OTP Morning Brief: Stock market sentiment was mixed ahead of the expected resumption of USA-Iran peace talks

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

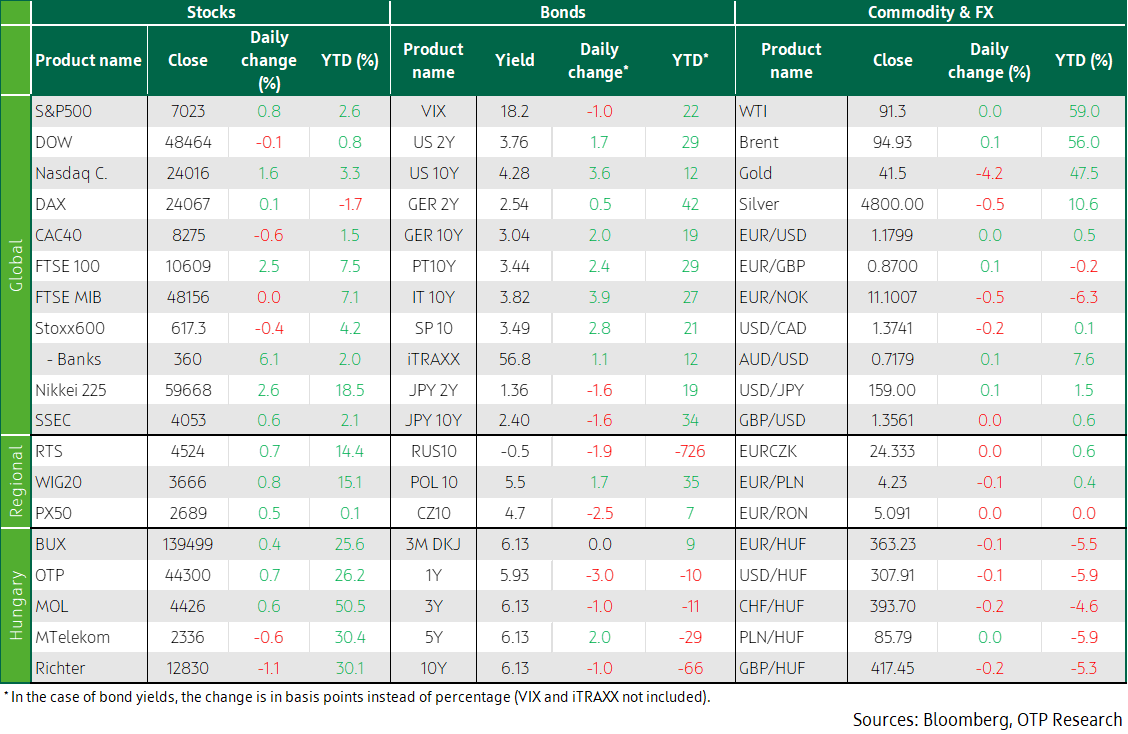

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Developed equity market had a mixed performance on Wednesday amid expectations that the USA and Iran resume negotiations soon. In Western Europe, most of the stock indices declined, as a sharp fall in luxury goods manufacturers weighed down sentiment after Hermés and Kering reported the negative impact of Middle Eastern tensions on sales. Main indices in CEE strengthened, with the BUX closing at a new all-time high on Wednesday. In the US, major indices rose further, with the S&P500 and the Nasdaq Composite closing at fresh record highs. By contrast, bond markets saw little movement yesterday, while the EUR/USD pair closed around 1.18. The EUR/HUF exchange rate also barely moved, remaining near the 363 level. Asian stock markets were in the green this morning, China released mixed macroeconomic data. Today, the final March eurozone CPI will be released, along with the minutes of the ECB’s latest monetary policy meeting.

Most European stock markets weakened following a downturn in the luxury sector

Sentiment on European stock markets turned negative, as investors primarily focused on developments in Middle Eastern geopolitical tensions, in particular pricing in the risk of an escalation of the US–Iran conflict as well as the chances of a potential diplomatic de-escalation. The STOXX 600 index fell by 0.4%, mainly driven by weakness in the luxury sector. Within the sector, Hermés plunged 8% after Middle East tensions significantly curbed sales growth, while Kering dropped 9% after the company reported weaker-than-expected performance due to Gucci's slowing demand linked to the conflict.

