OTP Morning Brief: It remains unclear whether negotiations between the U.S. and Iran will continue; chipmakers saw a sharp rise on Friday

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

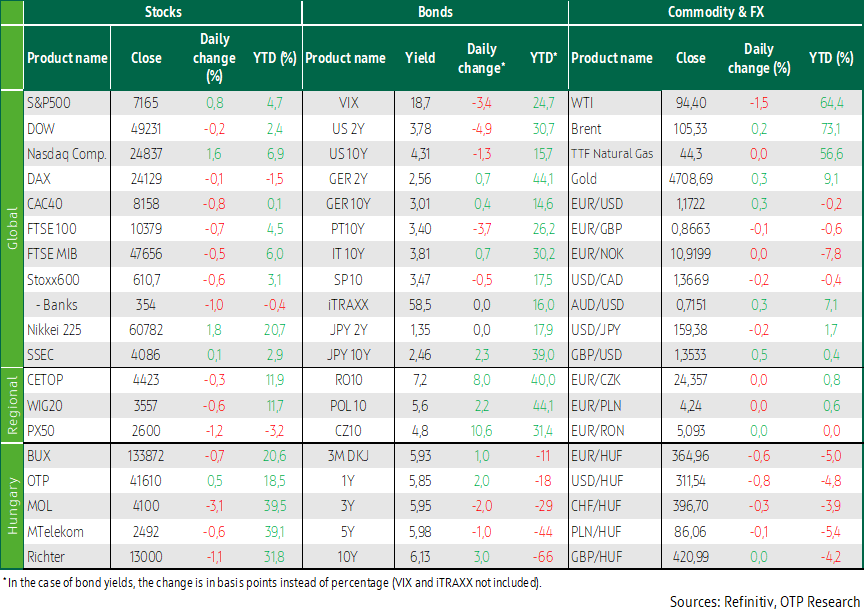

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Over the weekend, Donald Trump canceled his special envoys’ trip to Pakistan to continue negotiations with Iran. On Friday, it was precisely hopes for the resumption of those negotiations, along with Intel’s positive outlook, that drove the S&P 500 and the Nasdaq to new highs. Intel and other chipmakers closed 120% higher amid a rally fueled by optimism surrounding AI-enhanced chips. In Europe, however, investors were more cautious, with crude oil futures surging 15–17% over the week after no agreement was reached on reopening the Strait of Hormuz. Friday’s session did not bring about any significant changes in the bond markets of developed economies, but long-term yields edged higher over the course of the week. The EUR/USD dropped to around 1.172 on Friday, the US dollar gained 0.4% last week. The EUR/HUF fell below 365 on Friday. This week, the BoJ, the National Bank of Hungary, the Fed, the BoE, and the ECB will hold rate-setting meetings, and key interest rates are expected to remain unchanged everywhere. Eurozone flash CPIs for April and Q1 GDP data are scheduled for this week. On Thursday, the Fed’s preferred inflation gauge, the core PCE price index will also be released. In Hungary, the release of the latest GDP figures on Thursday is likely to attract significant attention.

The Stoxx600 closed at a two-week low, with European investors remaining pessimistic about the possible reopening of the Strait of Hormuz in the near future

Most European stock indices dropped on Friday: the unresolved conflict in Iran weighed on market sentiment throughout the week, while crude oil prices continued to climb. On Friday, the Stoxx 600 slipped 0.7% to a two-week low, while the FTSE100 and CA 40 lost about 0.8%, and the DAX edged 0.3% lower. Among Western European stock markets, Spain saw the sharpest decline, with the IBEX closing 1.1% lower. Markets failed to cheer on Friday even Donald Trump’s announcement the previous night, that the Israeli-Lebanese ceasefire would be extended by three weeks. The German IFO economic confidence index, released on Friday, fell more than expected to 84.4 points, to the lowest since May 2020.

Most of the Stoxx600 sector indices closed in the red, with the aerospace and defense sector seeing the sharpest decline. The healthcare and financial sectors also declined considerably; healthcare fell despite its flagship company, Novo Nordisk, rallying by over 5% after rival Eli Lilly’s anti-obesity pill failed to match sales of Novo Nordisk’s oral drug, Wegovy. Among the sectors, technology performed the best, with the sector index driven up in part by SAP’s nearly 5% jump after the German software maker exceeded preliminary expectations thanks to strong demand in its cloud business. Chipmakers also performed well after BE Semiconductor Industries reported strong order volumes and a positive outlook the day before. BESI’s share price jumped 4%, while ASML and ASM International closed around 2% higher on Friday.

Tomra, a Norwegian developer of recycling technologies, was another market mover, after the company plummeted 24% following the release of revenue and earnings figures that fell short of expectations. Swedish technology and industrial group Indutrade plunged 15% after reporting quarterly revenue figures surprising to the downside.

