OTP Morning Brief: Global financial markets opened the week with huge swings

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

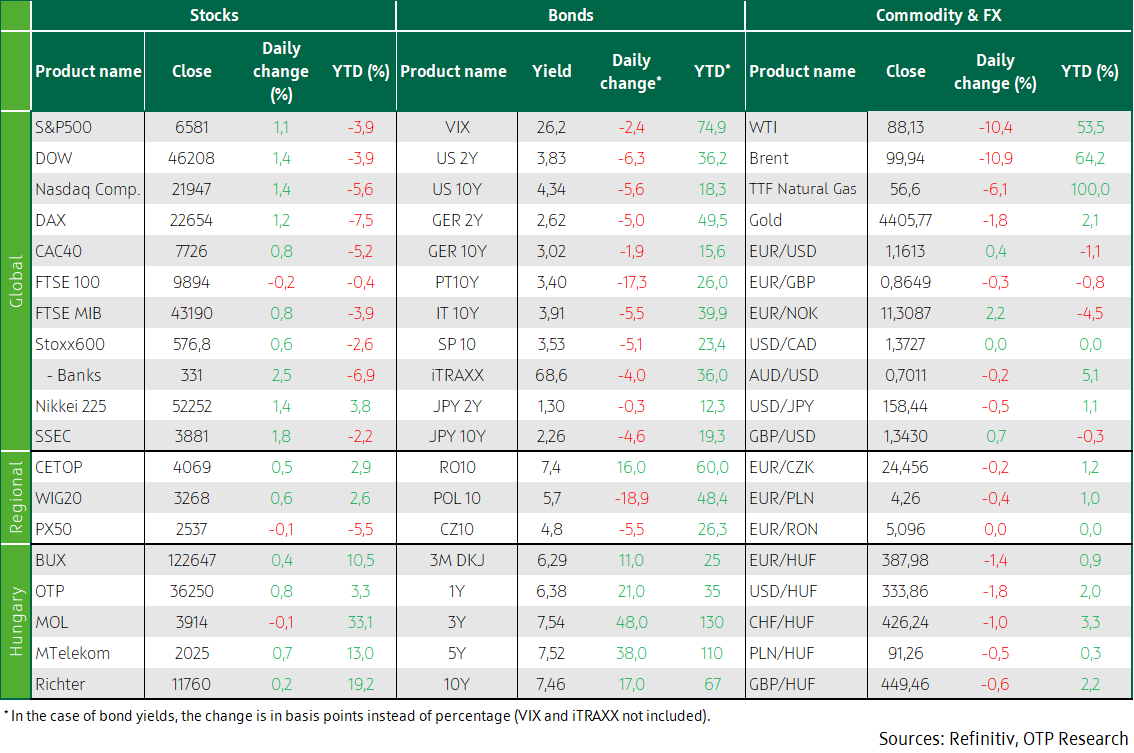

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Donald Trump's ultimatum for Iran and a subsequent U-turn caused huge swings on Monday. Given the growing tension on energy markets and the steep rise in US yields on Friday, trading in the developed world’s equity, bond, and currency markets started gloomily on Monday. Donald Trump’s words on negotiating with Iran and postponing strikes on Iran’s energy infrastructure for five days caused sharp reversal. Most of Europe’s stock indexes picked up, ending a three-day losing streak; Wall Street’s key indices gained over 1%. The EUR/USD fell below 1.15, before a rebound to near 1.165. Germany’s 10Y yield rose, then sank below 3%, remaining in its post-covid trading range. The EUR/HUF dropped 10 forints, to 387. Hungary’s bond yields briefly grew by 50 basis points, to 8%, before falling that much. In addition to the Middle East development, PMIs from the EZ and USA, as well as the MNB's policy decision are worth watching today.

Most stock markets in Europe closed higher, ending a volatile day

Following Monday’s plunge in Asia’s stock markets, trading in Europe also started on a week note as the USA and Iran had traded threat over the weekend, further escalating the Middle East conflict. While Europe’s stock indices subsided, Brent crude price headed towards 115 USD/barrel, WTI exceeded USD 101, and the price of natural gas in Europe approached 70 USD/MWh. The pressure eased during the day after President Trump lifted the 48-hour ultimatum for Iran to open the Strait of Hormuz and suspended military strikes on Iran’s energy infrastructure for five days after the USA, according to Donald Trump's post, had held constructive and productive talks with Iran. Although Iran later denied such talks, Donald Trump's optimistic announcement was enough to send energy prices plummeting and stock markets soaring. The Stoxx600 ended 0.6% higher, reversing a 2.5% fall. The DAX and CAC40 grew by 1% each, but the FTSE100 edged lower on Monday. Mining companies, financials, and travel & leisure led the gains. Brent's 9% fall kept the energy sector under pressure, making it Monday's loser.

In individual names, Telekom Italia shares jumped nearly 5% on news that Poste Italiane, Italy’s postal service provider, said it would buy the former telephone monopoly for EUR 10.8 billion. Poste Italiane shares slumped almost 7% on the announcement. Germany's Delivery Hero jumped nearly 8% after selling its Taiwanese home delivery service for USD 600 million. Danish jewellery maker Pandora soared 9%, benefiting from falling metal prices.

