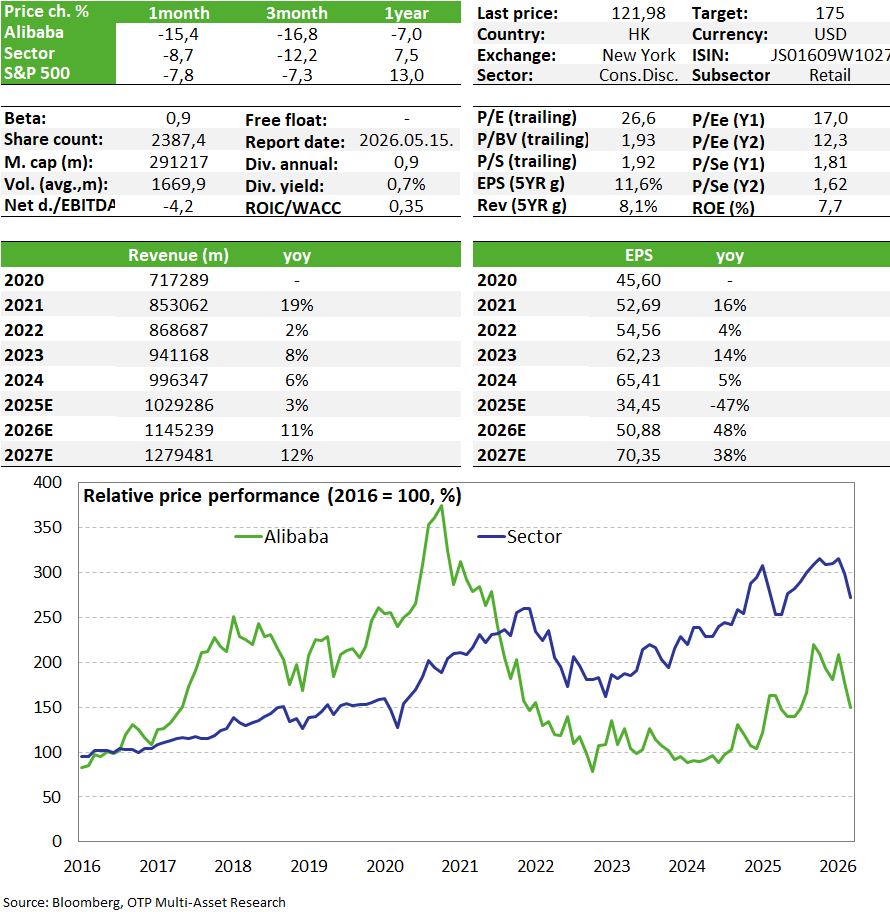

Alibaba: a short-term burden can become a driving force later on

Related content

Honeywell's stock price may be on the verge of a breakout

Major indices began to fall at the end of last week, but the movements were news-driven, and there has been significant volatility, which has resulted in a low number of opportunities indicating a quality breakout for the past two weeks. This week, one of the stocks from our Equity Top Pick List, Honeywell, also ranked high on the momentum list. After a minor pullback, the technical picture could indeed be supportive.

Uber Falls on Negative News

Uber shares failed to follow through on their breakout attempt, and on Friday, negative news concerning the company’s robotaxi business pushed the share price down to the stop-loss level specified in our trading idea.

Alibaba reported quarterly results in March that fell short of expectations; fierce competition in e-commerce continues to weigh on profitability, despite strong performance in the cloud business. Looking ahead, however, the situation may be on a path to gradual improvement, while new launches continue to roll out in AI services, which could represent significant business potential for the coming years. The market still does not price this in at current price levels, so even if heavy capex spending have a negative impact on performance in the short term, the company may be able to outgrow this over time. Moreover, due to the decline in share prices over the past few months, valuation levels are now more favorable, so we are maintaining the stock on our Equity Top Pick List.

Quarterly Report

Alibaba reported quarterly results in March that fell short of expectations across all major metrics, causing its stock price to drop by 7%. Revenue came in at 284.5 billion yuan, compared to the expected consensus of 289.8 billion, representing just 2% year-on-year growth. Excluding the impact of Sun Art and Intime, which were spun off in the meantime, growth would have been 9%. Traditional e-commerce, which accounts for nearly half of revenue, grew by 1%, while the growth of instant services was more significant at 56%. Overall, this core segment delivered the biggest negative surprise.

The company continues to focus on quick commerce, where market competition is fierce and providers are offering significant discounts in an effort to reach as wide an audience as possible. This also explains the 43% decline in EBITA for the segment, which dragged down the company’s overall adjusted earnings (EBITDA) to 34 billion yuan, compared to the expected 39.6 billion. There are signs of positive trends, as Alibaba has been able to increase the average order value month over month, while the integration of the Qwen app also helps the company adapt to users’ diverse needs in a better and more cost-effective way (this contributed to 140 million user interactions during the Chinese New Year holidays). This could also help the company begin to gradually scale back discounts, which could eventually set the segment on a path toward profitability.

