OTP Morning Brief: News of the ceasefire extension came after the market close

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

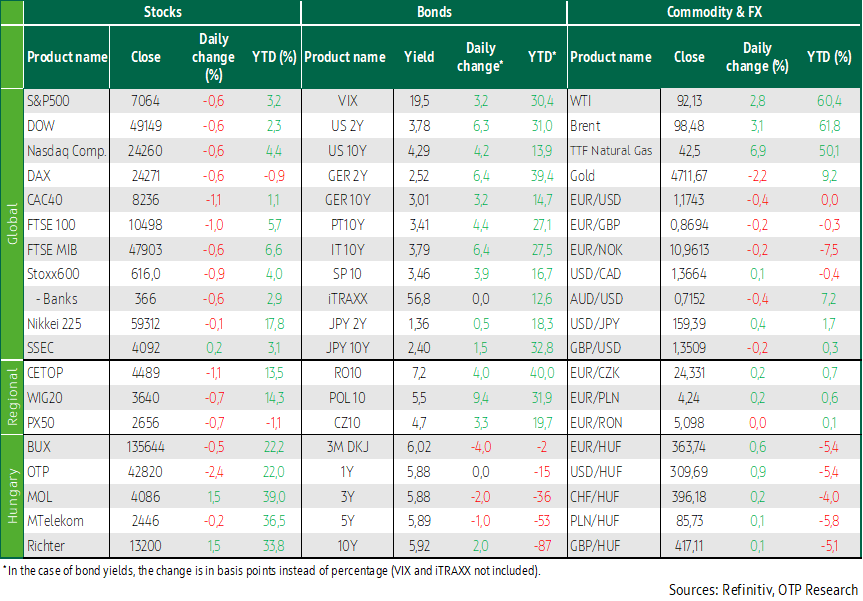

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Amid geopolitical uncertainties, European equities declined, economic sentiment deteriorated sharply in Germany due to the war, while unemployment fell in the United Kingdom. The BUX also fell, led by OTP. Trump unilaterally extended the ceasefire with Iran, but the announcement came only after the market close, sending U.S. indices lower. Several favorable macroeconomic data releases were published for the United States. At his hearing, Warsh emphasized central bank independence, while the decline in domestic yields continued. Asian markets also declined. Today the earnings season continues, while developments in the Middle East will be worth monitoring.

Amid geopolitical uncertainties, European equities declined, while economic sentiment deteriorated sharply in Germany due to the war

European stocks fell on Tuesday as uncertainty surrounding peace talks between the United States and Iran prompted investor caution, just hours before the planned expiration of the ceasefire. The pan-European STOXX 600 index closed down 0.9%, while major regional markets also weakened: France’s CAC 40 and London’s FTSE 100 each fell 1.1%, while Germany’s DAX declined by 0.6%. The aerospace and defense sector led losses, plunging 4.8% to post its biggest one-day drop since April 2025. Europe’s largest defense technology company, Thales, fell 6% after first-quarter sales missed expectations. Aircraft engine manufacturers Safran and Rolls-Royce both dropped more than 6.5%. Healthcare stocks also weighed on the index, with the sector down 2% overall. Novo Nordisk, the maker of Wegovy, slid 4.2%, while AstraZeneca and GSK each suffered losses of more than 2.5%.

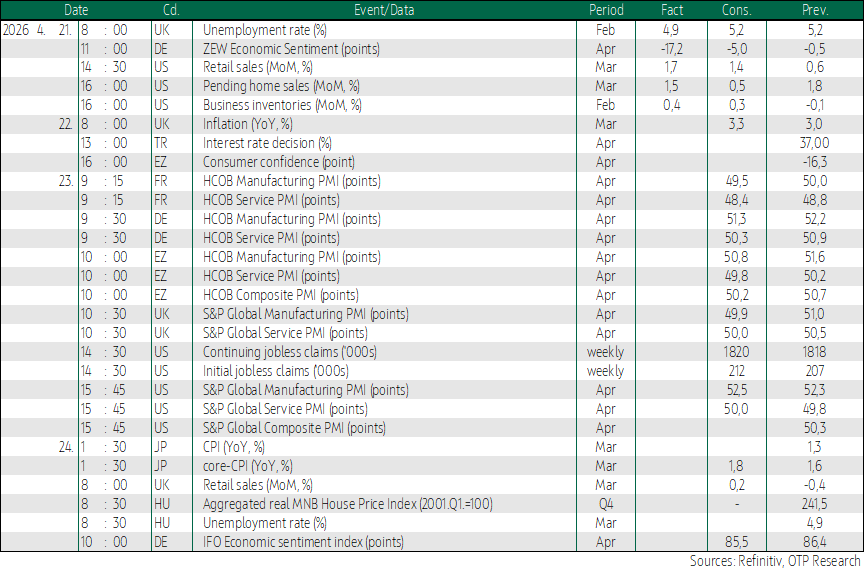

Germany’s ZEW economic sentiment index plunged by 16.7 points to -17.2 in April 2026, marking its lowest level since December 2022 and coming in well below the market expectation of -5. The sharp decline, which represented the third-largest monthly drop in the history of the index following the fall in March, reflects rising pessimism as the escalating conflict in the Middle East weighs on Germany’s economic outlook. Meanwhile, the UK unemployment rate fell to 4.9% in the three months to February 2026, defying expectations of stagnation at 5.2%. The decline in unemployment coincided with an increase in economic inactivity, suggesting that some Britons are opting to leave the labor force rather than continue searching for work.

