Hungary: Lower-than-expected inflation for the third month in a row

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

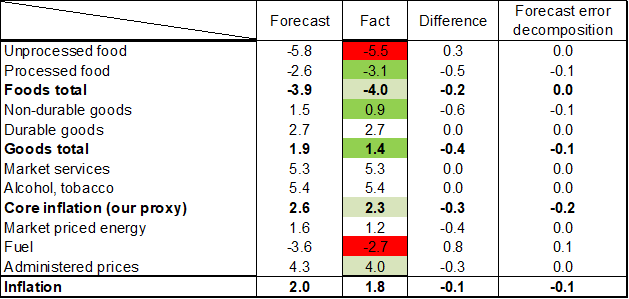

Hungary's headline inflation increased from 1.4% year-on-year in February, to 1.8% in March. The published data came as a surprise as it was lower than both the consensus (2.2%) and our forecast (2%). The downward surprise mostly came from lower-than-expected inflation of non-durable goods and processed food, while fuel prices rose slightly faster-than-foreseen. Core inflation edged down from 2.1 to 1.9%. The March data do not yet reflect the impact of the war in Iran. Even before the sharp increase in energy prices, we expected inflation to reach its annual low in February, followed by a gradual acceleration, driven by fuel prices and the waning disinflationary effect of food prices, although prices in both categories are still declining on a year-on-year basis.

