OTP Morning Brief: The BUX outperformed, the forint strengthened sharply, and domestic bond yields fell

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

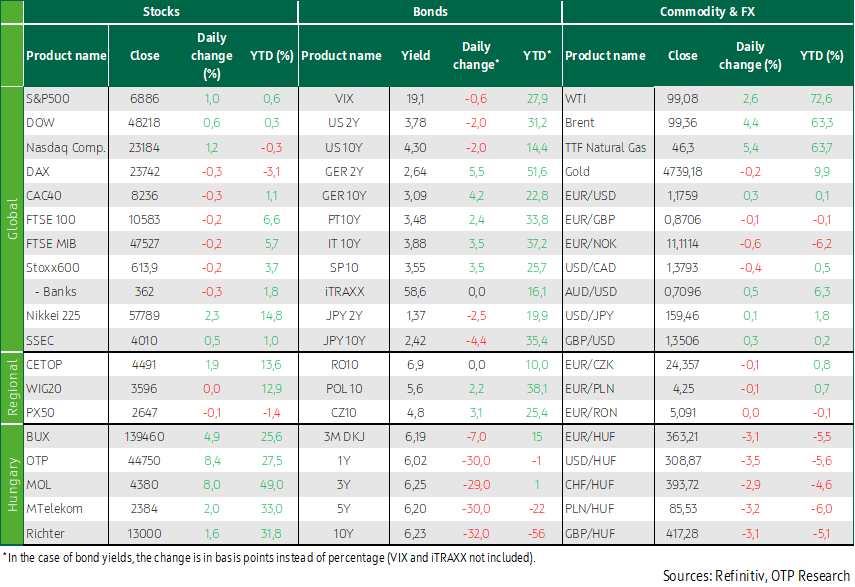

The weekend US–Iran talks failed to produce results, and on Monday the United States began a naval blockade of Iranian ports. Energy prices rose again on Monday, while Western European equity markets started the week with moderate declines. The BUX was an outperformer, rising by nearly 5%, with gains led by OTP (+8.4%) and Mol (+8%). Wall Street indices also started the week with strong gains. The forint strengthened by 3%, and domestic bond yields fell by 30–40 basis points. Earnings reports are due today from, among others, JPMorgan, Citigroup, Wells Fargo, and BlackRock. In the morning hours, strong gains are being seen in Asia, while oil prices are declining.

The United States has begun a naval blockade of Iranian ports

The two-week ceasefire that came into effect last Tuesday is being put at risk by the failure of the weekend US–Iran talks. Iran rejected demands to shut down its nuclear program, fully reopen the Strait of Hormuz, and cease support for armed groups allied with Iran. In response, President Donald Trump said on Sunday that any vessels on international waters that have paid transit fees to Iran would be intercepted. In addition, the US military announced that it would begin a full naval blockade of Iranian ports. According to the announcement, US forces will not obstruct ships transiting the Strait of Hormuz that are heading to or coming from non-Iranian ports. Even so, the measure could reduce global oil supply by nearly two million barrels per day. Iran’s Islamic Revolutionary Guard Corps warned that military vessels approaching the strait would be considered a violation of the ceasefire. NATO allies said on Monday that they do not intend to participate in the blockade of the strait. Energy prices rose again on Monday, with Brent crude increasing by around 4%.

Western European equity markets declined moderately

Against the backdrop of news from the Middle East, Western European equity markets started the week with moderate declines. The STOXX 600 fell by 0.2%, the DAX and the CAC 40 each dropped by 0.3%, while the FTSE 100 slipped by 0.2%. Travel and leisure stocks were among the biggest losers, with the sector down 1%; among airlines, Wizz Air fell by 5.4%, EasyJet by 2.6%, and Lufthansa by 2.3%. Luxury goods company LVMH reported quarterly revenue on Monday that fell short of expectations, with the war in the Middle East already having an impact. The French company’s US-listed shares dropped by more than 3% on Monday. The Volkswagen Group reported a 4% year-on-year decline in global deliveries in the first quarter of 2026, as weak demand in China and the United States put noticeable pressure on the German automaker. In China, extremely intense price competition with domestic brands is severely squeezing margins, while in the US demand is being held back not only by tariffs but also by the phasing-out of electric-vehicle subsidies. The automaker’s share price fell by 1.4% on Monday.

