OTP Morning Brief: European and US markets closed last week with losses

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

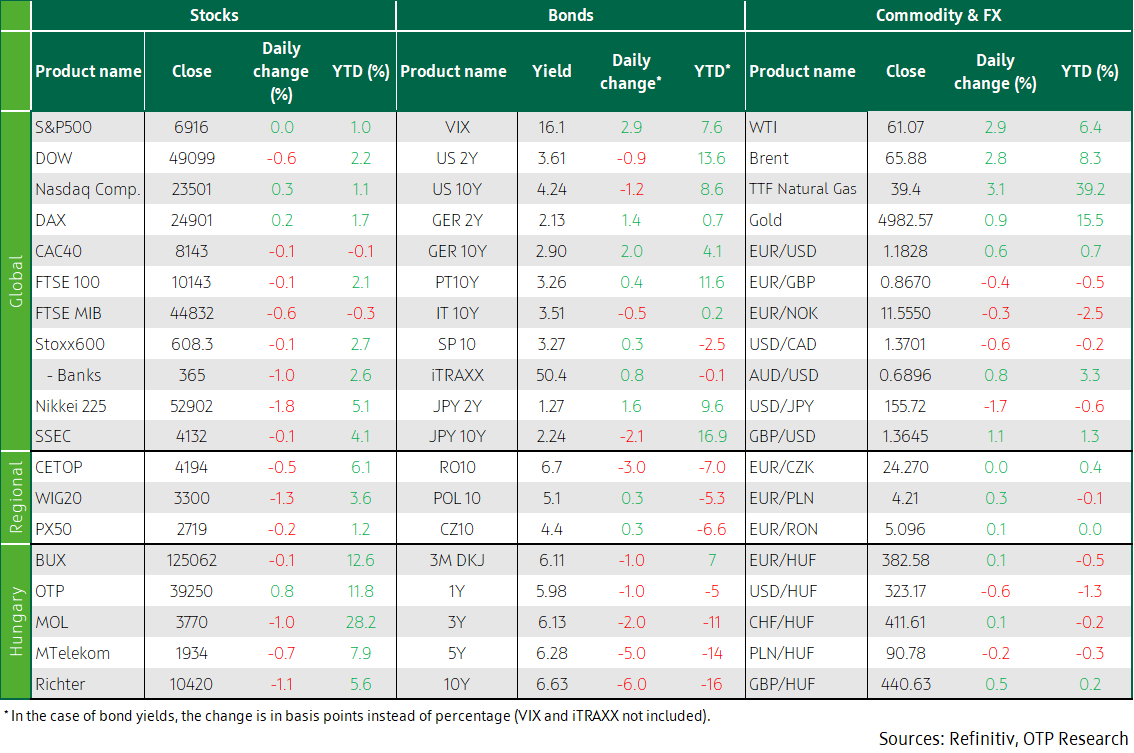

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Europe’s leading indices ended last week in the red, the trilateral talks in Abu Dhabi were fruitless. US indices also dropped last week, PMIs showed weaker-than-expected activity. Following the Greenland tensions and Davos speeches, US bond yields sank, European bond yields rose, while the dollar weakened. The yen’s marked strengthened held back the performance of Japanese stocks. This week’s major events are the rate decisions of the US Fed and Hungary’s MNB, as well as GDP data from across Europe.

Europe’s key indices declined week lower, trilateral talks in Abu Dhabi were inconclusive

European stock indices edged lower on Friday, dragging down last week’s performance, as investors remained cautious as they weighed the potential trade risks of tensions with the USA over Greenland. Of the major indices, France’s CAC 40 and the UK’s FTSE 100 inched down 0.1% each, while Germany’s DAX nudged 0.2% higher, thus the Stoxx Europe 600 dipped 0.1% on Friday. Of the latter’s sectors, telecommunications rose by 1.6%, while the insurance (-1.6%), and the travel & leisure (-1.4%) sector slipped. In individual stocks, Ericsson shot up 10.5% as the Swedish telecom equipment maker’s Q4 profit beat expectations, and it announced a share buyback programme. Adidas shrank by 5.7% after brokerage RBC downgraded the sportswear maker’s shares. Its rival Puma nose-dived 14.1%. Over the past week, the Stoxx 600 slipped 1%, largely dragged down by the DAX (-1.6%).

