OTP Morning Brief: Europe’s stock markets closed at record highs

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Europe’s main stock indices rose to new highs on Wednesday. The sentiment was also buoyant in the CEE region, where the BUX was top gainer. On Wall Street, the AI sector helped the Nasdaq rise the most. Nvidia's earnings report reinforced optimism for the technology sector. A naval incident in Cuba added to geopolitical tensions. OPEC+ considers boosting production ahead of summer demand. The HUF has appreciated, and Hungarian bond yields fell notably. Hungary’s ÁKK raised additional USD 1.2 billion worth of financing in a private placement. Today, markets await the eurozone’s economic sentiment indicator and US jobless claims data.

Europe’s major indices closed at record highs

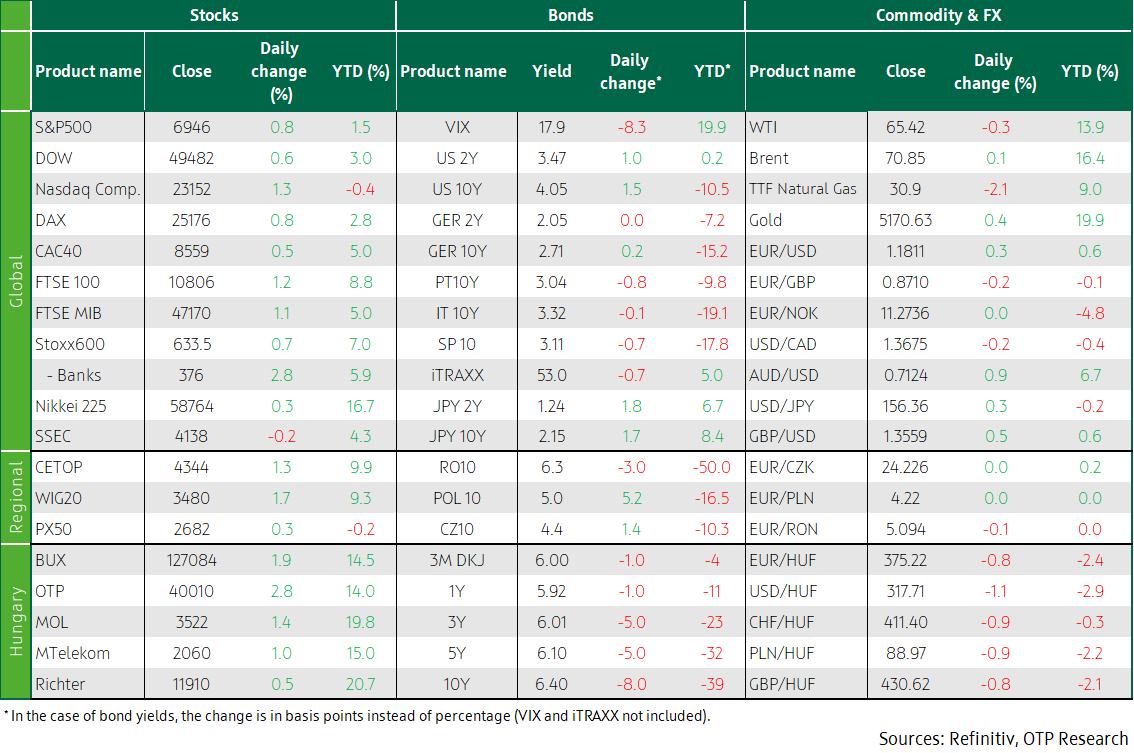

On Wednesday, most of the leading European indices went to record highs, including the DAX (+0.8%), the CAC 40 (+0.5%), the FTSE 100 (+1.2%) and the Stoxx 600 (+0.7%). The materials (+2.8%) sector posted the biggest gain. Banking shares surged by 2.6%, as global market sentiment improved after the US-based AI startup Anthropic entered into partnerships with several companies and launched new AI plug-ins. Some analysts opine that banks are exposed to the disruptive effects of AI innovations, so signs of successful integration alleviate concerns about margin squeeze. The performance of the financial sector also benefited from the jump in the share prices of HSBC (+8.0%) and Santander (+4.8%). The former's outstanding performance stemmed from raising its profit target after its annual profit exceeded expectations, despite recording a one-off USD 4.9 billion write-off. The worst-performing sector on Wednesday was the food sector (-1.9%), owing to Diageo's 12.7% dive after the drinks manufacturer had lowered its profit expectations for the second time in four months and also reduced its dividend.

The positive sentiment was also felt in the CEE region, where Czechia’s PX 50 (+0.3%), Poland’s WIG 20 (+1.7%), and Hungary’s BUX (+1.9%) all advanced on Wednesday. In Budapest, Mol (+1.4%) and OTP (+2.8%) bounced back from Tuesday’s weak performance.

