OTP Morning Brief: Market sentiment has deteriorated, the Middle East standoff remains unresolved

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

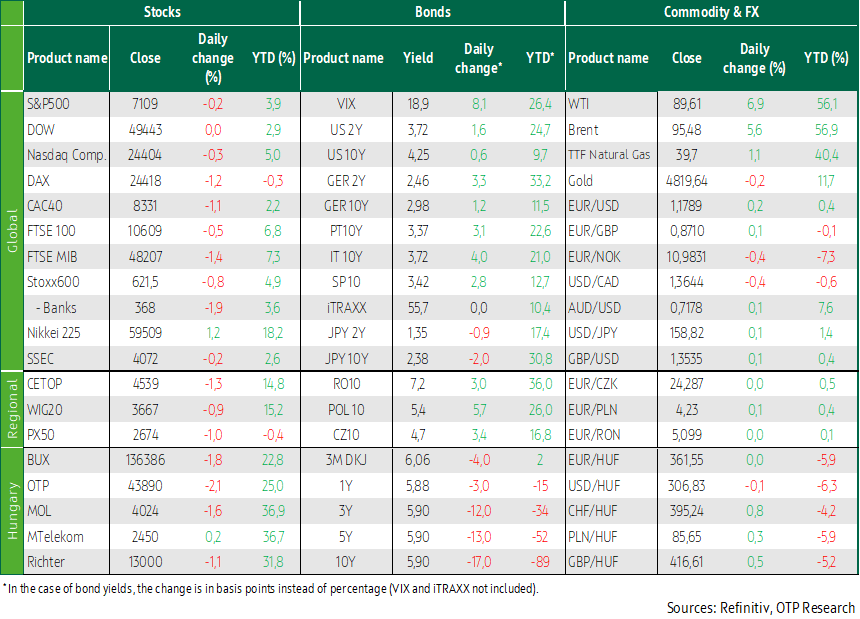

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

The reopening of the Strait of Hormuz proved to be short-lived, crude oil prices surged again on Monday, with inflation fears and growth concerns getting back into focus. Sentiment weakened in equity markets, with European stock indices and most major overseas benchmarks also declining. The BUX underperformed its regional peers. Bond yields moved sideways across developed economies, while the EUR/USD climbed near 1.18. In the Hungarian bond market, the yield decline that began after the elections continued, with the ten-year yield falling below 6%, while EUR/HUF stagnated at around 361.5. In Europe, the German and euro area ZEW economic sentiment index will be today's highlights, while in the US, the March retail sales data are expected to be released. Although the earnings season is underway and a number of key macroeconomic data releases are coming out, the Middle East stalemate remains in the focus, as the two-week ceasefire is set to expire on April 22.

Friday’s momentum quickly faded, with European stock indices declining on Monday

Most Western European stock markets dropped on Monday after the reopening of the Strait of Hormuz had lifted equity indices on Friday. However, developments in the Middle East over the weekend once again put pressure on equity markets, with investors turning more risk-averse as the end of the previously agreed two-week ceasefire approaches. According to Reuters, Iran is considering whether to take part in the Pakistan-mediated peace talks, a senior Iranian official said, after Islamabad attempted to lift the U.S.-imposed blockade on Iranian ports, which had been a major obstacle to Iran’s return to the peace process. Meanwhile, the Strait of Hormuz remains unsafe for navigation after Iranian gunboats opened fire on Saturday at two oil tankers transiting the strait, citing alleged violations by the United States of the agreement through its blockade of Iranian ports. In response to the attacks on the vessels, Donald Trump threatened to take out all of Iran’s power plants and bridges. In a statement on Monday, Trump said it was “highly unlikely” that the two-week ceasefire with Iran would be extended unless an agreement is reached before its April 22 expiration. The US president added that the Strait of Hormuz would remain closed until a deal is in place, Bloomberg reported.

The pan-European Stoxx600 fell 0.8% on Monday, while other major regional markets also declined: the CAC 40 and the DAX both declined 1.1%, while the FTSE 100 slipped 0.6%. Considering the Stoxx600 sector performances, the energy sector was Monday's winner, with BP, Shell and TotalEnergies climbing by 2–3%. The biggest losses were seen in the travel and leisure sector, Friday’s top performer, which dropped by 2.4%. The defense sector also underperformed, with Rolls-Royce and Safran posting losses of close to 4%. Banks and luxury goods manufacturers also dropped considerably. Among individual stocks, engineering company Renishaw rallied 6% after raising its 2026 revenue and earnings forecasts. Logistics company Loomis fell 5% after Goldman Sachs downgraded from buy to neutral.

Just as the BUX posted the strongest gain among key equity indices in the CEE region last Friday, it suffered the largest decline on Monday, falling 1.8%, while the WIG20 slipped 0.9% and the PX dropped near 1%. Among Hungarian blue chips, only Magyar Telekom edged higher (+0.2%), while the other stocks posted 1–2% losses.

The tide also turned in overseas markets, with crude oil prices jumping by 6–7% on Monday

On Monday, major overseas stock indices closed moderately lower following Friday’s highs: the Dow lost a few points, the S&P 500 slipped 0.2%, while the Nasdaq Composite fell 0.3%. In contrast, the Russell 2000 continued to strengthen (+0.6%), reaching a new record high. In terms of sector performances, materials and the financial sector lead gainers among the S&O500 sectors during Monday’s trading session, while telecommunications saw the largest decline. Meta lost 2.6% on Monday, closing in the red for the first time in nine days. Netflix also ended the day down 2.6%, and has fallen by 12% since last week’s earnings release and the announcement of co-founder Reed Hastings’ departure. Building materials distributor TopBuild surged nearly 20% after construction materials supplier QXO agreed to acquire the company in a USD 17 billion deal. Shares of QXO fell 3%. Apple added 1%, after the company named longtime hardware boss John Ternus as its next CEO. Current CEO Tim Cook will stay on as executive CEO from September 1.

