OTP Morning Brief: Stock markets fell again amid escalation risks

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Western European indices declined once more, as the positive sentiment seen earlier in the week was replaced by fears of escalation. Several key policymakers commented on the possibility of an ECB rate hike. In parallel with Europe, U.S. stocks also posted sharp losses. After the market closed, Trump eased pressure on Iran. It was a difficult day for the communications sector. Concerns about inflation and potential rate hikes pushed developed-market bond yields higher. Asian markets moved in an uncertain direction. Today, domestic labor market data and the balance of payments will be worth watching.

Western European markets closed in the red again

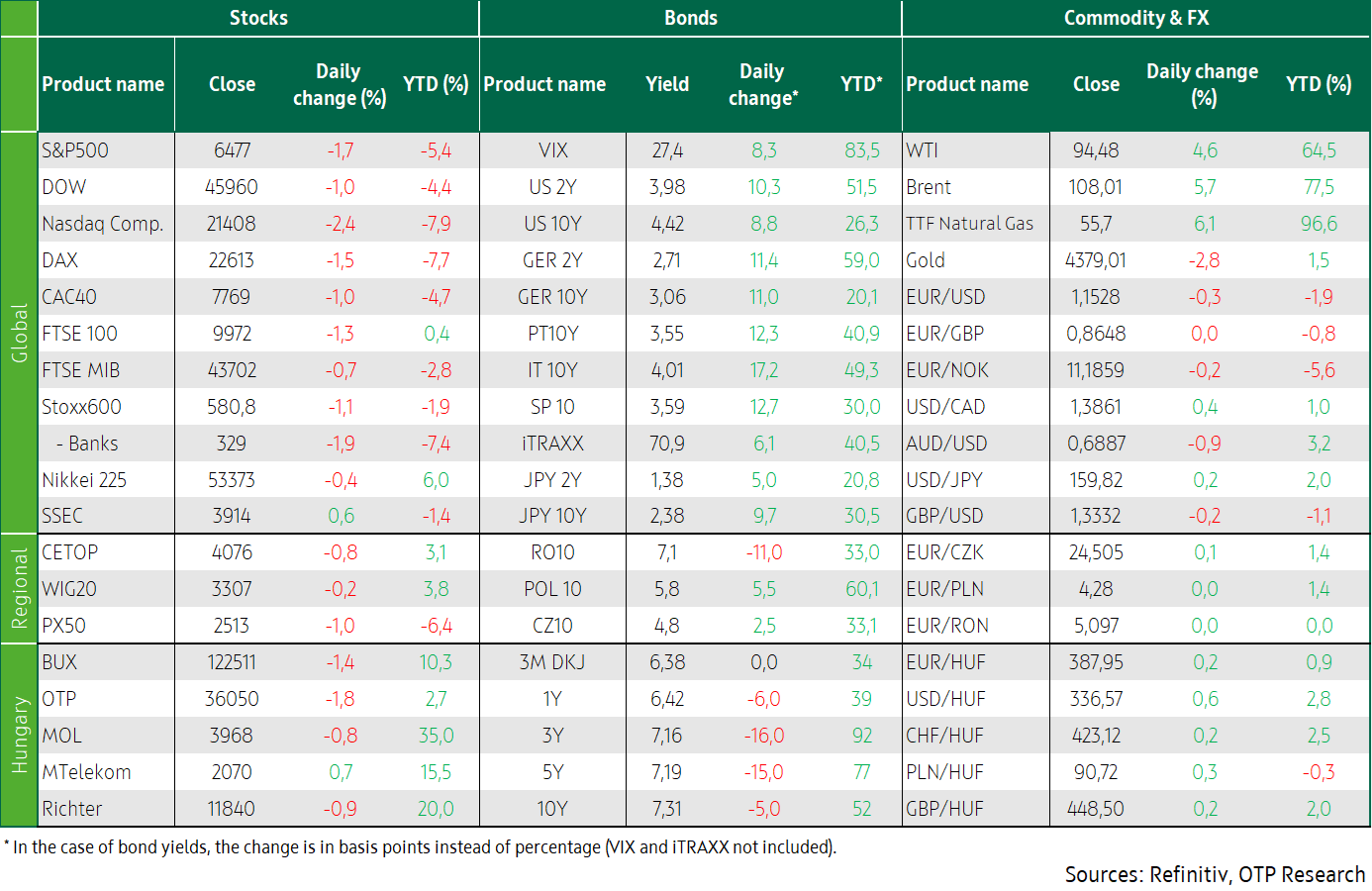

Western European markets fell again on Thursday as investors faced the possibility of an upcoming ECB rate hike and fading hopes for a swift resolution to the Middle Eastern conflict. According to Joachim Nagel, President of the German Bundesbank (and thus an ECB Governing Council member), a rate hike remains an option for the ECB. His remarks came just one day after President Christine Lagarde signaled that the central bank is prepared to act at any meeting to keep inflation close to its 2% target. The pan-European STOXX 600 index dropped 1.1%, breaking a three-day winning streak. Among the major national indices, the DAX saw the steepest decline, falling 1.5%. Industrial companies and banks, two cyclical and recession-sensitive sectors both slipped by nearly 2%, while the technology sector fell by 2.3%. However, the decline was led by mining companies: shares of Boliden plunged 19.9% after the company announced that exceptionally strong seismic activity was expected to hurt its quarterly results, while falling metal prices also weighed on the sector. Another notable mover was Sweden’s H&M, which dropped 3.6% after its quarterly revenue missed expectations.

The downturn also affected Central and Eastern Europe: the Polish index fell 0.2%, the Czech index 1%, and the Hungarian market declined by 1.4%. Most Hungarian blue chips ended in negative territory, with OTP posting the largest loss at 1.8%, while Magyar Telekom rose by 0.8%.

U.S. stocks tumbled on fears of Middle East escalation, though Trump may ultimately postpone the strike on energy infrastructure

