OTP Morning Brief: Hungarian government bonds sold well, with the 10-year government bond yield approaching 6%

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

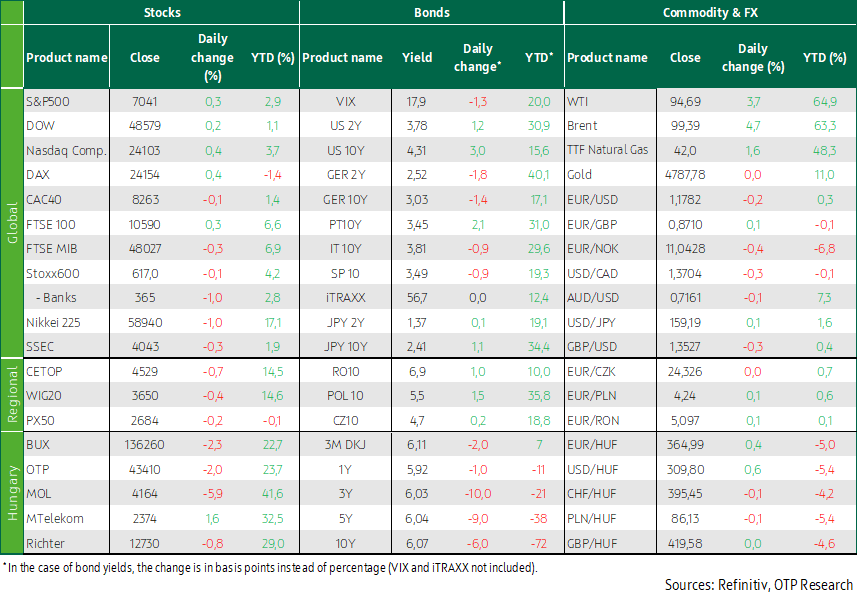

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

After the initial momentum, Western European markets closed in near-stagnation; the BUX and the region also weakened. The initial market rally was driven by news of the expected continuation of U.S.–Iran talks. However, the early momentum ultimately faded, resulting in a mixed close. Oil prices rose as market uncertainty increased over whether the peace talks could resolve supply disruptions in the energy markets in the short term. Overseas stock markets continued to rise from Wednesday’s record levels, helped in part by the ceasefire between Israel and Lebanon announced in the afternoon. There was minimal movement in the international bond market; however, the domestic 10-year yield fell to close to 6%, a level not seen since the outbreak of the Iran war, while the Government Debt Management Agency (ÁKK) sold HUF 200 billion worth of government bonds. Today, February wage data will be released domestically, and it remains advisable to closely monitor news related to Iran.

After the initial momentum, Western European markets closed mixed; the BUX and the region also weakened

Western European equity markets closed mixed on Thursday, as investors assessed potential progress toward a resolution of the Middle Eastern conflict alongside the ongoing corporate earnings season. Optimism grew that the war involving Iran may be approaching its end; however, Tehran indicated that the fate of its nuclear program remains unresolved, and the indices ultimately failed to hold on to their initial stronger gains.

The pan-European STOXX 600 fell by 0.1%. The index came close to recouping the losses suffered since the outbreak of the conflict, but ultimately closed below its late-February level. At the same time, concerns persisted over the extent to which a sustained rise in oil prices could weigh on the European economy, which is heavily dependent on imported energy. Among sectors, technology and energy provided support to the index: the former rose by 1.5%, while the latter gained 0.7%. Software stocks advanced, with Germany’s SAP jumping 3.5%, while Dassault Systemes and Capgemini climbed by more than 2.5%. On the negative side, financial stocks dragged the benchmark sharply lower, contributing to a 1% decline. Defense stocks fell by 1.8%, with Safran and Rolls-Royce closing down 3.4% and 2.4%, respectively. The travel and leisure sector also came under pressure: Ryanair plunged 6.4%. Germany’s Lufthansa became the first major airline forced to cancel flights due to high jet fuel prices, while UK-based easyJet reported that bookings were running below last year’s level. Lufthansa shares fell 3.4%, while easyJet dropped 5%. Among individual stock moves, Barry Callebaut stood out, with its shares plunging 15.6% after the Swiss chocolate maker downgraded its full-year operating profit outlook. By contrast, gambling company Entain’s shares rose 6% after it reported a 3% increase in first-quarter net gaming revenue.

Amid surging oil prices, the German government has halved its growth forecast for 2026 and also cut its growth outlook for 2027, while raising its inflation projections, a source told Reuters.

According to the minutes of the ECB’s March meeting, the war in the Middle East has materially increased uncertainty, posing upside risks to inflation while creating downside risks to economic growth. Although short-term inflation prospects were revised significantly upward, policymakers continue to expect inflation to stabilize around the 2% target over the medium term. In this environment, maintaining interest rates and preserving a meeting-by-meeting, non-pre-committed approach was deemed a prudent decision.

Stock markets in Central and Eastern Europe weakened: the BUX fell by 2.3%, the WIG20 declined by 0.4%, while the PX50 slipped by 0.2%. Domestic blue chips remained broadly under pressure: MOL dropped 5.9%, OTP fell 2%, and Richter declined by 0.8%, all of which contributed materially to the BUX’s downturn, while Magyar Telekom’s 1.6% gain was only able to partially offset the index’s decline.

