OTP Morning Brief: Netflix walked away from WBD deal

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

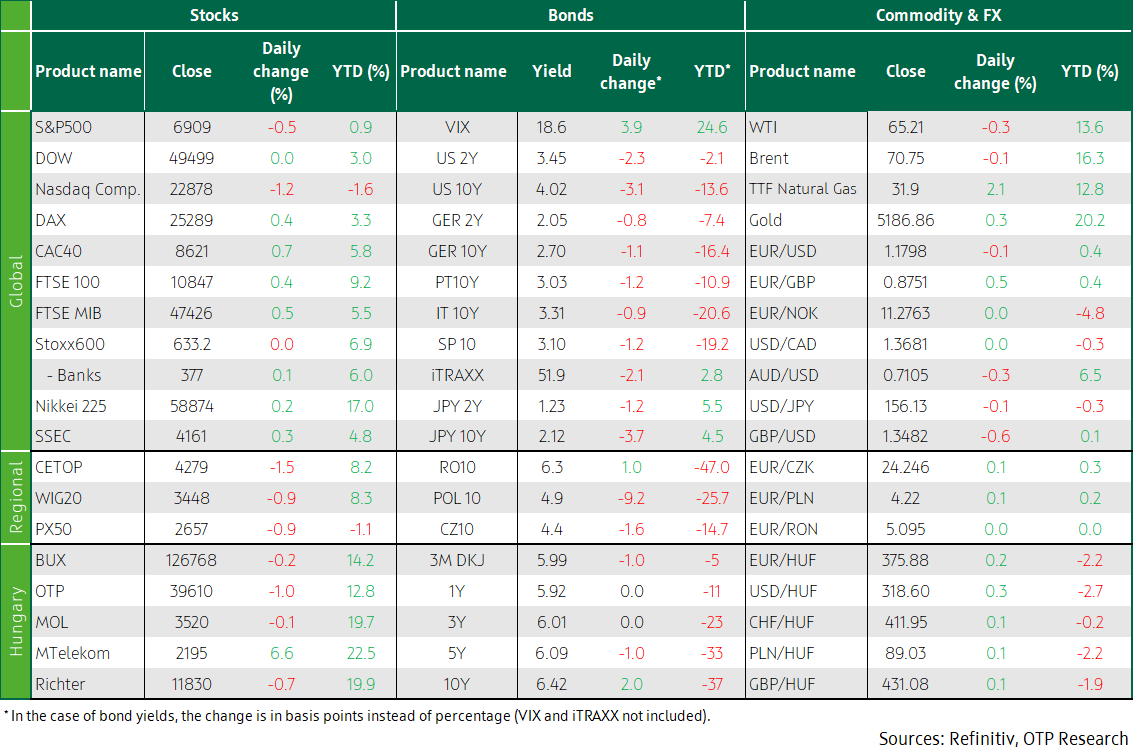

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Corporate earnings reports moved markets in Europe. Nvidia's strong earnings failed to alleviate investors’ concerns; the world's largest company by market cap slumped 5.5% yesterday. In Europe, ASML, ASM International, and BE Semiconductor fell more than 4%. The European Commission's Economic Sentiment Index (ESI) disappointed. US indices declined yesterday. The unsupportive sentiment on global stock market made investors seek bonds. In the bidding war for Warner Bros between Netflix and Paramount, Netflix walked away in the end. The third round of US-Iran talks was held in Geneva on Thursday. France, Spain, and Germany publish February inflation data today. Hungary releases January industrial producer prices and unemployment rate today.

Corporate earnings reports moved markets in Europe

Following an across-the-board rise on Wednesday, the STOXX 600 closed almost flat on Thursday as investors digested corporate reports. Germany’s DAX (+0.45%), France’s CAC40 (+0.7%), and the UK’s FTSE100 (+0.4%) all advanced. A 1% decline in the healthcare sector weighed on the Stoxx Europe index. The technology sector slid 0.5%, as ASML, ASM International, and BE Semiconductor slumped more than 4%, as Nvidia's particularly impressive report proved fell on deaf ears on stock markets.