The January reading of HCOB’s Eurozone Composite Purchasing Managers’ Index remained at the previous month’s level, 51.5, slightly missing market expectations of 51.8. Despite its slowdown, the services sector kept the region above the psychological 50 mark (51.9, after the previous month’s 52.4), while the manufacturing index rose slightly (49.4, up from 48.8 in December). New orders increased for the sixth month, although at the lowest rate in four months, thanks to shrinking export orders. Despite the expansion in output and new business, companies slightly reduced employment. Germany’s PMIs came in better than expected, with manufacturing standing at 48.7 points (estimate: 47.8) and services at 53.3 points (vs. 52.5). In France, manufacturing exceeded expectations by half a point, standing at 51 points, while services disappointed (47.9 vs. 50.5). In the case of the United Kingdom, the S&P measure of services and manufacturing both surpassed analysts' predictions.

On the geopolitical front, the Russian-Ukrainian-American trilateral talks held in Abu Dhabi ended inconclusively. However, US officials spoke positively about the talks, indicating that the parties were ready for further negotiations. The talks were also complicated by the fact that Russia’s nighttime airstrikes on Kiev left more than one million Ukrainians without electricity in the harsh winter cold.

The sentiment in the CEE region was negative on the last day of last week. The BUX and the PX50 dropped slightly and the WIG 20 lost 1.3%. Of Hungary’s blue chips, only OTP grew by 0.8%, while Richter and MOL lost more than 1%. each Nonetheless, the BUX gained 2.2% last week.

US indices also ended the week in the red, PMIs showed weaker-than-expected activity

America’s stock market closed mixed on Friday: the Dow Jones slid 0.6%, mainly dragged down by Goldman Sachs (-4%), the S&P 500 practically stagnated, while the Nasdaq (+0.3%) extended its gains, amid easing geopolitical tensions, propelled by stocks such as Nvidia and AMD. Meanwhile, Intel slumped 17% owing to weak guidance. Although the market began to gain momentum in the middle of the week as Donald Trump backed down on the tariffs planned for European countries, alleviating investors’ fears. Unfortunately this did not save the week: although the Nasdaq's weekly loss was trivial, the S&P 500 (-0.4%) and the Dow (-0.5%) slipped last week. Trump took aim at Canada over the weekend, threatening 100% tariffs if it makes a trade deal with China.

The S&P's January U.S. purchasing managers' indices showed but tiny changes: the manufacturing PMI upped a tenth of a point and the services sector was flat, bringing the composite PMI to 52.8 (from 52.7 in December), but the figures for both sectors fell short of analysts' expectations. A pick-up in new orders offset a weak labour market and cost pressures from tariffs, while export orders fell to a nine-month low. Business confidence has declining somewhat, partly due to high prices, geopolitical concerns, and uncertainty about government policy. The labour market has been sluggish, reflecting cost-cutting by companies and subdued demand, even though some firms continue to struggle with labour shortages.

Brent crude futures jumped more than 2%, to around 65.8 USD/barrel on Friday, ending a fifth straight week higher, supported by geopolitical and supply-side risks. The rise in prices was fuelled by US President Donald Trump's latest warning to Iran, saying that the United States was sending an ’armada’ of warships to the country. Supply concerns were further compounded by a production halt at a key oil field in Kazakhstan.

Following Greenland tensions and Davos speeches, US bond yields fell, European bond yields rose, while the dollar weakened

Geopolitical tensions over Greenland, the Davos conference, US inflation data and Friday's confidence indices made last week eventful. On Friday – and thus throughout last week – US bond yields edged lower due to weaker-than-expected US confidence indicators. The 10Y yield eventually sank back to around 4.2%. The market still expects the Fed to cut rates via two 25-basis-points reductions in 2026. In contrast, Japan’s bond yields closed near 2.26% on Friday, in an increase of two basis points in one day and nearly six basis points in one week, but were also at a 30-year high 2.35% in the middle of last week. Reasons included political uncertainty, fears of the new government's deficit-increasing measures, and the communication of the Bank of Japan, which has left interest rates at 0.75% this time but suggested that interest rate hikes may follow (the market expects two 25-basis-point hikes from the BoJ this year). These fears were only partially dispelled by the Japanese government's market-calming communication, which included reducing long-term bond issuance and hinting at possible help from the Bank of Japan. In Europe, most bond yields rose last week, partly because the tension over Greenland clearly means that the continent will have to spend more on its own defence, and partly because the confidence indices published on Friday showed an unbroken recovery. Germany’s 10Y Bund yield jumped by 2 basis points on Friday, growing nearly 10 basis points in a week, to 2.9%, the upper end its post-pandemic trading range. The dollar, which was already weakening due to the Greenland issue, received another blow on Friday from weaker-than-expected US and stronger-than-expected European confidence indices. The EUR/USD rose by 0.5% on Friday, and by 2% in a week, to 1.182, heading for a five-year high.