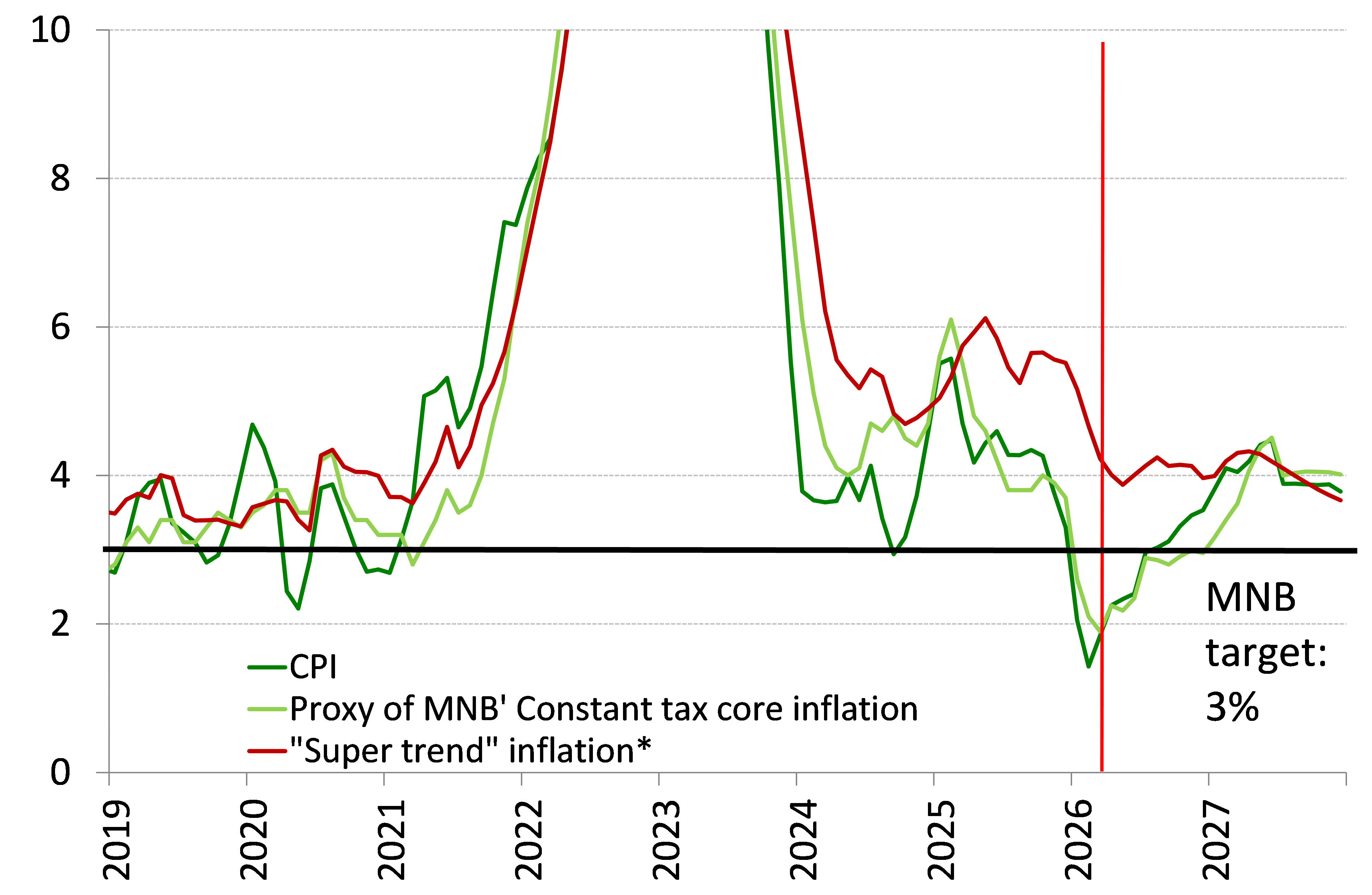

Underlying indicators improved further in March. The MNB’s constant tax core inflation declined from 2.1% to 1.9% YoY, and the sticky price inflation decreased from 4.6% to 4.2% YoY. We should highlight that the MNB’s constant tax core inflation contains some items that were affected by the margin cap measures and it also contains the mainly backward-looking pricing of telecom and financial services, which are also affected by the "voluntary" price freezes proposed by the government. Hence, we think our “super trend” inflation (Chart 9) indicator is the better underlying gauge in the current environment as it does not contain telecommunication or financial services, and it is filtered from the margin cap’s effect, therefore it is not affected by any administrative measures. The annualized MoM change of our trend inflation indicator increased from 1.8% to 2.6%, and the repricing of market services, which is closely watched by the central bank, remained subdued in March. As our "super trend" indicator remained favourable in the first three months of 2026, we can now say with increasing certainty that the inflation risks linked to the 11% minimum wage hike and to the government's consumption-stimulating measures did not materialize, and the strong exchange rate and weak economic growth appear to have brought lower re-pricing at the beginning of the year.

The March inflation data reinforce the view that the effects of the war in Iran are hitting the economy at a point when the inflation situation is relatively favourable. It is important to emphasize that energy prices have the strongest and fastest impact on inflation through fuel and energy prices. In Hungary, household energy prices are regulated, and we assumed that the government would not raise them. Furthermore, the Hungarian government has also capped fuel prices so rising oil prices will have only a limited impact on this product group as well. As a result, the effects of rising energy prices are reflected in inflation in a much less direct and slower manner (rising transport costs, corporate energy prices, etc.). As a consequence, we expect 2.9% inflation in 2026 and the effect of the Iranian war can be around only 0.5ppts in our baseline scenario (with oil prices following the forward price curve). It is also important to note that fertilizers for spring agricultural work are typically purchased in early stages; moreover, the introduction of EU carbon tariffs this year led to increased stockpiling. Furthermore, the European food market is characterized by oversupply in several segments (milk, meat), and grain silos are also at very high levels of capacity. For these reasons, we do not currently expect a drastic price increase similar to that of 2022 in the agricultural products market, which also mitigates the inflationary effects of the war in Iran.

Although March's inflation data was lower both than the market consensus and the MNB’ short-term forecast (1.9%) and there has also been positive news regarding the war in Iran, the central bank will almost certainly wait to make its next interest rate adjustment until it has a clearer picture of the current "risk landscape." A half-hearted ceasefire aside, the extent of the shock to the energy market will depend on how quickly shipping traffic in the Strait of Hormuz can return to normal—which, in addition to the "reopening" of the strait, also depends on the extent of damage to the energy infrastructure of the Gulf states. Furthermore, the central bank will likely wait until it becomes clear how risk premiums will develop following the elections before adjusting the interest rate in either direction. Since we believe that inflation trends are developing favorably, we expect that the central bank will have the opportunity to cut interest rates in the last third to quarter of the year. However, we do not expect more than one rate cut, because, on the one hand, food inflation is contributing very strongly to disinflation this year, but in 2027 we expect this to come to an end, and food inflation will exceed the overall inflation rate; on the other hand, the spillover of second-round inflationary effects will impact 2027 inflation at least as much as it did this year. Risks are huge, further escalation on the Middle East could force the central bank to hike rates, while a fast normalisation on energy markets especially with a market-friendly shift in domestic economic policies could pave the way for more rate cuts.

Inflation forecast (annual changes, %)

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more