In the corporate world, Rolls-Royce revved up more than 5% as it suggested further dynamic growth after 40% jump in profit in 2025. Schneider Electric, a maker of artificial intelligence hardware, published stronger-than-expected earnings, driven by robust demand for data centres; its shares soared 3%. Belgian chemicals company Syensqo, whose fourth-quarter earnings missed expectations, nose-dived 30.6%, therefore its trading was suspended at one point on Thursday. Spain’s defence industry company Indra was among top performers, skyrocketing more than 21%, on the back of better-than-expected 2025 results. On Thursday, Stellantis reported a net loss of EUR 20.1 billion for the second half of 2025; earlier this month, it said it would book EUR 22.2 billion one-off charges in that period, owing to a scale-back in its electric vehicle strategy. Its stock price grew by 4.2%. The huge loss highlights the difficulties carmakers are facing around the world, as the transition from internal combustion engines to electric vehicles is slower and more complex than had been hoped, while the United States and Europe ease their EV targets. Separately, Erste Group posted a record profit of EUR 3.5 billion in 2025, supported by balanced loan and deposit growth and strong performance in Austria and the Czech Republic. The group’s capital position continued to strengthen, but this year the dividend payment will be reduced to EUR 0.75, owing to the cash-financed acquisition in Poland. German sportswear maker Puma said on Thursday it was like to be in the red this year, but its 2025 loss was smaller than feared. Under new CEO Arthur Hoeld, Puma is undergoing a transformation process, owing to subdued demand for sportswear, and as US import tariffs hit its business. The 2026 forecast also includes one-off costs related to the implementation of the cost efficiency programme, the company said in a statement. Puma’s share price jumped by 9.8% on Thursday.

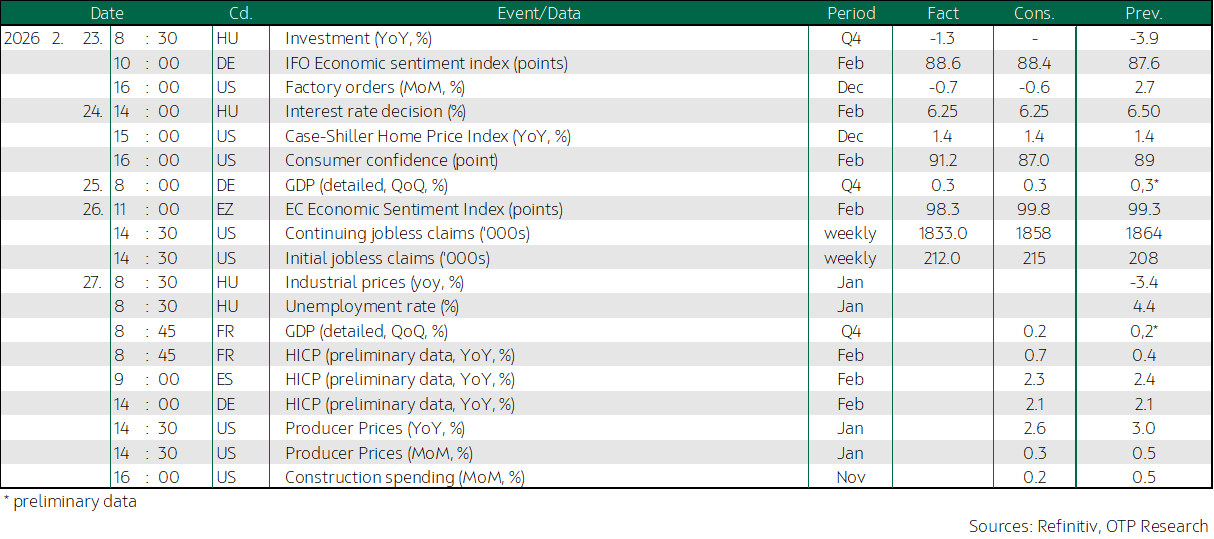

In the euro area, the European Commission's economic sentiment indicator (ESI) dropped to 98.3 points, from a three-year high of 99.3 in January. Thus the February figure missed expectations of 99.8. The sentiment deteriorated in the services, industry, and construction sectors.