The performance of the major European stock indices was mixed but overall weak. France’s CAC40 and the UK’s FTSE 100 reacted sensitively to negative sector-specific news, with the former closing down 0.6% and the latter falling 0.5%. By contrast, Germany’s DAX posted a slight 0.1% gain, reflecting technical stability rather than any meaningful fundamental support.

The three main stock indices in the CEE-region showed overall improvement compared to the previous trading session: while markets had been characterized by more moderate, mixed movements a day earlier, all three indices managed to post gains today. The WIG20 performed the strongest, rising by 0.8%, followed by the PX, which gained 0.5%, while the BUX advanced 0.4%, indicating a slightly improving regional risk sentiment compared with yesterday’s levels.

Hungarian blue chips were a mixed bag amid subdued market sentiment. OTP shares rose by 0.7%, showing a moderate correction after the previous day’s decline, while Mol gained 0.6%, reflecting stabilization in the energy sector. By contrast, Richter’s share price fell by 1.1%, continuing the downward trend seen in recent days, while Magyar Telekom weakened further.

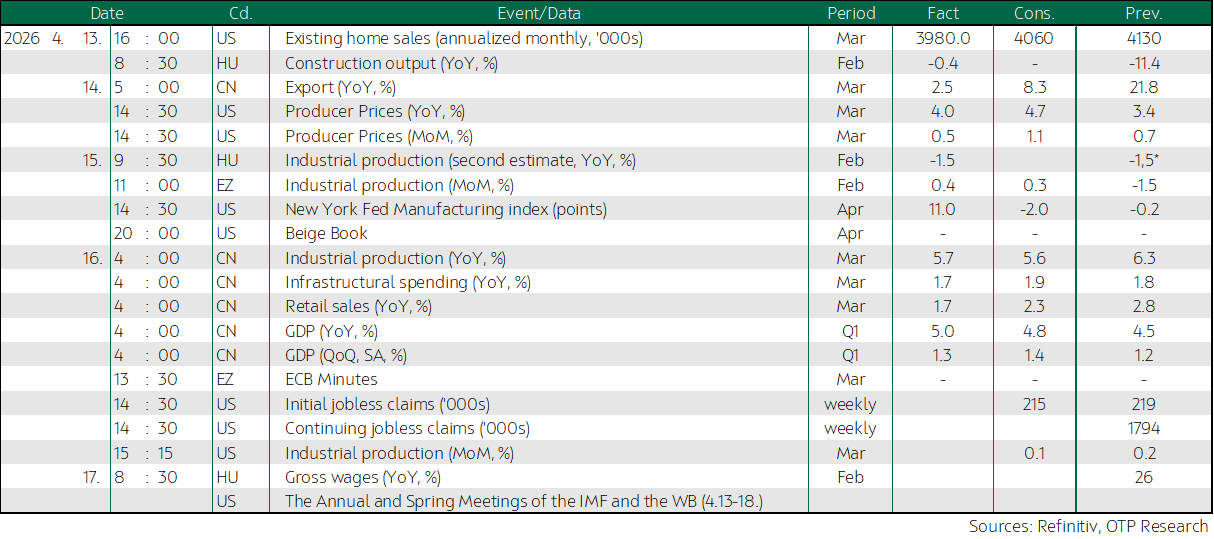

In Hungary, industrial production declined by 1.5% yoy in February following the contraction seen in January, while a significant decrease was also observed on a month-on-month basis. Within manufacturing, coke production and petroleum refining continued to represent the main downside risk, while the performance of the energy sector also deteriorated sharply, by around 11%. Based on data for the first two months of the year, overall industrial output remains below the level of the same period last year, continuing to point to a weak cyclical picture for the industrial sector.