The decline was mirrored across the CEE markets, with both the PX50 and the WIG 20 down 0.7%, while the BUX fell by around half a percent. The drop was led by OTP, which lost 2.4%, while MOL and Richter both managed to post gains of around one and a half percent.

Trump extended the ceasefire with Iran for an indefinite period, U.S. stock markets fell, and macroeconomic data came in stronger than expected

Developments in the Middle East remain in focus. The two-week ceasefire was set to remain in effect until Wednesday evening, while the outcome of the talks in Pakistan remained uncertain after Trump once again threatened Iran with intensified bombardment, and the Iranian side did not even confirm its participation in the negotiations. The turning point came on Tuesday evening after the U.S. market close, when Trump extended the ceasefire with Iran for an indefinite period, just hours before its planned expiration, to allow the two countries to continue peace talks. Trump said he had extended the ceasefire that came into force two weeks ago until Iran submits its proposal and the negotiations are concluded, one way or another.

As the positive news failed to arrive in time, overseas investors were marked by heightened uncertainty and pessimism, leading major indices to close lower: the Dow Jones, Nasdaq and S&P 500 each fell by 0.6%. The S&P 500 energy sector index rose by 1.3%, the only gainer among the major S&P sectors, as oil prices jumped again amid heightened tensions in the Middle East. UnitedHealth shares surged 7% after the healthcare conglomerate raised its full-year profit forecast and beat Wall Street expectations in the first quarter, providing the largest support to the Dow during the session. Apple shares also came into focus, falling 2.5% after the company announced that CEO Tim Cook would hand over leadership to long-time hardware chief John Ternus.

Several U.S.-related macroeconomic data releases were published yesterday. U.S. retail sales jumped by 1.7% in March 2026, beating market expectations of 1.4% and the upwardly revised 0.7% increase recorded in February. This marked the strongest expansion since March 2025, driven largely by a record 15.5% surge in gasoline station revenues. At the same time, the data excluding fuel and motor vehicle sales also showed no sign of slowing compared with the previous month. Pending home sales likewise exceeded analyst expectations, rising 1.5% month on month. The February business inventories report also delivered a positive surprise, increasing by 0.4% compared with January after three months of stagnation.

Oil prices rose ahead of the ceasefire extension, with Brent climbing 3.8% to move back above USD 99 per barrel, while WTI gained 2.8%.

At his hearing, Warsh emphasized central bank independence, while the decline in domestic yields continued

Long-term yields rose across developed bond markets, with the German 10-year yield climbing above 3% (+4bp), while the U.S. 10-year yield increased by nearly 5bp to close the day at around 4.3%. The two-year yield jumped by 7bp on Monday, pushing expectations for interest rate cuts further out; according to the CME FedWatch Tool, markets are now pricing in the first 25bp Fed rate cut for October 2027. Fed chair nominee Kevin Warsh emphasized during his congressional hearing that he would make monetary policy decisions independently of advice or pressure from President Trump, adding that success in maintaining low inflation could serve as a “shield” protecting the central bank from criticism. As expectations for a potential rate cut were pushed further back, the dollar strengthened, with EUR/USD falling 0.4% to 1.174.

In the domestic bond market, yields continued to decline at maturities below 10 years, while the long end of the curve edged slightly higher, according to secondary market data from the Government Debt Management Agency (ÁKK). Today’s ÁKK auction was successful, with bids exceeding HUF 150 billion submitted for the announced HUF 30 billion quota, of which the issuer accepted HUF 88 billion. The average yield came in at 6%. Meanwhile, the forint traded close to the 361 level against the euro for most of the day, but strengthened sharply in the evening, with EUR/HUF jumping to around 365 (+1.0%).

Today's highlights

The MSCI index tracking Asia-Pacific equities excluding Japan fell by 0.5% after reaching a seven-year high on Tuesday. Meanwhile, Japan’s Nikkei index declined by 0.1%.

Today, the UK will release its March inflation data, while April consumer confidence figures for the euro area are due, and a monetary policy decision is expected in Turkey. In addition, earnings reports are anticipated from companies including Tesla, Philip Morris, IBM, and Boeing.

Today, a six-month Treasury bill auction will be held with a HUF 30 billion issuance limit, while the ÁKK will also conduct two bond auctions worth HUF 15 billion each.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more