11 consecutive quarters. This now accounts for nearly a third of the division’s revenue, or 9 billion yuan, but management expects it to account for half of revenue within a year. Alibaba’s large language model, Qwen, has already reached 1 billion cumulative downloads, and the March update to Qwen 3.6 Plus demonstrated significant performance improvements in coding and agent-based programming. Growth continues to depend primarily not on demand (which is abundant) but on the scale of investment spending.

In the cloud business, not only did revenue surge, but so did profitability. Despite rising costs for chips and infrastructure, the company has been able to offset these increases for now through price hikes in a market driven by strong demand, as well as through the growing use of its in-house developed chips. As a result, the margin improved to 9.1%, causing adjusted EBITDA to jump 57% year-over-year. According to the company, these positive trends will continue, and we may even see margin levels exceeding 10% in the coming quarters. This still falls short of the mid-term target of around 20% and the 30–40% margins seen among Western competitors, which is due to increased competition from China and lower prices maintained to gain market share.

In China’s traditional e-commerce market, revenue declined by 1%; this is now a stable, mature, and competitive market where Qwen’s AI solutions (including the introduction of the Shopping Assistant) and services have begun to be integrated into Taobao and Tmall. Within this segment, instant delivery services continue to drive revenue growth, at 57% year-over-year. Competition here is very intense, forcing the company to offer significant discounts and invest in marketing—and thus incur high costs—but the average order value is already rising, and they have begun to place greater focus on non-food products, while customer retention remains strong. Overall, the business unit is expected to work off its losses in the coming year, and by 2027, upon reaching a turnover of 1 trillion yuan, there may be an opportunity for the business to begin generating cash.

If we were to exclude the instant delivery business, the Chinese e-commerce segment’s EBITA would have remained stable on an annual basis. However, since the unit is currently operating at a significant loss, the segment’s overall EBITA plummeted by 40%. All in all, this significantly reduced the company’s overall EBITA by 84%; needless to say, the shortfall relative to the consensus is now very significant. The same is true for net profit, where the company managed to achieve only 86 million yuan compared to nearly 30 billion in the base period, although this was largely due to the revaluation of investments.

Given the company’s substantial spending on AI and the instant delivery market, free cash flow has also declined, with 17.3 billion yuan in cash burn during the quarter. Net cash reserves are thus steadily declining, but even so, there is still 260 billion yuan on hand, which is more than 10% of market capitalization. Overall, the quarterly figures remain weak, but the market appears to be undervaluing the growth potential of the cloud business at current price levels. This could serve as an additional catalyst, as could the business turning a profit in the instant delivery market.

Valuation

The stock’s valuation, based on P/E and EV/EBITDA ratios, is slightly higher than that of its narrower-scope Chinese peers (2026 P/E: 19, EV/EBITDA: 9.8), a level justified by its more dynamic growth profile relative to them. A pricing discount remains compared to overseas companies with similar profiles, which can be partly justified by lower margin-generating capacity and a more diversified business profile, but not entirely. Net cash stands at 12% of market capitalization, but free cash flow generation is currently under pressure from AI-related investments and intense price competition in the instant e-commerce sector. As a result, share buybacks are on hold despite a potential $19 billion buyback program available through 2027 (6.5% of market capitalization). We maintain our fair value estimate, calculated based on key metrics, at $175; however, the prolonged pressure on earnings creates downside risk.

Investment thesis

- Alibaba is China's largest e-commerce company. This division accounts for ~43% of revenue (Taobao and Tmall); in addition, the company holds the largest share of the Chinese cloud services market (Alibaba Cloud), which accounts for 13% of revenue, while international trade services (AliExpress) and logistics services (Cainiao) each account for a similar share.

- The company’s e-commerce segment is capable of achieving modest single-digit percentage growth in normal times due to market maturity and significant competition (JD.com, PDD), but it remains a stable pillar of revenue and profit generation. Monthly active users are at historic highs, while user loyalty remains strong, driven in part by the recently launched instant delivery service. However, intense price competition has emerged in this sector (from JD and Meituan), causing Taobao’s revenues—due to surging volumes—to grow much more dynamically; however, scaling up entails significant cost implications. The ratio of sales and marketing costs to revenue has increased significantly, causing profit generation at the EBITA level to halve on an annual basis.

- The profit growth is primarily in the cloud business, where revenue growth is also more dynamic, and the AI solutions offered to customers here have significant potential (in-house AI: Qwen). Customers are increasingly adopting these services, driving triple-digit annual growth. The company is targeting $100 billion in revenue in this segment over a five-year period, which would imply average annual revenue growth of over 40%, potentially accompanied by high margins exceeding 20%. The market still does not price in this potential for earnings growth (which, of course, is also explained by a more conservative approach).

- Investors continue to view Alibaba as one of the top AI-focused investments in Asia; the company began using its in-house chips to train models this fall (chips whose capabilities are on par with Nvidia’s H20 chips), while the stock remains a significantly cheaper alternative compared to Western AI investments. Alibaba has the largest AI model portfolio in China and is well-positioned to become the leading platform on which developers build applications and AI agents.

- While they are already market leaders in China, they are also expanding into Southeast Asia, the Philippines, Thailand, and South Korea.

- As with other Chinese stocks, the greatest risks stem from the U.S.-China trade war, the threat of delisting from U.S. stock exchanges, and intense competition in the Chinese e-commerce market. Banning the company from the U.S. market is constantly on the agenda in certain U.S. political circles, with the argument that investors should not finance companies linked to the Chinese state and military. While this does not yet translate into a direct loss of business for the company, it could increase the risk premium; the Xi-Trump meeting in the spring did not result in a real breakthrough for either side.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more