Peter Magyar, the prospective prime minister, held talks with MOL’s management yesterday and announced afterward that the capped fuel price would remain in place in Hungary even after the new government is formed.

Overseas stock markets continued to rise from Wednesday’s record level

Overseas stock markets continued to rise from Wednesday’s record level, with the S&P up 0.3%, the Dow gaining 0.2%, and the Nasdaq advancing 0.4%. Mild optimism was bolstered by the late-afternoon announcement of a ceasefire agreement between Israel and Lebanon, which raised hopes that the worst phase of the Middle Eastern conflict may be over. Meanwhile, investors reacted to mixed macroeconomic data and corporate earnings reports. The strongest gains were seen in the energy (+1.5%) and real estate (+1%) sectors, while healthcare (-0.8%) was the weakest performer.

Among the macroeconomic data, the number of new unemployment benefit claims fell by more than expected last week, indicating that labor market conditions have remained stable, even though companies remain cautious about expanding their workforce as the war with Iran puts pressure on the economy. Industrial production declined by 0.5% month on month in March.

Meanwhile, the earnings season is in full swing. U.S. beverage maker PepsiCo rose 2.3% after beating expectations for quarterly profit. Medical device manufacturer Abbott fell 6%, dropping to its lowest level since November 2023 after the company cut its full-year profit forecast, while brokerage firm Charles Schwab also weakened by 7.6% following the release of its earnings report. After closing the regular trading session unchanged, Netflix shares fell 8% in after-hours trading after the company published its quarterly results. The streaming service left its 2026 revenue guidance unchanged and also announced that co-founder Reed Hastings will step down from the company in June.

Software stocks rose by 1.5%. Among the biggest price moves was Myseum, which surged by around 129% after repositioning itself under the name Myseum.AI. The rally followed an even more spectacular gain on Wednesday in shares of sneaker maker Allbirds, after the company announced a strategic shift toward artificial intelligence. Voyager Technologies shares climbed 8.8% after NASA awarded the company a contract to carry out the seventh private astronaut mission to the International Space Station—marking the first time the firm has been selected for such a mission.

Oil prices rose on Thursday as market uncertainty increased over whether peace talks between the United States and Iran would be able, in the short term, to resolve the energy supply disruptions in the Middle East caused by their ongoing war. Brent crude futures climbed 4.7%, while WTI rose 3.7%.

There was minimal movement in the international bond market; however, the domestic 10-year yield fell to close to 6%, a level not seen since before the outbreak of the Iran war

Yesterday, despite a renewed rise in energy prices, bond markets remained relatively calm, and neither the slightly higher-than-preliminary final March euro area inflation data nor the weak U.S. industrial production figures led to any significant market moves. The 10-year U.S. Treasury yield stayed around 4.3%, while the German 10-year yield remained slightly above 3%. The dollar strengthened somewhat, with EUR/USD correcting from its previous peak of 1.18 to around 1.178.

There was also only limited movement in regional currency markets. The Czech koruna strengthened marginally, while the zloty weakened by 0.1% and the forint by 0.4%, with EUR/HUF correcting to 365. At yesterday’s three-, five- and ten-year bond auctions held by the Government Debt Management Agency (ÁKK), demand was extremely strong, with bids exceeding HUF 400 billion across the three bonds. ÁKK took advantage of the strong interest and sold more than HUF 200 billion in nominal value of bonds at an average auction yield of around 6%. Benchmark yields declined further by 6–10 basis points, with the 10-year yield only slightly above 6%.

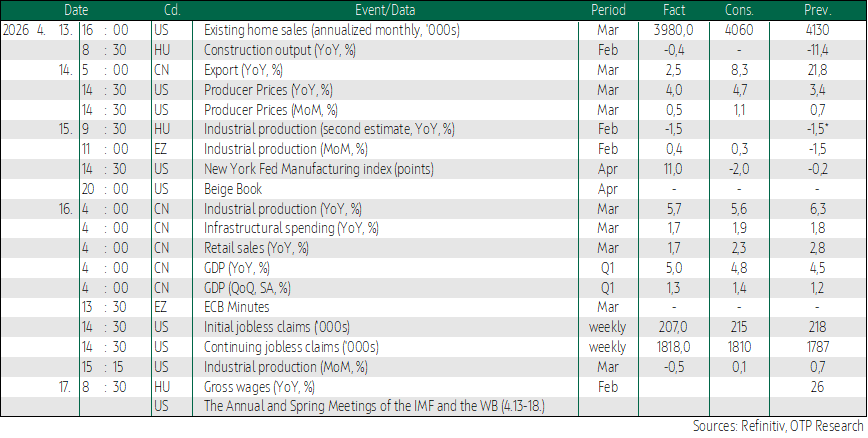

Today's highlights

Although Japan’s Nikkei rebounded by 1% from its record high yesterday, it is still on track to finish the week with a sizable gain of over 4%. China’s SSEC is down 0.3%, but its weekly performance could still come in at around a 1.5% increase. Investors are waiting on the sidelines ahead of potential U.S.–Iran talks over the weekend. European futures are slightly lower, while their U.S. counterparts are hovering near flat. WTI crude is down 1.3%.

Today, domestically the February wage data will be the key focus, while on the international front it will be important to closely monitor news related to Iran.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more