The return of AI optimism helped the NASDAQ rise notably

Wall Street’s indices closed higher on Wednesday, continuing a rally led by technology stocks, and hitting two-week highs as concerns about AI faded in the face of renewed optimism about the potential benefits of the new technology. Nvidia, the engine of the rally, reported fourth-quarter revenue of USD 68.13 billion, beating analysts’ expectations. Its shares grew about 3% in after-hours trading, after rising 1.6% in premarket trading. The positive news about artificial intelligence helped the NASDAQ lead the pack with a 1.3% gain, followed by the S&P500 (+0.8%) and the Dow Jones (+0.6%). Within the S&P, the technology sector (+1.9%) was the best performer, second to it was financials (+1.7%). Companies such as SMC (+7.9%) and Intel (+1.7%) contributed to the former. Axon Enterprise shot up 17.6% after the manufacturer of stun guns and other law enforcement equipment reported better-than-expected fourth-quarter earnings. The bidding war between Netflix and Warner continued as the latter made a new bid to acquire Paramount, which caused Netflix shares to soar 6.0%.

Adding to geopolitical tensions, Cuban armed forces killed four people and wounded six on board a ship sailing from Florida, which had entered Cuban territorial waters on Wednesday and opened fire on a Cuban patrol boat. Prior to the unusual incident, the USA had blocked virtually all oil shipments to the island, increasing pressure on the Cuban government. Wednesday's incident could add fuel to the fire in the conflict between the two countries.

According to Reuters, OPEC+ may consider boosting its oil production by 137,000 barrels per day from April as peak summer consumption approaches, and higher oil prices due to tensions between the USA and Iran may make the move favourable. Brent rose by 0.3%.

The forint strengthened markedly, Hungary’s yields fell sharply; Hungary’s ÁKK raised additional USD 1.2 billion worth of FX financing in a private placement

Developed economies’ bond markets continued a directionless trading yesterday. The US 10Y yield remained at 4.05% and the German one near 2.7%. A slight dollar weakening drove the EUR/USD higher, to 1.18.

Although there was no significant movement in the other currency markets of the CEE region, the forint strengthened by almost 1% against the euro, thus the EUR/HUF sank to 375. The situation was similar in the bond market, even though developed markets’ yields stagnated and the direction was not clear in other CEE countries either – Czechia’s yields edged lower, Polish ones rose –, Hungary’s yields fell by 5-7 basis points at the belly of the curve, and by 10 basis points in the 10Y-20Y segment. The ten-year yield slid to a one-year low of 6.4%. Citing Bloomberg, the Portfolio.hu portal reported that Hungary’s ÁKK had raised USD 1.2 billion in foreign currency financing, in a private placement, following the 2035 bond issuance in mid-2025. The ÁKK has not announced the transaction so far, presumably because US regulations prohibit the publication of details until financial settlement has been completed. There was subdued demand at the ÁKK's auction of three-month discount Treasury Bills, where the planned amount, HUF 30 billion, was sold at an average yield of 6.03%.

Today’s highlights

Asia’s markets also fared well, thanks to the supportive international sentiment; Japan’s Nikkei upped 0.3%, and Korea’s Kospi surged 3.7%, to a new high. In China, however, the SSEC (-0.2%) and the Hang Seng (-1%) both sank.

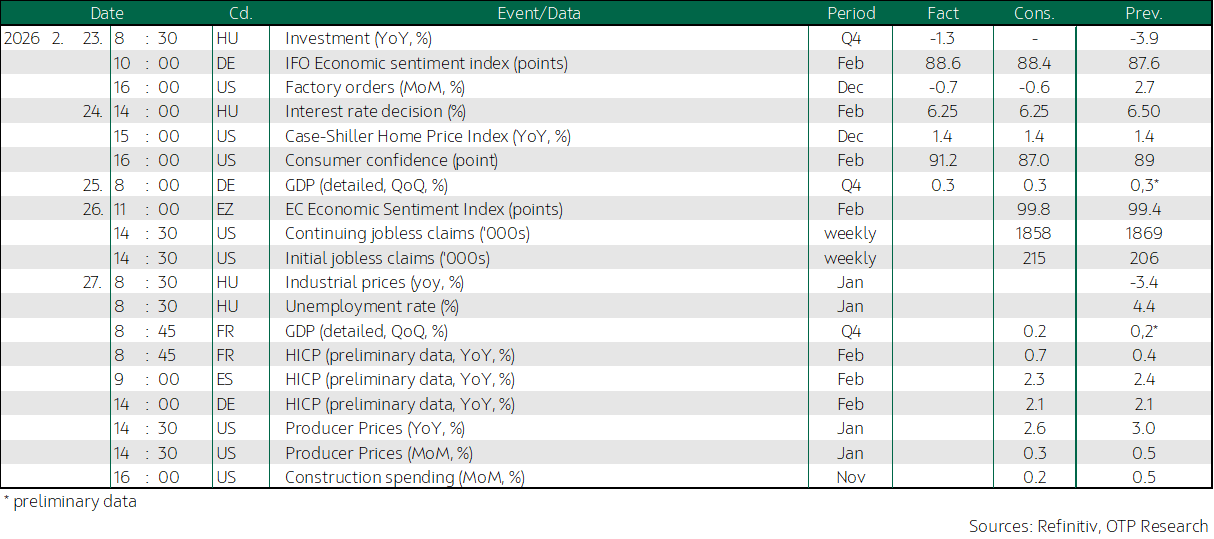

Today, the Eurozone Economic Sentiment Indicator (ESI) is worth checking, as is the weekly jobless claims statistics from the USA.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more