OTP Morning Brief: Investors were closely monitoring the extremely fragile ceasefire

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

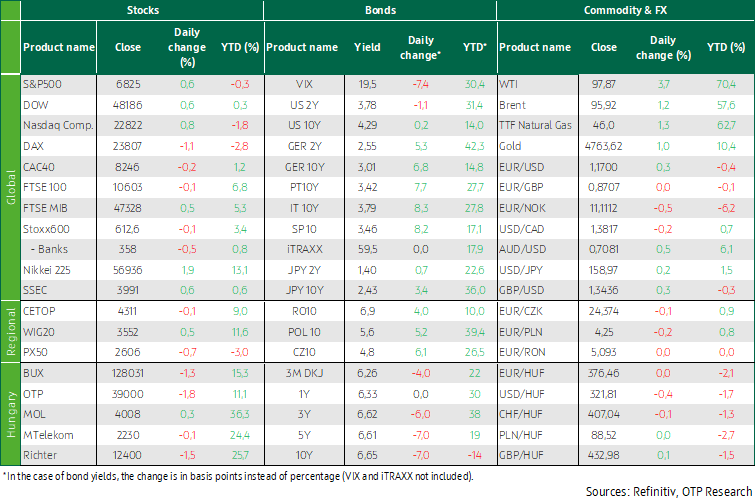

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

European markets declined under the pressure of the ceasefire. German industrial production fell more than expected ahead of the war, while export performance came as a positive surprise. The Polish central bank left its policy rate unchanged. Markets rose later in the evening on signs of de-escalation. Core PCE came in in line with expectations. Oil futures rose again. U.S. yields declined, and a weakening dollar supported gains in regional currencies. Asian stock markets advanced. Today, attention will be on U.S. inflation data.

Investors were watching the extremely fragile ceasefire; European markets declined, and industrial production in Germany came in lower than expected

Investors worldwide were monitoring developments surrounding the shaky U.S.–Iran ceasefire, which came under threat within a day after Israel stated that the agreement did not extend to Lebanon and carried out the most intense airstrike of the war on Beirut, resulting in more than three hundred fatalities, just days ahead of the planned talks in Pakistan. In response, Iran’s Supreme Leader vowed retaliation for the attacks and signaled a move into a “new phase” of control over the Strait of Hormuz, which effectively remained closed despite Wednesday’s agreement, with not even 10% of normal shipping traffic able to pass through. Accordingly, both the Iranian and U.S. sides accused each other of violating the ceasefire. However, by the end of yesterday’s session, Israeli Prime Minister Benjamin Netanyahu stated that he intended to pursue direct talks with Beirut.

Volatile news dampened investors’ risk appetite, and following the strong gains seen on Wednesday, European stock markets turned lower again. The DAX recorded the largest decline, falling 1.1%, while the CAC 40 slipped more modestly by 0.2% and the UK’s FTSE 100 edged down 0.1%, leaving the Stoxx 600 to close just 0.1% lower overall. The industrial sector weighed most heavily on the market, declining 0.5%, with Germany’s Siemens falling 2.1% and Airbus dropping 2.5%. Travel, banking, and technology stocks also traded in negative territory following the previous day’s rally, while the energy sector rose 1.9% amid renewed gains in oil prices. The sector was supported by a 3.1% rise in BP shares, which also provided support to the UK market.

Germany’s weaker market performance was partly driven by a contraction in industrial production, which fell by 0.3% month on month in February, compared with expectations for a 0.7% increase, although the January figure was revised upward. The outlook for the industrial sector is being weighed down by energy prices that remain significantly above pre-Iran conflict levels. That said, analysts argue that the risk of a downturn comparable to the 2022 energy crisis is lower, as the rise in energy prices has been more moderate, interest rates are unlikely to increase further, portion of the energy-intensive production capacity has been already underperforming, and the manufacturing PMI showed a slight improvement in March. The weaker-than-expected data point was partly offset by a strong export performance, as German exports rose by 3.6% month on month in February 2026, reaching a three-year high of EUR 135.2 billion, following a downward-revised 1.5% decline in January and exceeding the market’s expectation of a 1% increase.

Sentiment across Central and Eastern Europe was also mostly negative, with the BUX falling 1.7% and the PX50 down 0.7%, while the WIG20 posted a gain of around 0.5%. The latter may have been supported by the Polish central bank’s decision at its April meeting to keep the policy rate unchanged at 3.75%, in line with market expectations. Optimism expressed at the previous meeting regarding the Middle East conflict has since faded, with inflation forecasts now surrounded by heightened uncertainty. Within the BUX index, losses were led mainly by OTP, which fell 1.8%, and Richter, down 1.5%.

