OTP Morning Brief: Winds blowing from the Strait of Hormuz are driving the markets

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

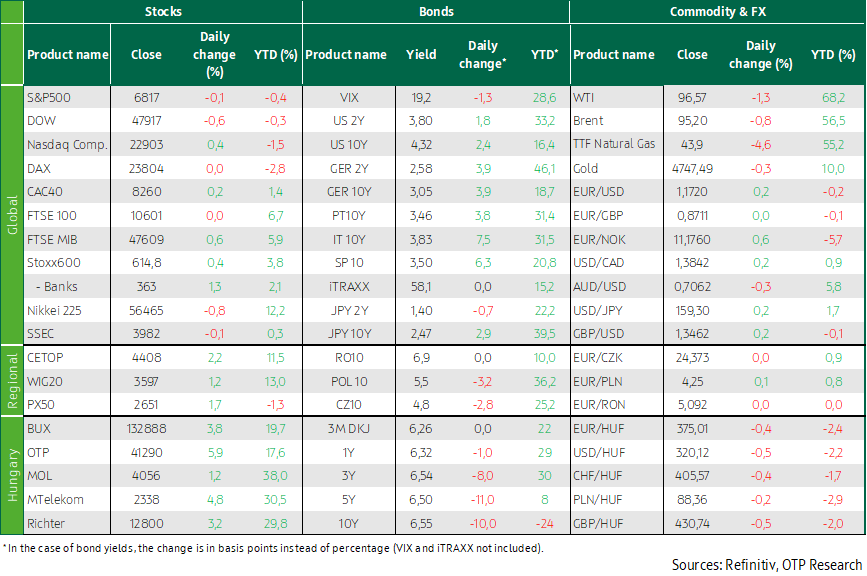

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Optimism fueled by the ceasefire agreement faded steadily over the past week as the conflict appears to be escalating again. On Friday, the world’s leading stock exchanges delivered mixed performances, but managed to rise on a weekly basis. Stock markets in the CEE region closed in positive territory on Friday and also posted gains for the week as a whole. Due mainly to rising fuel prices, inflation in the United States accelerated in March, in line with expectations. The Middle Eastern ceasefire helped push crude oil prices lower last week, but prices rebounded following news of developments over the weekend. Eurozone yields remained stuck near previous highs, while long-term U.S. yields declined. The euro strengthened against the dollar. Domestic long-term yields fell, and the forint performed well on the foreign exchange market. In Sunday’s parliamentary election, with more than 98% of votes counted, the Tisza Party secured a two-thirds majority in the Hungarian Parliament. This week will bring several domestic, European, and U.S. business cycle indicators, and the earnings season is set to begin.

Optimism fueled by the ceasefire agreement gradually faded over the course of last week

Last week, global attention remained focused on the Middle Eastern conflict and the Strait of Hormuz. In the first half of the week, news about the start of negotiations significantly eased fears related to oil supply, inflation, and interest rate hikes. Risk appetite strengthened, while energy prices, the dollar, and bond yields declined. In the second half of the week, however, a correction began, and over the weekend peace talks collapsed, to which markets will only be able to react today. On Sunday, Donald Trump announced that the U.S. Navy will impose a blockade on the Strait of Hormuz today, and he also threatened China with a 50% tariff should if it sends arms to Iran. As a result, oil prices are rising again.

On Friday, optimism in European markets was still fueled by confidence in the success of the weekend peace talks

Cautious optimism characterized trading on Friday across the leading Western European stock exchanges, with only Germany’s DAX and the UK’s FTSE 100 slipping into slight negative territory. At the sector level, media, basic materials, financials, and technology performed best, while aerospace and defense stocks declined on news of a possible Russian–Ukrainian agreement. Germany’s Rheinmetall and Hensoldt, as well as Italy’s Leonardo, fell by more than 5%, while CSG dropped by 8%. Shares of Sodexo plunged more than 10% to a six-year low after the French company significantly revised down its full-year revenue and profitability targets. Repsol’s share price declined by 5.8% after the Spanish energy company reported weaker-than-expected first-quarter results.

Looking at the week as a whole, all major European stock markets managed to move higher—for the third consecutive week—as investors awaited the next round of U.S.–Iran peace talks over the weekend with optimism, that we now know did not succeed. The pan-European Stoxx 600 rose by 0.4% on Friday, bringing its weekly gain to 3%.

Stock markets in the CEE region also moved higher on Friday, with the BUX clearly delivering the strongest performance, rising by nearly 4%. All domestic blue-chip stocks closed in positive territory, with OTP—up more than 5%—emerging as the day’s winner on the final trading day of the week. Looking at the week as a whole, the BUX also outperformed the region, posting gains of over 7%.

With more than 98% of votes counted in Sunday’s parliamentary election, the Tisza Party secured a two-thirds majority in the Hungarian Parliament. The result was received positively by the market, with the forint strengthening against the euro, falling below the 370 level.