The CEE region’s stock indices lagged behind yesterday: Hungary’s BUX (-0.2%), Czechia’s PX50 (-0.9%) and Poland WIG20 (-0.9%) all ended in the red.

Nvidia’s share price tumbled 5.5%

Of America’s leading indices, the industrials-heavy Dow Jones’ stagnation marked the best performance. The S&P500 slipped 0.5%, while the tech-heavy Nasdaq Composite fell 1.2%. Nvidia, which has more than 10% weight in the NASDAQ, failed to impress investors: despite its better-than-expected results, the stock price tumbled 5.5%. The Philadelphia SE Semiconductor index slid 3.2%. Of the S&P500’s eleven main sectors, technology (-1.8%) and communication services (-0.75%) suffered the biggest losses, while financials excelled with 1.3% gain.

Warner Bros Discovery said Paramount’s revised offer of 31 USD/share would beat its existing deal with Netflix, giving the streaming giant four business days to respond — or exit the bidding war for the prestigious Hollywood studio. Paramount shares skyrocketed 10%. Netflix eventually backed out of the deal, and its shares shot up 10% in after-hours trading.

The weekly US unemployment figures were not particularly surprising.

The third round of US-Iranian talks was held in Geneva on Thursday. The critical point now appears to be that while Iran has shown willingness to negotiate on its nuclear programme, it is refusing to expand the scope of the talks, particularly on its ballistic missile programme and support for militant groups in the region.

The sour sentiment on global stock markets made investors seek bonds instead

In the unsupportive sentiment on global stock markets, investors preferred bonds of developed economies, causing US and European bond yields to decline by 1-3 basis points. The US 10-year yield is now nearing 4%, while the German 10-year benchmark sank below 2.7%. The increasing risk aversion has also strengthened demand for the dollar, so the EUR/USD dropped by a quarter of a percent, to around 1.175.

The strengthening dollar has weakened the CEE region’s currencies yesterday as well: they depreciated by 0.1-0.3% against the euro, while the forint’s weakening sent the EUR/HUF to 376, from a two-and-a-half-year high of 375. Hungary’s bond yields were more or less stagnant yesterday, after a 10-basis-point decline on Wednesday: the 10-year benchmark yield inched up, exceeding 6.4%. At Thursday's auction, the ÁKK sold HUF 40 billion worth of 12M discount Treasury Bills (it had offered HUF 30 billion), at an average yield of 5.96%. There was exceptionally strong demand for the 2032 fixed-interest-rate green bond: bids surpassed HUF 130 billion, of which the agency accepted HUF 75 billion. There was subdued demand for the 10Y floater; only half of the announced HUF 20 billion was sold.

Today’s highlights

Asia was heading for moderate gains ahead of today’s close. Japan’s Nikkei (+0.2%), Korea’s KOSPI (+0.4%), Hong Kong’s Hang Seng (+0.9%), and China’s SSEC (+0.4%) all traded in positive territory.

On Wednesday, Japan’s Prime Minister Sanae Takaichi elected two dovish candidates to the Bank of Japan’s board of directors. This raises doubts about how much monetary policy can be tightened further, and whether it will affect monetary policy normalization in the longer term. The decision has somewhat surprised the markets; many expected her to choose more moderate candidates.

In Hungary, the KSH statistical office publishes January industrial producer prices and unemployment rates today.

In Europe, France, Spain and Germany release February inflation data. The indicators from large member states usually give a good idea of the euro area's gauge, but this time it is a bit more difficult because Italy’s preliminary data will be published next week (on 3 March), at the same time as the eurozone’s data. In the USA, the January producer price index will see the light of day.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more