Albemarle: Well Placed for a Lithium Turnaround

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

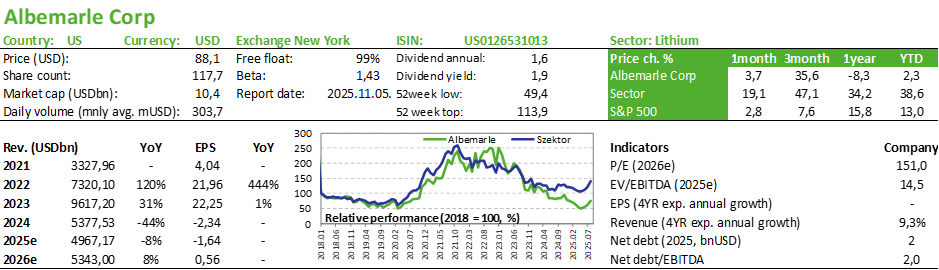

The price of lithium still seems weak, but there has been a slight upturn since June, and industry newsflow has been particularly strong recently. The raw material is mainly used in electric car batteries and energy storage, and demand in both sectors is likely to grow rapidly in the coming years. However, at current prices, a significant proportion of producers are operating at a loss, which does not encourage capacity expansion. In the longer term, therefore, the ingredients for a more sustained turnaround are in place. Albemarle, one of the world's largest and cheapest producers, is in a favorable position to await the market turnaround. Most of the company's production comes from Australia and Chile, its liquidity position is adequate, and its debt level is not high. In addition, the technical picture looks good, so we are opening a trading idea on the company's shares.

Entry: ~85 USD

Stop: 76 USD

Target: 112 USD

Risk/return: ~3

Investment thesis

Lithium is primarily used in electric car batteries and energy storage, which is typically linked to solar and wind energy. According to data from the International Energy Agency (IEA), electric cars accounted for 53% of lithium demand in 2024, while energy storage accounted for 9%. The IEA forecasts that demand in both sectors could grow rapidly in the coming years, with total lithium demand doubling by 2030 compared to last year (with electric cars and energy storage accounting for more than 80% of demand). According to data from Rho Motion, more than 9 million electric cars were sold globally in the first half of this year, representing a 24% increase YoY. Energy storage is also poised for significant growth, as solar and wind energy capacities are growing at a rapid pace. China, for example, recently announced that it would double its current energy storage capacity by 2027, where it is already the largest player globally.

Despite this, the price of lithium remains at a multi-year low (down nearly 90% from its 2022 peak), although there has been a slight increase since June. This is primarily due to oversupply caused by previous high prices. However, the euphoria has turned into a deep depression, with a significant proportion of producers operating at a loss at current prices. In the longer term, therefore, the ingredients for a more sustained market turnaround are in place, although the timing of this is rather uncertain.

Albemarle is one of the world's largest and cheapest lithium producers, accounting for an estimated 22% of global supply in 2023. Most of the company's production comes from the Greenbushes mine in Australia (~48% last year), which is the world's cheapest hard rock mine. The rest of its production comes mainly from Salar de Atacama in Chile (~33%), which is also one of the cheapest sources of lithium. Albemarle not only extracts lithium but also processes it: it has several lithium carbonate and lithium hydroxide production plants in China, Australia, and Chile. The company is also involved in the production of other chemical products and is one of the world's largest bromine producers.

Due to depressed lithium market prices, the company's earnings are currently weak despite being one of the cheapest producers (most of its peers are in an even worse position). However, the Q2 earnings report at the end of July was relatively favorable for Albemarle, beating analysts' expectations. In addition, thanks to previous cost savings and a cutback in investment activity, management expects positive free cash flow this year. The company's liquidity remains adequate (USD 1.8 billion in cash and USD 1.6 billion in credit facilities), its debt level is not high (net debt / EBITDA ratio of 2), and its maturity and interest rate structure is favorable (100% fixed at an average interest rate of 3.6%). Overall, Albemarle is in a favorable strategic position to await the turnaround in the lithium market. The company’s Q3 earnings report will be released after the market closes on November 5.

Technical picture

The Albemarle chart has formed a trend-reinforcing ascending triangle pattern over the last three months. It could open up significant space above 87.5. Since there is a gap (76.34-77.5) open, this could also be a good risk management level. If it were to fill, it would be a sign of weakness and could signal the end of long speculation. We can expect at least two natural levels of rise from the pattern, so the target level could be around 112. In light of this, we are opening a long position, managing the risk at the 76 level and setting the target price at 112. The risk/reward (RR) ratio is ~1:3.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more