Looking at the week as a whole, Western European indices posted 2–3% losses; rising energy prices (the TTF price surged 14% over 44 EUR/MWh by Friday) do not bode well for European economies that are more vulnerable in terms of energy supply, particularly with regard to inflation and growth outlooks. Among the Stoxx 600 sector indices, the biggest losers — the travel and leisure sector, banks, automakers, and retail — fell 5-6%. Last week, the German Ministry of Economics halved its growth forecast for this year to 0.5%, , and now expects only 0.9% growth for 2027, down from the previously forecast 1.3%.

Stocks in the CEE also dropped on Friday, with the WIG20 edging 0.6% lower, the BUX slipping 0.7%., and the PX declining 1.2%, extending their weekly losses to considerable levels. The WIG20 fell 3.4%, the BUX 3.6%, and the PX 3.7% over the past week. Among Hungarian blue chips, OTP was the only one to edge higher on Friday, while Mol fell just over 3%, Richter lost 1.1%, and MTelekom fell 0.6%.

The S&P500 and the Nasdaq closed at new highs on Friday, with Intel surging as much as 25%

Hopes for a possible resumption of negotiations between the United States and Iran, along with Intel’s announcement, gave a boost to overseas stock markets on Friday, with the S&P500 and the Nasdaq Composite closing at new highs amid the optimistic sentiment. Pakistani government sources reported that Iranian Foreign Minister Abbas Arraqchi was expected in Islamabad to discuss proposals for the resumption of Iranian-American negotiations. White House spokesperson Karoline Leavitt said on Friday that Steve Witkoff and Jared Kushner, as Trump’s special envoys, will travel to Pakistan on Saturda.

The S&P rose 0.8% and the Nasdaq Composite surged nearly 2% on Friday, while the Dow fell 0.2%. The Philadelphia Stock Exchange’s semiconductor index, the SOX, rallied 4.3%, marking its 18th consecutive trading day of gains—a new record. Intel’s stock price jumped 24.5% during Friday’s trading, ultimately closing up 20% at a record high of $82.54, after the company released a better-than-expected sales forecast for the second quarter, providing further fuel for the chipmakers’ rally. Among its competitors, AMD jumped 24% and Texas Instruments soared 20.6%, while Nvidia rose just over 3%. Broadcom edged 4% higher, and Qualcomm and Micron Technology jumped 9%. As a result, the S&P technology sector index posted a 2.5% gain, making it the day’s top performer. The cyclical consumer goods, telecommunications, materials, and utilities sectors also strengthened. The healthcare sector saw the sharpest decline.

Looking at the week as a whole, the S&P500 closed slightly higher amid a hectic market environment, while the Nasdaq posted a near 2.5% gain, with Friday’s rally providing the most of the weekly gains. The Dow fell 0.4% for the week as a whole.

Crude oil prices rose again on Friday, although the two benchmarks showed mixed results at the close: The Brent added 0.2%, while WTI fell 1.5%. For the week as a whole, double-digit gains held, with Brent futures rising nearly 17% and WTI futures surging more than 15%.

Long-term yields in the developed bond markets remained flat following volatile trading on Friday, while the EUR/USD edged over 1.17. In the Hungarian government bond market, we saw moderate but mixed movements, and the EUR/USD fell below 365

Ten-year benchmark yields in developed economies closed near their previous day’s levels on Friday, although trading in the US Treasury market was volatile during the day. Attention remained focused on events in the Middle East after it emerged that peace talks between the United States and Iran could take place over the weekend, boosting optimism that the conflict could soon subside. Investors viewed it as another positive sign that US Attorney Jeanine Pirro announced the Department of Justice is closing its investigation into cost overruns incurred during the Federal Reserve’s renovation work under Chairman Jerome Powell. The price of WTI moderated during the course of Friday, which also provided cause for optimism. Thus, on Friday, the US 10-year yield closed at 4.31%, while the German 10-year yield stagnated near 3.0%. The euro strengthened slightly against the dollar.

Throughout the week, events in the Middle East continued to dominate the FX and the bond markets; long-term yields rose significantly, with the US and German 10-year yields climbing by 7 and 4 bps, respectively, while the US 2-year yield rose nearly 8bps, and the two-year Bund yield surged 14 bps, reflecting short-term interest rate expectations. Over the course of the week, the dollar strengthened slightly against the euro, with the EUR/USD pair edging closer to the 1.17 level.

In Hungary, the yield curve steepened over the course of the week, following volatile trading. For maturities shorter than ten years, the post-election decline was maintained, and yields even fell further; for the ten-year and longer maturities, benchmark yields mostly rose. The 10-year yield benchmark closed at 6.13%, which is still significantly below the pre-election level. The forint closed slightly stronger at 365 on Friday, but over the week as a whole, the Hungarian currency weakened 0.9% against the euro.