Most major U.S. indices declined on Friday, but posted gains for the week as a whole

Leading Wall Street indices slipped slightly on Friday, with the exception of the NASDAQ, which was able to benefit from the strong performance of the technology sector, as investors remained cautious ahead of the weekend peace talks. Among the S&P sector indices, consumer staples led the declines, while technology stocks topped the gainers. Chipmakers recorded strong gains, with Broadcom and Nvidia rising by 4.7% and 2.6%, respectively. The financial sector underperformed on Friday, as markets prepared for the release of earnings reports from major U.S. banks due later this week. On a weekly basis, all three major Wall Street indices posted solid gains.

The March inflation data published on Friday showed an acceleration in line with expectations. The 0.9% month-on-month increase was driven three-quarters by rising fuel prices, while the increase in housing costs—long a persistent concern—also accelerated compared with February. Core inflation rose by 0.2% month-on-month, as in February, below than expected (+0.3%).

Following Thursday’s rebound after the sharp sell-off on Wednesday, Brent and WTI prices edged slightly lower again on Friday. Prices are hovering around USD 95 per barrel. However, worries began to mount again on unfavorable news related to the peace talks.

Eurozone yields remained stuck around previous highs; long-term U.S. yields declined; the euro strengthened against the dollar; domestic long-term yields fell; and the forint performed well on the foreign exchange market

Although markets are currently paying less attention to macroeconomic data, incoming U.S. and European activity indicators—largely still referring to the period before the outbreak of the war—pointed to a slowdown in growth, while U.S. core inflation for March also came in lower than expected. Markets continue to expect the Federal Reserve to keep its policy rate unchanged at the current 3.5–3.75% level through year-end, though the implied probability of rate cuts increased last week. Long-term bond yields fell by around 10 basis points from recent local peaks by mid-week, but only about half of this move remained after the subsequent correction, leaving the 10-year yield above 4.3%, in the lower third of the post-COVID trading range. The number of 25-basis-point rate hikes expected from the ECB declined from three to four to two to three, while eurozone government bond yields, despite significant volatility, ultimately hovered around previous highs. The 10-year German Bund yield returned above the important 3% level, the upper bound of the post-pandemic trading range. The euro continued to strengthen against the dollar on Friday as well for the whole week—rising by 0.2% on the final trading day and by 2% over the week as a whole—pushing the EUR/USD exchange rate above 1.17.

In Hungary, February’s industrial production and retail sales data show no sign of a meaningful acceleration in growth in the first quarter, although the March inflation figure came in more favorably than expected. This likely contributed to the very positive sentiment on the domestic FX and bond markets in the week leading up to the parliamentary elections. The forint strengthened by 0.5% against the euro on Friday and by 2% over the week as a whole, pushing the EUR/HUF exchange rate below 375—a two-and-a-half-year high for the forint. This represented a significant outperformance compared with the zloty and the koruna, which appreciated by less than 1% over the week. Expectations for rate hikes also declined: instead of the 125 basis points priced in two weeks ago and the 75 basis points expected a week ago, the yield curve now implies a single 25-basis-point rate increase. As a result, government bond yields fell sharply, with maturities beyond one year declining by 10 basis points on Friday and by 30–50 basis points over the week as a whole. The 10-year yield now stands only slightly above 6.5%.

Today's highlights

News over the weekend related to the Middle Eastern conflict was received negatively by the major Asia-Pacific stock markets this morning. The failure of the peace talks and the potential U.S. blockade of the Strait of Hormuz have renewed concerns about a prolonged conflict and pushed oil prices higher. As a result, Brent crude, which was trading around USD 95 per barrel on Friday, climbed back above USD 100 per barrel this morning. Equity index futures point to a lower open in both Europe and the United States.

Today it will be important to monitor how markets react to the domestic election results.

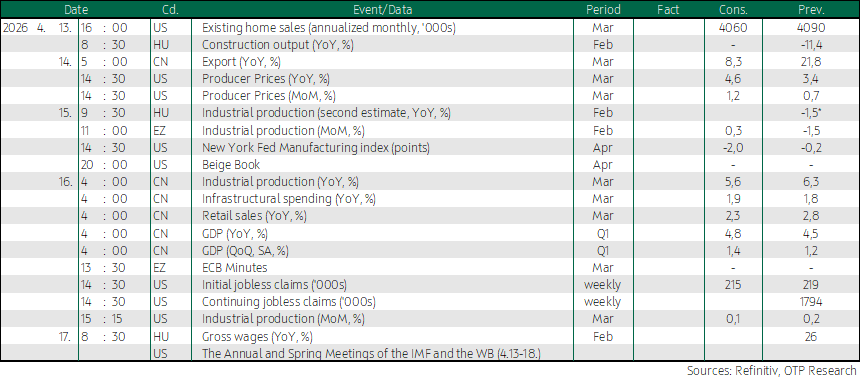

From a data perspective, we are heading into a busy week both domestically and internationally. Hungary’s Central Statistical Office (KSH) will publish February business confidence indicators. Industrial production data will be released from the euro area and the United States, while first-quarter GDP figures will be in focus in China.

News related to the Middle Eastern conflict is unlikely to fade into the background, and markets are currently awaiting reactions to the unfavorable developments over the weekend.

In addition, the earnings season kicks off this week, with major names such as Goldman Sachs, JPMorgan, Citigroup, BlackRock, Bank of America, Morgan Stanley, and Netflix among those set to report.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more