OTP Morning Brief: Markets showed subdued activity ahead of a busy week of events

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

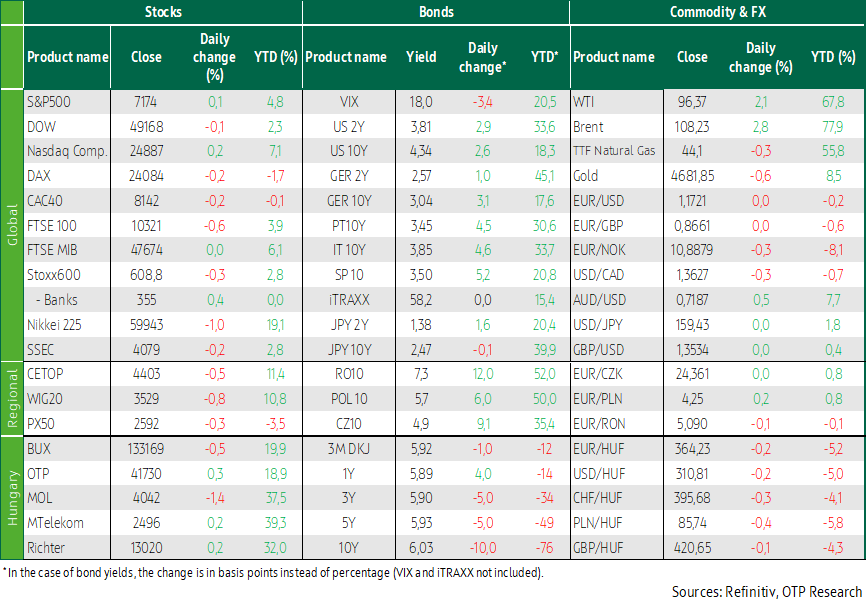

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Stalled negotiations dampened European investors’ risk appetite, leading to a modest decline in the major indices. The negative sentiment also spilled over to the Hungarian market, where MOL shares fell the most. U.S. markets traded sideways following the cancellation of the peace talks, while oil prices rose. Long-term yields edged higher ahead of the Fed’s rate decision on Wednesday, while the decline in domestic yields continued. The Bank of Japan left its policy rate unchanged. Today, attention will be focused on the MNB’s interest rate decision.

European equities declined amid uncertainty stemming from stalled negotiations, with the BUX down by half a percent

European equities edged lower on Monday as investors assessed the stalled negotiations between the United States and Iran, as well as the prospect that disruptions to critical oil supply chains—now ongoing for weeks—are likely to persist. Among the major regional indices, the FTSE recorded the largest decline, falling 0.6%, while the DAX and the CAC 40 slipped by 0.2% each, leaving the Stoxx 600 0.3% lower at the end of the first trading day of the week. Breaking down the Stoxx 600 by sector, banks posted the strongest gains, rising 0.4%, supported by stocks such as Commerzbank (+2.4%) and Santander (+0.8%). On the downside, the technology sector stood out with a 1.3% decline, while the energy sector fell 1.1%, weighed by uncertainty despite the renewed rise in oil prices. Among individual stocks, shares of onshore wind turbine manufacturer Nordex jumped 5.7% after its first-quarter adjusted results exceeded analysts’ expectations.

The CEE region was characterized by the same negative sentiment, with the PX 50 down 0.3%, the BUX falling 0.5%, and the WIG 20 declining by 0.8%. The domestic index was weighed mainly by a 1.4% drop in MOL, while shareholders of the other three blue-chip stocks managed to post modest gains.

U.S. markets traded sideways at the start of an event-packed week, while oil prices rose following the cancellation of the peace talks

The S&P 500 and the Nasdaq recorded modest gains on Monday amid subdued trading, as investors remained cautious at the start of an event-packed week. Market focus later in the week will simultaneously turn to corporate earnings, economic data releases, central bank interest rate decisions, as well as the potential escalation or easing of tensions in the Middle East. As a result, the major indices traded within a narrow range, with the S&P rising 0.1%, the Nasdaq gaining 0.2%, while the Dow slipped 0.1%. Among the S&P 500’s 11 primary sectors, communication services performed the best, while the consumer staples sector posted the largest decline. Verizon shares rose 1.5% after the telecom company raised its full-year guidance on stronger-than-expected subscriber growth. Shares of Domino’s Pizza fell 8.8% after the food delivery chain’s first-quarter sales missed expectations. Nvidia shares jumped 4.0%, extending the previous session’s 4.3% gain and pushing the company’s market capitalization back above USD 5 trillion.

Efforts to revive peace talks between the United States and Iran continued after President Donald Trump decided to cancel the weekend trip of U.S. negotiators to Islamabad, which would have provided an opportunity for another round of in-person discussions. Iran continues to restrict shipments passing through the Strait of Hormuz, and although direct diplomatic talks have been suspended following Trump’s decision, intermediaries say that discussions between the United States and Iran are still ongoing behind the scenes. On Monday, Trump consulted with his national security advisers regarding Iran’s latest proposal, which would postpone negotiations on nuclear issues until after the end of the war. Washington is expected to reject the proposal, however, as the U.S. administration maintains that resolving nuclear concerns has been a priority from the outset. As stalled negotiations weighed on sentiment, Brent crude futures rose by 2.8%, while WTI gained 2.1%.