The Nasdaq plunged 2.4% on Thursday, extending a downward trend that had briefly paused in recent days, while the S&P 500 fell 1.7% and the Dow declined 1.0%. Investors sought safe-haven assets amid fears that the U.S.-Israeli conflict with Iran could escalate further, driving oil prices higher and intensifying inflation concerns. As a result, equity indices erased Wednesday’s gains, when markets had still been pricing in a potential de-escalation of the conflict. President Donald Trump stated that Iran must reach a deal with the United States or face a continued series of attacks, and also warned that he could take control of Iran’s oil reserves. A senior Iranian official told Reuters that the U.S. proposal—which aims to end nearly four weeks of fighting—is “one-sided and unfair,”though he did not rule out the use of diplomacy. After the market closed, however, Trump announced that, at the request of the Iranian government, he would postpone strikes on Iran’s energy infrastructure by ten days, until April 6. He also said that negotiations with Tehran were “going very well.”

Among the S&P 500’s eleven major sectors, most ended the day lower. The energy sector was the biggest gainer, rising 1.6%, while the only other sector posting a percentage increase was the defensive utilities sector, which edged up 0.2%. The worst performers were communication services, which fell 3.5%, and technology, down 2.7%. The sharp decline in communication services was partly driven by a court ruling that found Meta and Alphabet liable for harms done to children by social media platforms, adding to a growing wave of lawsuits. Meta shares sank nearly 8%, while Alphabet dropped more than 3%. Brent and WTI crude prices surged by almost five percent on Thursday amid rising tensions in the Middle East.

On the data front, initial jobless claims increased by 5,000 to 210,000, in line with expectations, while continuing claims dropped to their lowest level in nearly two years. This points to a still-resilient labor market despite the inflationary risks posed by the Middle Eastern conflict, potentially giving the Federal Reserve room to maintain current interest rate levels.

Developed-market bond yields rose on inflation and rate-hike fears

Surging oil prices on Thursday significantly heightened inflation concerns and expectations of further rate hikes. In the United States, market pricing began to shift toward the possibility that the Federal Reserve may even be forced to raise rates later this year. The U.S. 10-year Treasury yield climbed by nearly 10 basis points, surpassing 4.4%. Yields rose sharply in Europe as well: the German 10-year increased by 13 basis points, the French by 15, and the Italian by 19. The German 10-year yield is approaching 3.1%, reinforcing fears that it may break out of its previous trading range to the upside and remain above 3% on a more sustained basis. The U.S. dollar strengthened further, with the euro weakening 0.2% to around 1.154 in EUR/USD trading.