U.S. markets moved higher on positive news, with core PCE meeting expectations

The deterioration in morning sentiment had partly eased by the time of the U.S. market open, and following conciliatory remarks from Israeli officials, U.S. equities moved higher: the S&P 500 and the Dow Jones ended the session up 0.6%, while the Nasdaq gained 0.8%. The consumer discretionary sector strengthened after Amazon CEO Andy Jassy said that annualized revenue from AI-based services within the company’s cloud division has exceeded USD 15 billion so Amazon shares closed sharply higher, up 5.8%. CoreWeave shares rose 3.4% after the cloud infrastructure company announced an expansion of its USD 21 billion cloud agreement with Meta Platforms, although gains were limited by the announcement of a USD 3 billion convertible bond issuance.

PCE inflation rose by 0.4% month on month in February, while the year-on-year rate remained at 2.8%, indicating price pressures similar to those seen in the previous month. At the same time, core inflation—excluding volatile food and energy prices—also increased by 0.4% on a monthly basis, while easing to 3.0% year on year from 3.1% in January. Consumption expanded by 0.5% in February, suggesting that elevated price levels continue to provide meaningful support to the growth of nominal spending. Inflation had already been running above the 0.2% monthly pace consistent with the Fed’s 2% target even prior to the war, a trend that was further reinforced by Trump’s import tariffs. According to weekly labor market data, initial jobless claims rose by 16,000 to 219,000 in the week ending April 4 compared with the previous week, exceeding the market expectation of 212,000 and reaching the highest level in roughly one month.

Brent crude oil futures rose again on Thursday, gaining 1.7% to above USD 96 per barrel, partially correcting the nearly 13% plunge seen in the previous trading session, as investors grew increasingly concerned about the fragility of the ceasefire. Meanwhile, WTI surged by 3.7%, approaching USD 98 per barrel.

U.S. Treasury yields declined, while a weakening dollar supported gains in regional currencies

Optimism about a swift end to the conflict with Iran proved short-lived, as the parties failed to adhere to the ceasefire. As a result, the sharp sell-off seen in energy prices on Wednesday was followed by a correction yesterday. Meanwhile, the U.S. 10-year Treasury yield edged slightly lower, briefly dipping below the 4.3% level, after February PCE inflation rose in line with expectations, while fourth-quarter GDP growth was revised down to an annualized 0.5%. Weaker data have also been emerging for the first quarter, and initial jobless claims increased as well. In contrast, European bond yields corrected higher after Wednesday’s drop, with the 10-year German yield rising by nearly 5 basis points to around 3.0%. On the back of weak U.S. data, the euro strengthened further, with EUR/USD reaching the 1.17 level.

Regional currencies were supported by a weakening dollar, with the Czech koruna appreciating by 0.1%, the Hungarian forint by 0.2%, and the Polish zloty by 0.3% against the euro. The domestic currency strengthened back to the 376 level per euro. The Government Debt Management Agency’s (ÁKK) early-afternoon published government bond reference yields showed declines of 5–6 basis points at maturities beyond one year; however, this largely reflected the drop following Wednesday’s fixing, as there was no material movement during yesterday’s trading session, with the 10-year yield closing below 6.7%. Demand was weak at auctions, however: the announced HUF 20 billion of one-year Treasury bills was only just sold, at an average yield of 6.35%. Sales of the 15-year bond amounted to HUF 26 billion at an average yield of 6.71%, while only around HUF 7 billion of the 20-year green bond was sold, at an average yield of 6.73%.

Today's highlights

Most Asian stock markets advanced on Friday amid cautious optimism ahead of ceasefire talks between Iran and the United States. South Korea’s KOSPI was the best-performing index, rising 1.9% as demand for local technology stocks strengthened. Markets showed little reaction to the Bank of Korea’s decision to leave its policy rate unchanged at 2.50%. Japan’s Nikkei also gained 1.9%, while China’s Shanghai Composite (SSEC) was up 0.6%.

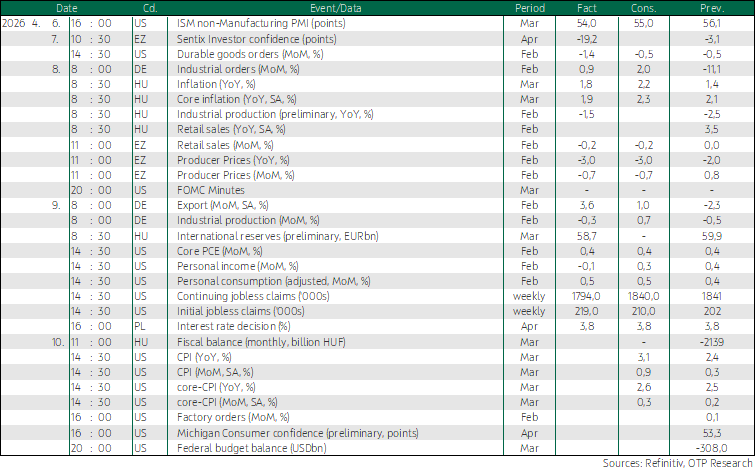

Today, investors’ attention will primarily be focused on U.S. inflation data, although figures on factory orders, a confidence index, and the federal budget balance are also due. Before these releases, however, Hungary’s March budget balance will be published.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more