The easing of geopolitical tensions related to Greenland and the weak dollar helped the CEE region’s currencies last week. The koruna (CZK) closed flat week-on-week, but the zloty (PLN) and the forint (HUF) strengthened against the euro. The EUR/HUF declined from 385 to 382 in a week, thus once again approaching the two-year low seen before the MNB’s December interest rate meeting. Hungary’s benchmark government bond yields declined by 2-7 basis points on Friday and by 5-10 basis points last week; the 10Y one fell closer to 6.6%, its lowest in almost a year.

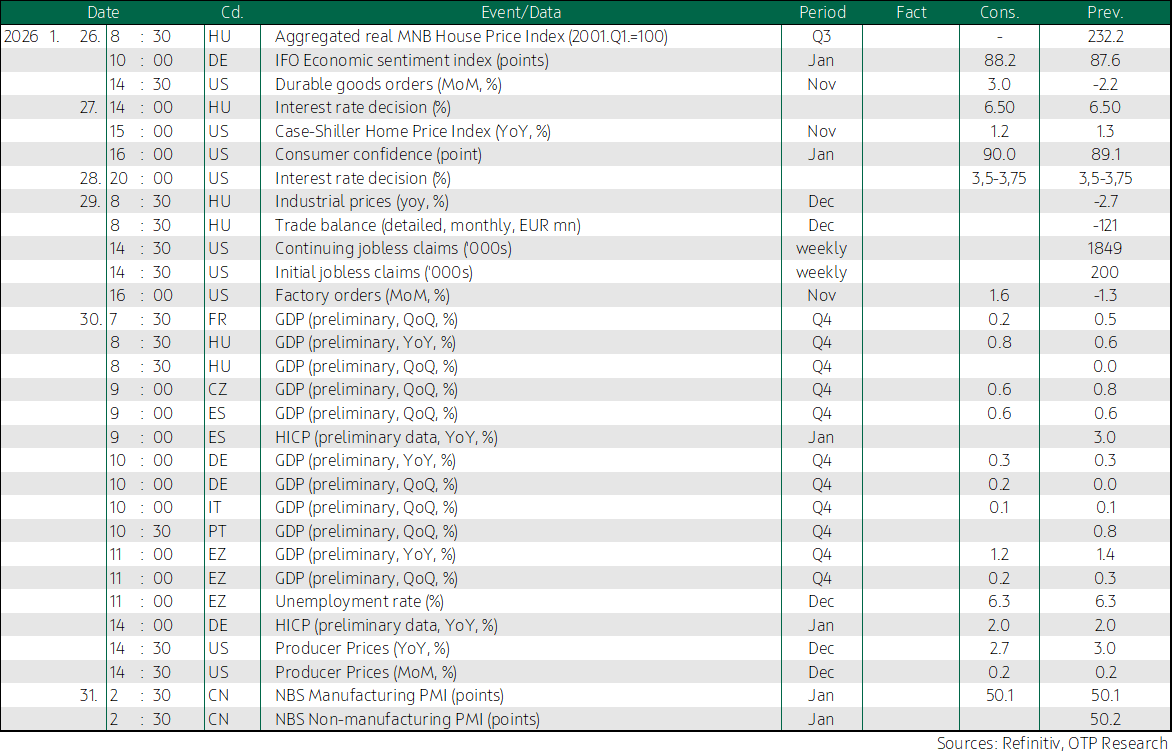

Today’s highlights

The Nikkei fell 1.8% today as the yen strengthened to its strongest in three months, 153.92, versus the dollar, thanks to the greenback’s weakening and as investors perceived signs of possible intervention by the Bank of Japan and the Fed. The strong yen weighed on the shares of exporting companies, including Toyota (-3.2%), Honda (-3.7%), and Rubber (-2.2%). Meanwhile, China’s indices posted negligible losses.

There will be several important events this week, including the MNB's interest rate decision in Hungary. In line with the market expectations, we think interest rates will remain unchanged in January. Nevertheless, the central bank's communication on its assessment of recent events and the conditions for interest rate cuts may have a significant impact on FI and FX market developments. In the USA, the Fed's Open Market Committee will conclude its first interest rate decision meeting of the year on Wednesday; market prices imply that interest rates will almost certainly remain at their current levels.

In addition to monetary policy decisions, several European countries, including Hungary, release fourth-quarter GDP data this week.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more