In regional FX markets, there were no major moves; Central and Eastern European currencies weakened by about 0.1–0.2%, while the forint remained below 388. On the domestic bond market, demand was strong for the 15-year fixed-rate bond, with HUF 50 billion sold at an average yield of 7.31%. By contrast, neither the discount treasury bill nor the floating-rate bond attracted investor interest: the debt agency managed to sell only HUF 8 billion of bills and a mere HUF 2.5 billion of the floating-rate bond. Reference yields recorded early in the afternoon declined compared with the previous day: the 3–5-year segment fell by 10–15 basis points, while the 10-year benchmark yield stood at 7.3%.

Today’s highlights

Geopolitical uncertainty led to mixed movements in Asian markets: the Nikkei and the Kospi both fell by 0.4%, while the SSEC rose by 0.5% and the Hang Seng gained 0.6%.

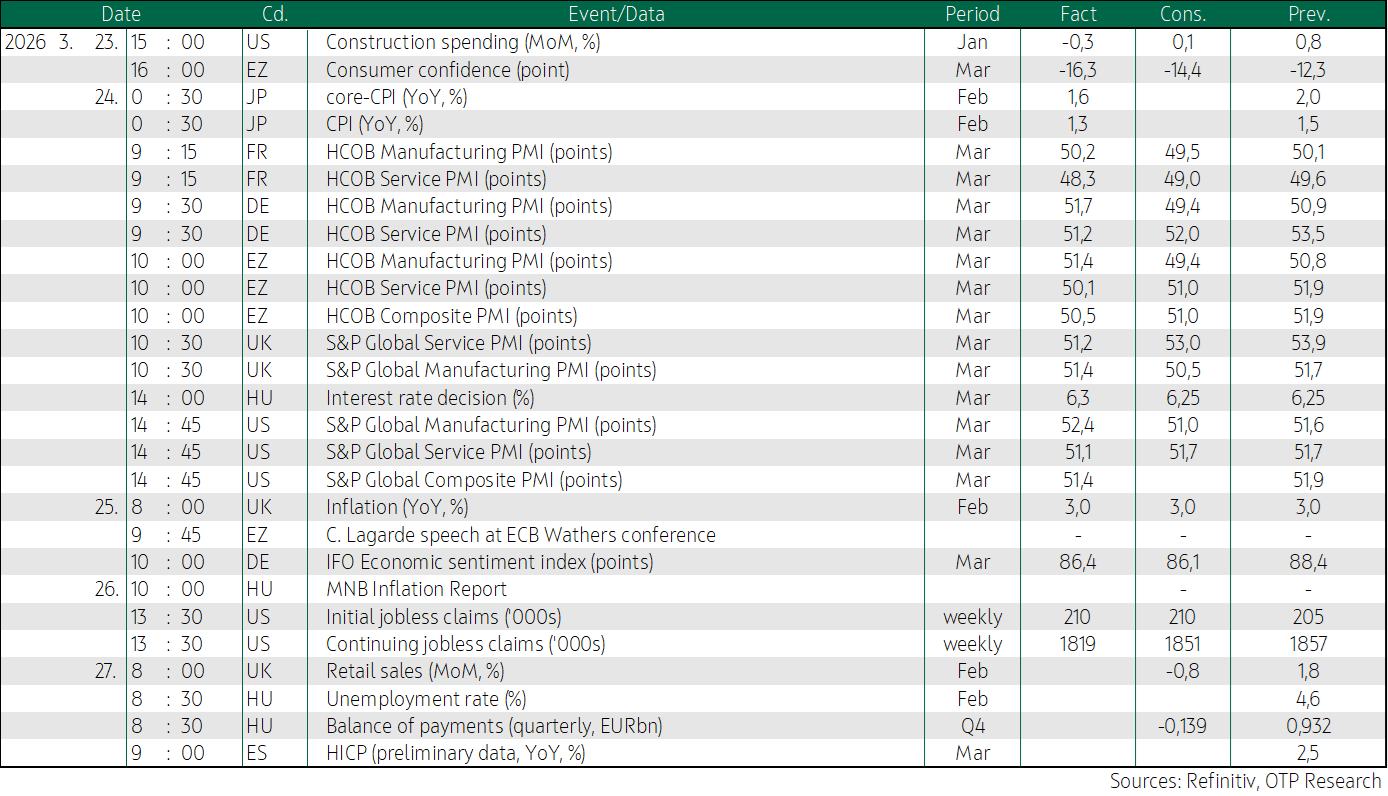

Today, attention will turn to the United Kingdom’s February retail sales data, while in Hungary the February labor market statistics and the balance of payments data for the fourth quarter of last year will be released.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more