Today's highlights

Asian stock indices are trading in positive territory on Monday morning. The Nikkei rose 1.7% to a new all-time high. The Japanese stock market was driven by optimism regarding AI and the resolution of the Iran conflict on Monday, following Friday’s record closes in US indices. The Nikkei briefly turned negative shortly after the opening, but then began to rise sharply after Axios reported that Iran had presented a new proposal to the United States to end the war. The Shanghai Composite, the CSI300, and the Hang Seng edged up 0.2%. Korean benchmarks are all showing gains of over 2-3%. Stock index futures point to a mixed opening in both European and US markets.

Crude oil prices continued to rise on Monday morning after Trump canceled Witkoff and Kushner’s trip to Pakistan on Saturday, prompting the Iranian foreign minister to leave Pakistan on Sunday without holding any talks. Following Monday’s opening, WTI and Brent prices jumped 2%, later easing to 1%. A shooting occurred at a gala dinner for White House correspondents on Saturday; according to reports, the perpetrator’s target may have been Donald Trump. No one was injured in the attack, and the assailant was apprehended.

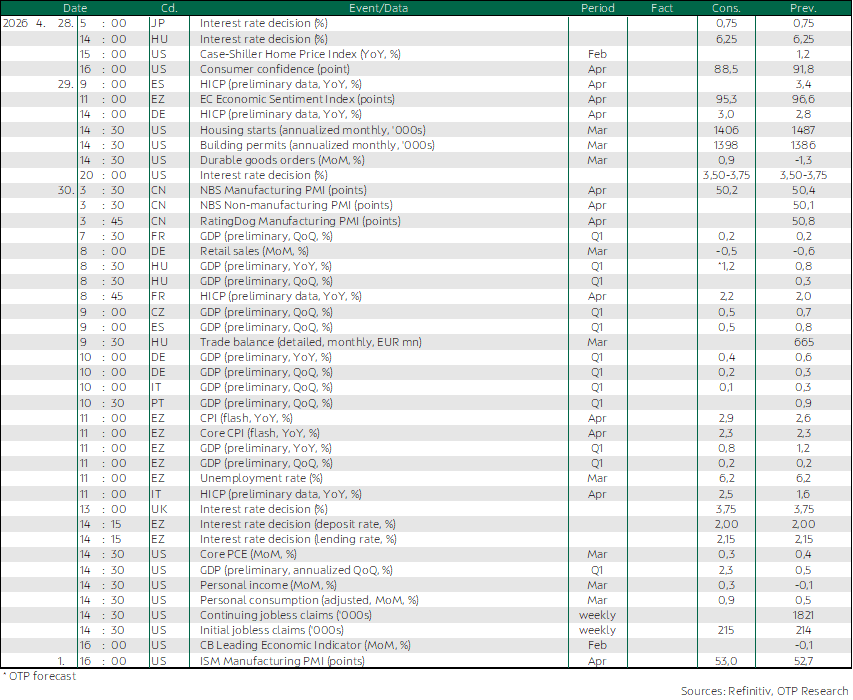

No major macroeconomic data is scheduled for release today, but the rest of the week promises to be all the more exciting. On the monetary policy front, the first event to watch is the Bank of Japan’s meeting on Tuesday, where the policy rate is not expected to change—a sentiment that also applies to the Hungarian National Bank’s interest rate decision a few hours later. Although the Hungarian risk premium fell sharply and the forint strengthened following the elections, and inflation also developed favorably in the first three months of the year, we believe the central bank will hold off on cutting rates for now.

On Wednesday, the FOMC’s interest rate decision will be in the focus, and markets are most likely pricing in a hold on interest rates. On Thursday, the Bank of England and the ECB will announce their interest rate decisions just over an our hour apart; both central banks are expected to keep rates unchanged.

In addition to interest rate decisions, a number of key economic indicators will be released during this shorter week in Europe due to the May 1 holiday: April flash CPIs and Q1 GDP growth statistics will be released by several eurozone member states, and these figures for the eurozone as a whole will also be published on Thursday. In addition, the Commission’s sentiment index, German retail sales data, and eurozone unemployment figures may also be worth watching this week.

In the US, apart from the interest rate decision, Thursday’s release of the core PCE price index could be particularly market-moving, and statistics on household income and spending released later in the day may also be in the spotlight. In addition, a number of economic indicators will be released throughout the week, including the consumer confidence index on Tuesday, durable goods orders on Wednesday, and the ISM index on Friday.

In Hungary, in addition to the MNB’s interest rate decision on Tuesday, we will get the Q1 GDP data and the March foreign trade balance statistics on Thursday.

The corporate earnings season is also picking up steam, with Wednesday expected to be the busiest day of the week, when Alphabet, Microsoft, Amazon, and Meta will all release their quarterly results after the market closes. There is also great anticipation ahead of Apple’s earnings report following Thursday’s market close. In Europe, Novartis, Airbus, AstraZeneca, BP, TotalEnergies, Santander, UBS, and Deutsche Bank, among others, will report this week.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more