The S&P500 and the Nasdaq Composite closed at new record highs, as investors welcomed bank earnings reports and the extension of the Broadcom–Meta partnership

US stock indices rose on Wednesday, as investors welcomed corporate earnings reports alongside optimistic expectations regarding the end of the war with Iran. While the Dow edged slightly lower, the Nasdaq Composite and the S&P500 both closed at new all-time highs. The former has now advanced for 11 consecutive days, while the latter has finished in positive territory in ten of the past eleven trading sessions. Equity markets have been climbing this week amid hopes of a peace agreement between the United States and Iran. US President Donald Trump said on Fox Business’s Wednesday program that the war against Iran would come to an end very soon. Of the S&P 500’s 11 major industry sectors, the majority closed lower, with materials (-1.2%) and industrials leading the declines, while technology and consumer discretionary stocks provided upward momentum for the index. Broadcom was among the biggest winners of the session, gaining 4% after Meta Platforms extended its partnership with the company, under which custom chips are developed using Broadcom’s technology. Other notable gains among chipmakers included Nvidia (+1.2%), AMD (+1.2%) and Intel (+1.8%), while software companies such as Microsoft, Oracle, Palantir and Synopsys recorded rallies of 4–5%. Among megacap stocks, Apple jumped 3% and Tesla surged 7.6% amid the broadly positive sentiment, while Alphabet and Meta closed the session with gains of more than 1%.

Key corporate earnings were also released on Wednesday: Bank of America and Morgan Stanley reported revenue and profit figures that exceeded analysts’ expectations. Bank of America shares rose by nearly 2% yesterday, while Morgan Stanley jumped 4.5%.

Amid cautious expectations of a near-term resumption of ceasefire talks, crude oil futures were essentially flat on Wednesday. Brent crude remained below 95 USD/bbl, while WTI fluctuated around 91 USD/bbl. While President Trump said the war with Iran would soon be over, press reports suggested that the United States and Iran are working, among other issues, on extending the ceasefire following the imminent restart of negotiations. Meanwhile, European natural gas futures fell to around EUR 41/MWh, the lowest level since the attack against Iran.

Long yields slightly corrected on Wednesday, the EUR/USD remained near 1.18, while only minimal movement was observed in the domestic market

Although data released yesterday showed that euro area industry expanded faster than expected in February, this did not affect market expectations. Following the large swings seen recently, trading in developed economies’ bond and currency markets was surprisingly calm yesterday. Bond yields generally rose by 2–3 basis points both in the United States and in major euro area countries, with the 10-year US Treasury yield approaching 4.3%, while the German 10-year yield stood at 3.03%.

The EUR/USD pair had already approached the 1.18 level on Tuesday, and the exchange rate did not change materially yesterday.

There was no significant movement in the regional FX market either, with the forint’s exchange rate against the euro stagnating below the four-year high around 364. Only minimal movements were also seen in the bond market, with the longer end of the domestic yield curve remaining around 6.15%.

Today's highlights

Market sentiment was also positive in Asian stock markets today. The Nikkei and the Hang Seng gained 2%, the Shanghai Composite edged by 0.5% ahead of the morning close, while South Korean benchmarks are posting gains of 1–2%. In China, stronger-than-expected Q1 GDP and industrial production data were released today, while March retail sales and investment figures came in below preliminary expectations. The unemployment rate rose to 5.4% last month.

Today, attention may be focused on the final March inflation data for the euro area, as well as the minutes of the ECB’s most recent monetary policy meeting. In the UK, February industrial production, manufacturing output and construction data could also be of interest.

In the US, regional Fed banks will publish their business activity indices, while March industrial production and manufacturing data will also be released. Developments in the weekly jobless claims figures may also be today's highlights.

In Europe, earnings reports from Tesco Plc, Lonza and Pernod Ricard are due today, while in the US, the earnings reports of Netflix, PepsiCo and Charles Schwab will be in the focus.

Today, the Government Debt Management Agency (ÁKK) will offer 3-, 5- and 10-year government bonds in amounts of HUF 15, 20 and 25 bn, respectively.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more