In international e-commerce (AliExpress), the company achieved a 4% increase in revenue, but the figure of 39 billion fell short of the expected 41.7 billion. The quarterly loss at the EBITDA level narrowed by half thanks to logistics optimization.

The cloud business, which serves as the company’s driving force and engine for future growth, continued to deliver strong growth that exceeded expectations. Revenue grew by 36%, with AI services continuing to generate triple-digit percentage growth within that segment. They maintain their market-leading position, with a 36% market share in China, and continue their international expansion. In February, Alibaba unveiled its new Qwen 3.5 language model; the open-source model family remains the most widely used in the world (over 1 billion downloads by the start of the year). Mass production of its in-house developed chips has also begun, and the aforementioned Qwen app has received new features that are being integrated into services; as AI assistants, they are capable of coordinating across platforms and performing complex tasks.

The cloud business remains the most profitable segment, with EBITA growing by 25% year-on-year. The company plans to generate $100 billion in revenue in this segment over a five-year period, which would imply an average annual growth rate of over 40%. Given the potential for margins exceeding 20%, this could be one of the most important earnings drivers in the coming years. Although the market is indeed experiencing strong demand, growth of this magnitude appears quite ambitious; therefore, it is likely not yet factored into analysts’ expectations, which increases the potential for positive surprises in the future.

On the bottom lines, goodwill impairment also hurt net profit growth, which fell by nearly 70%, falling well short of expectations (reaching nearly half of them). Since significant capital expenditures are incurred in both the cloud business and instant services, this has so far manifested itself in a decline in free cash flow (which fell to one-third of its previous level), leading to a suspension of share buybacks.

Valuation

The stock’s valuation, based on P/E and EV/EBITDA ratios, is on par with that of its Chinese peers (2026 P/E: 12, EV/EBITDA: 6.3), which, combined with the decline in the share price, represents a significant normalization of valuations in recent months. A valuation discount remains compared to overseas companies with similar profiles, even though valuations of major U.S. technology companies have also declined. Net cash stands at 17% of market capitalization, but free cash flow generation is currently under pressure from AI-related investments and intense price competition in the instant e-commerce sector. As a result, share buybacks are on hold despite a potential $19 billion buyback program available through 2027 (7.5% of market capitalization). We maintain our fair value estimate of $175 based on ratios, but the prolonged pressure on earnings creates downside risk.

Investment thesis

- Alibaba is China's largest e-commerce company. This division accounts for ~43% of revenue (Taobao and Tmall); in addition, the company holds the largest share of the Chinese cloud services market (Alibaba Cloud), which accounts for 13% of revenue, while international trade services (AliExpress) and logistics services (Cainiao) each account for a similar share.

- The company’s e-commerce segment is capable of achieving modest single-digit percentage growth in normal times due to market maturity and significant competition (JD.com, PDD), but it remains a stable pillar of revenue and profit generation. Monthly active users are at historic highs, while user loyalty remains strong, driven in part by the recently launched instant delivery service. However, intense price competition has emerged in this sector (from JD and Meituan), causing Taobao’s revenues—due to surging volumes—to grow much more dynamically; however, scaling up entails significant cost implications. The ratio of sales and marketing costs to revenue has increased significantly, causing profit generation at the EBITA level to halve on an annual basis.

- The profit growth is primarily in the cloud business, where revenue growth is also more dynamic, and the AI solutions offered to customers here have significant potential (in-house AI: Qwen). Customers are increasingly adopting these services, driving triple-digit annual growth. The company is targeting $100 billion in revenue in this segment over a five-year period, which would imply average annual revenue growth of over 40%, potentially accompanied by high margins exceeding 20%. The market still does not price in this potential for earnings growth (which, of course, is also explained by a more conservative approach).

- Investors continue to view Alibaba as one of the top AI-focused investments in Asia; the company began using its in-house chips to train models this fall (chips whose capabilities are on par with Nvidia’s H20 chips), while the stock remains a significantly cheaper alternative compared to Western AI investments. Alibaba has the largest AI model portfolio in China and is well-positioned to become the leading platform on which developers build applications and AI agents.

- While they are already market leaders in China, they are also expanding into Southeast Asia, the Philippines, Thailand, and South Korea.

- As with other Chinese stocks, the greatest risks stem from the U.S.-China trade war, the threat of delisting from U.S. stock exchanges, and intense competition in the Chinese e-commerce market. Banning the company from the U.S. market is constantly on the agenda in certain U.S. political circles, with the argument that investors should not finance companies linked to the Chinese state and military. While this does not yet translate into direct business losses for the company, it could increase the risk premium; moreover, since the Xi-Trump agreement last fall, a de-escalation in the conflict between the two parties has been observed.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more