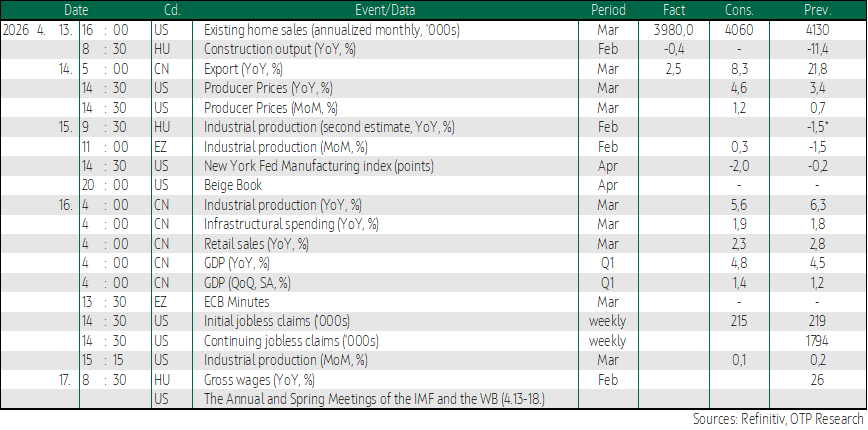

Looking at domestic macroeconomic data, construction output in February was 0.4% lower than in the same period a year earlier. On a month-on-month basis, output increased by 4.9%, which represents only a partial correction following the nearly 9% decline recorded in January.

Following last week’s gain of more than 7% and Sunday’s parliamentary elections, the Hungarian stock market remained an outperformer in the region on Monday amid exceptionally high trading volumes. While Poland’s WIG20 was close to flat and the Czech PX50 slipped by 0.1%, the BUX index surged by nearly 5%. Among blue chips, gains were led by OTP, which jumped 8.4%. Mol rose by 8%, Magyar Telekom by 2%, and Richter closed 1.6% higher. The biggest losers included Opus (-30.2%) and 4iG (-17.4%). Markets reacted positively to comments by Péter Magyar, leader of the election-winning Tisza party, who confirmed his intention to cooperate with the central bank’s leadership.

Wall Street indices started the week with strong gains

Wall Street indices started the week with strong gains. The S&P 500 rose by 1%, the Dow Jones increased by 0.6%, and the Nasdaq Composite advanced by 1.2%. As a result, the S&P 500 has fully recovered all the losses it had suffered since the outbreak of the war. For the time being, investors looked past the lack of progress in the weekend US–Iran talks.

The rally was driven primarily by the technology and financial sectors: Oracle’s share price jumped by nearly 13%, while Microsoft gained 3.6%. Intel shares closed higher for the ninth consecutive day on Monday, with the entire rally delivering almost a 58% gain in the stock price. The surge was fueled by several strategic announcements, including agreements with Google and Elon Musk. Demand for Intel-manufactured CPUs is being supported by the fact that, following the training phase of the AI revolution, increasing emphasis is being placed on generating responses to user queries. The financial sector rose by 1.7%. However, Goldman Sachs’ earnings report disappointed the market due to weakness in its fixed income, currency, and commodities division, despite profits exceeding expectations. Defensive sectors (utilities and consumer staples) underperformed on Monday.

Another excellent day for the domestic bond and foreign exchange markets

After Middle East peace talks collapsed over the weekend and oil prices surged by nearly 10%, trading on developed bond markets opened with significant selling pressure. Later, however, news about a possible resumption of negotiations brought some calm. Ultimately, oil prices closed up by only 2–3%, allowing US Treasury yields to edge lower, with the 10-year yield falling by 5 basis points to below 4.3%. Euro area bond yields rose slightly, pushing the German 10-year yield above 3.05%. The dollar continued to weaken, with EUR/USD trading around 1.175.

Another excellent day for the domestic bond and foreign exchange markets followed the parliamentary election, which was won by the Tisza party – campaigning on a pro-Western foreign policy, the securing of EU funds, and the introduction of the euro – with a two-thirds majority. The forint continued to strengthen, appreciating by another three (!!!) percent yesterday from the 375 level to around 363, a level not seen since the launch of the invasion of Ukraine. Meanwhile, bond yields fell by 30–40 basis points, with long-term yields dropping to around 6.2%. There were no significant moves in other regional currency markets: both the Czech koruna and the Polish zloty were broadly unchanged, while bond yields rose in both the Polish and Czech markets. Today, the Government Debt Management Agency (ÁKK) will hold a three-month T-bill auction, with an announced amount of HUF 20 billion.

Today's highlights

Sentiment is also positive across Asian markets as trading approaches the close. The Nikkei is up 2.3%, the KOSPI 3.7%, the SSEC 0.5%, and the Hang Seng 0.4%. However, China’s year-on-year export growth of 2.5% in March fell well short of expectations. Oil prices moved lower in the morning hours, driven by expectations related to a resolution of the Iranian conflict.

Domestically, Duna House will publish its first-quarter housing market price index today, along with data on housing market transactions in March. From the United States, the March producer price index is due. Earnings reports are also scheduled today from, among others, JPMorgan, Citigroup, Wells Fargo, and BlackRock.

The IMF will publish its updated macroeconomic forecasts today as part of the April World Economic Outlook (WEO).

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more