Long-term yields edged higher ahead of the Fed’s interest rate decision on Wednesday, while the decline in domestic yields continued

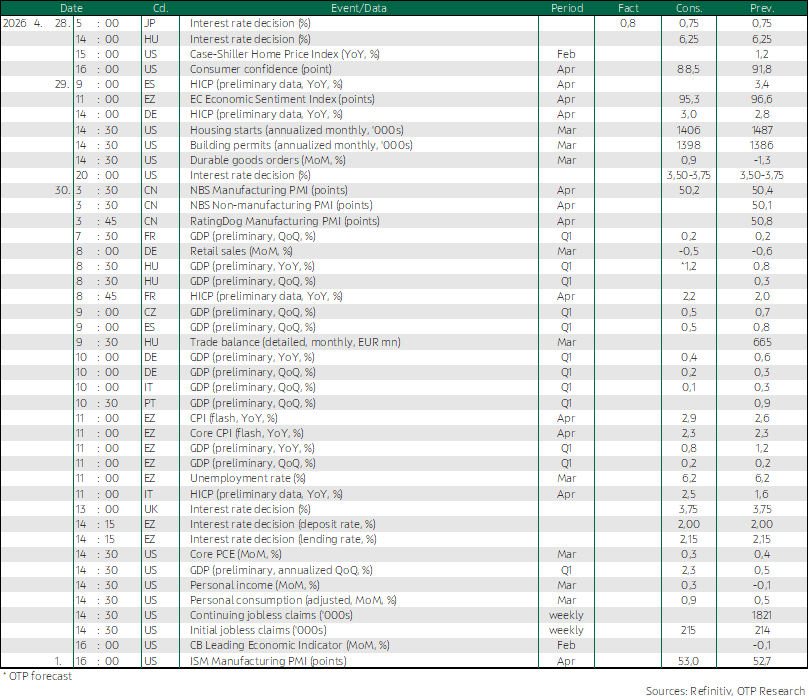

Long-term yields in developed bond markets edged higher on Monday, with the U.S. 10-year yield rising to 4.34% and the German 10-year yield climbing above 3.04%, after no progress was made toward reviving U.S.–Iran ceasefire talks. A heavy slate of economic data due this week is urging investors to remain cautious with respect to rate expectations. At the same time, the Federal Open Market Committee’s two-day meeting, which begins today, is not expected to deliver any surprises, with markets widely anticipating a decision to keep the policy rate unchanged on Wednesday. According to the CME FedWatch Tool, Fed funds futures are pricing in the first rate cut with a higher probability than a hold only at the last meeting of 2027, suggesting that the current 3.50–3.75% rate range may remain in place until then. In the euro area, investors are also preparing for Thursday’s ECB policy meeting, alongside a series of key data releases, including preliminary April inflation figures for both individual member states and the euro area as a whole, as well as first-quarter GDP data. While the ECB is expected to leave rates unchanged at this meeting, market participants continue to expect two 25-basis-point rate hikes in 2026, with a potential third increase toward the end of the year. After modest intraday swings, EUR/USD returned to its Friday level near 1.172 toward the end of the session. In Germany, a consumer confidence index released on Monday deteriorated by more than expected, falling to its lowest level since February 2023.

Yields in the domestic government bond market continued to decline, with benchmark yields falling by 5–10 basis points across maturities beyond one year. The 10-year yield dropped to 6.03% ahead of the MNB’s rate-setting meeting on Tuesday. At Monday’s T-bill switch auction, the planned issuance volume was increased by 15% amid strong demand. The forint strengthened slightly, with EUR/HUF slipping toward the 364 level toward the end of the session.

Today's highlights

The Bank of Japan kept interest rates unchanged at 0.75% on Tuesday, although three members of the nine-member policy board voted in favor of a rate hike, signaling policymakers’ concerns over inflationary pressures stemming from the Middle East conflict. The central bank also significantly revised its price forecasts upward and emphasized the importance of remaining vigilant against the risk of inflation overshooting, pointing to a strong likelihood of a rate increase in the coming months. Following the hawkish-toned statement, the Nikkei fell by 1.0%, while the yen strengthened. Asian markets showed mixed performance overall, with the SSEC down 0.2% and the Hang Seng falling 1.0%, while the Kospi gained 0.6%.

Today, the primary focus will be on the MNB’s interest rate decision. Although Hungary’s risk premium declined sharply following the elections and the forint strengthened, and inflation developments over the first three months of the year were also favorable, we believe the central bank will remain on hold for now and refrain from cutting rates. In addition, U.S. house price data and a consumer confidence reading are due to be released. The earnings season also continues, with companies such as Visa, Coca-Cola and Novartis reporting.

Today, the Government Debt Management Agency (ÁKK) will hold its regular three-month T-bill auction, with an announced issuance size of HUF 30 billion.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more