Alongside developments related to the Strait of Hormuz, earnings reports are also in focus: 48 companies in the S&P 500 had released their quarterly results until last Friday, nearly 90% of which exceeded analysts’ expectations, according to LSEG data.

Crude oil futures surged 6–7% on Monday, pushing Brent above USD 95 per barrel, while WTI settled just below USD 90 by the end of the session. Following Friday’s 9–11% jump in oil prices, the latest move came after the US Navy intercepted an Iranian vessel over the weekend, after Tehran opened fire on ships, reasserted control over the strategically important waterway, and then closed it again, accusing Washington of violating the ceasefire set to expire this week. The European TTF gas price rose 1% by the end of the day to around EUR 40/MWh, although it had been up as much as 11% during Asian trading hours on Monday morning. The Middle East standoff threatens to worsen the global energy crisis, as a route vital for oil and gas shipments has been largely cut off.

Long-term bond yields in developed economies remained close to their Friday levels, while yields continued to decline in the Hungarian market, with the EUR/HUF falling to 361.5

Long-term yields in developed economies did not move significantly from their Friday levels during Monday’s session, as inflation concerns remain elevated and the outcome of the US–Iran conflict is still uncertain, with a stalemate over the Strait of Hormuz persisting ahead of the April 22 expiration of the two-week ceasefire. The German 10-year yield closed at 2.98%, while the US 10-year yield closed at 4.25%. The EUR/USD closed near 1.18 yesterday, reflecting a further slight euro appreciation compared to Friday. The ECB will hold its next rate-setting meeting at the end of the month, though interest rates are expected to remain unchanged at that meeting. Attention is therefore shifting toward the June meeting, although developments in the Middle East could still alter the outlook. On Friday, the IMF said it expected the ECB to raise interest rates by around 50 bps in 2026 in order to maintain a neutral monetary policy stance.

While long-term yields rose across the region in line with global sentiment, yields continued to decline in the Hungarian market. The 10-year benchmark yield fell by 17 basis points to 5.9%, while EUR/HUF remained stuck at 361.55, its lowest level since February 2022. Since the elections, the domestic currency has strengthened by 3.6% against the euro and by 4.2% against the dollar. The Hungarian 10-year yield has dropped a total of 65 bps over the past week.

Today's highlights

In equity markets across the Asia–Pacific region, indices reflect mixed sentiment ahead of the closing bell: the Nikkei and the Hang Seng edged moderately higher, while the Shanghai Composite and the CSI 300 slightly dropped. Crude oil prices fell 1% this morning.

Equity index futures are currently pointing to a positive opening for the major overseas markets, while a mixed open is expected in Europe.

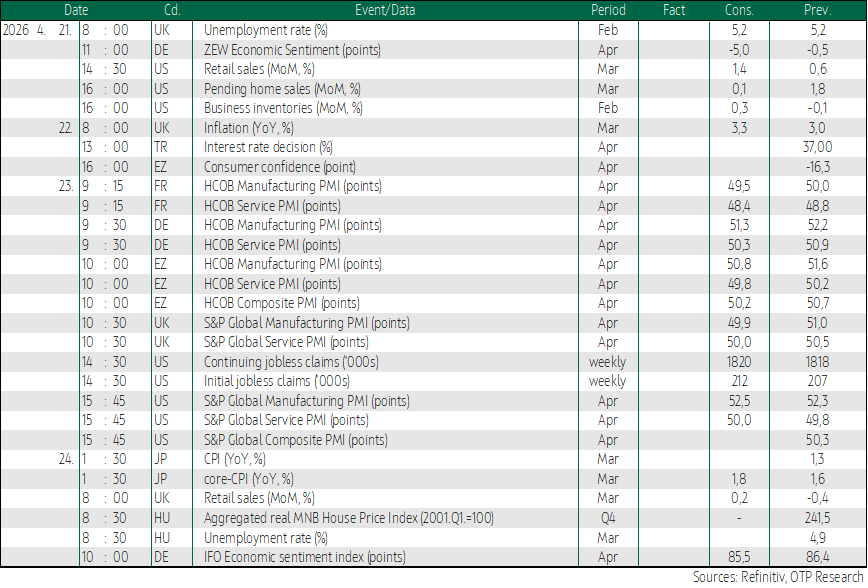

Today, the April ZEW economic sentiment indices for Germany and the euro area as a whole will be released, which, according to expectations and in line with the uncertainty caused by the Middle East conflict, could show a sharp decline. From the United States, March retail sales data are due, which are very likely to show a strong increase compared with the previous month, not necessarily because of stronger underlying consumption, but rather due to higher fuel prices, as the national average price of gasoline has exceeded USD 4 per gallon for the first time in a long while, and the upcoming data are not adjusted for inflation.

Today, among others, UnitedHealth, Interactive Brokers, defense company Northrop Grumman, 3M, United Airlines and Halliburton are scheduled to report earnings in the US, while in Europe, Thales, ASM International, Lonza Group and Beiersdorf are expected to release earnings figures.

Investors are also likely to closely watch today’s Senate hearing of Kevin Warsh, the nominee for Chair of the Federal Reserve. Warsh is generally viewed as more dovish than the current chair, Jerome Powell, whose term expires in May.

The Government Debt Management Agency (ÁKK) will auction three-month Treasury bills today, with a total value of HUF 30 billion.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more