In the eurozone, consumer confidence deteriorated sharper than expected; the preliminary March gauge fell below -16, reflecting a significant weakening in consumer confidence following the outbreak of the war in Iran.

In Europe’s natural gas market, TTF price fell below 57 EUR/MWh by the end of Monday’s session. This is consistent with more than 4% decline and 15% intraday change – yet the current level is double the price at the end of 2025.

In the CEE region, Hungary’s BUX edged up 0.4%, lagging behind the WIG20’s 0.6% increase, but it managed to fully erase the almost 2.5% loss made earlier in the day. Hungary’s benchmark was powered by OTP (+0.8%), MTelekom (+0.75%), and Richter, while MOL closed in the red.

U-turn on Wall Street after Donald Trump's announcement

Although Monday’s decline in US stock indices was not as dramatic at the beginning of trading as in Europe or in Asia, the rapid recovery was spectacular: the Dow, S&P500 and Nasdaq Composite all increased by more than 1%. President Trump claimed that he had ordered the military to postpone attacks on Iran’s power plants after “fruitful talks” with Tehran. However, the speaker of the Iranian parliament posted in social media that there were no talks with the USA, contradicting Donald Trump’s announcement that talks had taken place between the United States and Iran in recent days, during which the two sides had allegedly agreed on major points and that an agreement on resolving the war could be reached soon, Reuters reported.

Nevertheless, the market welcomed President Trump’s intention to negotiate a settlement: oil futures subsided, easing inflation fears, although previously priced-out expectations for a rate cut this year have not yet reversed. The VIX volatility index jumped to a two-week high of 31 points at the start of trading, from where it sank to around 26 points. The Russell2000 small-cap index, which is sensitive to higher interest rates, outperformed the large-cap index, finishing Monday's trading session 2.3% higher.

All S&P500 sector indices closed higher, particularly consumer discretionary (+2.5%), technology and materials (+1.5% each), while defensive sectors posted smaller gains. Fuel-heavy airlines and shipping companies rose sharply after the oil price reversal; Alaska Air, American Airlines and United Airlines took off roughly 4%. Norwegian Cruise Line, Carnival, and Viking Holdings were among the top performers, with gains of 5-6%. The banking sector also recovered, with leading US financial institutions and investment companies closing the day 1-2% higher.

WTI crude oil closed below 89 USD/barrel on Monday, down more than 9% from Friday, while the difference between the daily high and low was 15%. Brent crude oil closed near 100 USD/barrel, 11% lower than on Friday. The surge in oil prices earlier in the day stoked inflation and growth fears, which kept the stock markets under pressure in Monday morning's trading, but President Trump's announcement brought a sharp reversal.

Monday started with huge swings: the EUR/USD first fell below 1.15, then bounced back to nearly 1.165. After an initial rise, Germany’s 10Y yield fell below 3%, back to its post-covid trading range. The HUF appreciated by 10 forints, sending the EUR/HUF to 387. Hungary’s bond yields rose 50 bps, to 8%, before sinking that much

After the US ultimatum to open the Strait of Hormuz, as well as the attacks on Middle East’s energy infrastructure and threats of further strikes, Monday’s trading in the oil market started with an increase; the price of Brent jumped to 115 USD/barrel. Given the growing tension on energy markets and the significant increase in US yields on Friday, trading in developed economies’ stock, bond, and currency markets started gloomily on the first day of the week. However, Donald Trump's announcement on negotiation with Iran and postponing strikes on Iran’s energy infrastructure for five days brought a strong reversal. On Monday morning, Japan’s 10Y bond yield closed on a sour note, near multi-decade highs, above 2.3%. The day did not start well in Europe’s bond markets either: Germany’s 10Y yield rose from the top of its post-covid trading range and approached the 3.1% mark, while EUR/USD fell below 1.15. However, Donald Trump's about-face brought a turnaround: the 10Y German yield closed below the 3% breakout level, following an intraday drop of 10 basis points, and the EUR/USD finally rebounded 0.5%, to 1.165.

Monday's trading saw huge movements in the CEE region, including Hungary. CEE currencies weakened under the selling pressure. The HUF initially depreciated, trading at 396 against the euro. A wild rally began after Trump's about-face: the HUF strengthened by 10 forints, causing the EUR/HUF close at 387, as the forint strengthened by 1.5%. The zloty (PLN) appreciated by 0.5% and the koruna (CZK) strengthened by 0.3% versus the EUR. Similar swings occurred in the expected path of the base rate and in bond yields. At one point, the market was already pricing in that the MNB would have to raise the key interest rate to almost 8%, and in a completely illiquid trading, government bond yields were also drawing near 8% at their peak. The selling pressure eased by the afternoon, and the interest rate level priced in for the end of the year eased to 7.25%. Government bond benchmark yields, fixed in the early afternoon, reflected 7.5-7.6% levels, which exceeded Friday's benchmark yields by 40-50 basis points for 3Y–5Y maturities, and by 15-20 basis points for 10Y-20Y tenors. However, bond yields returned to the 7.3-7.4% range by the close.

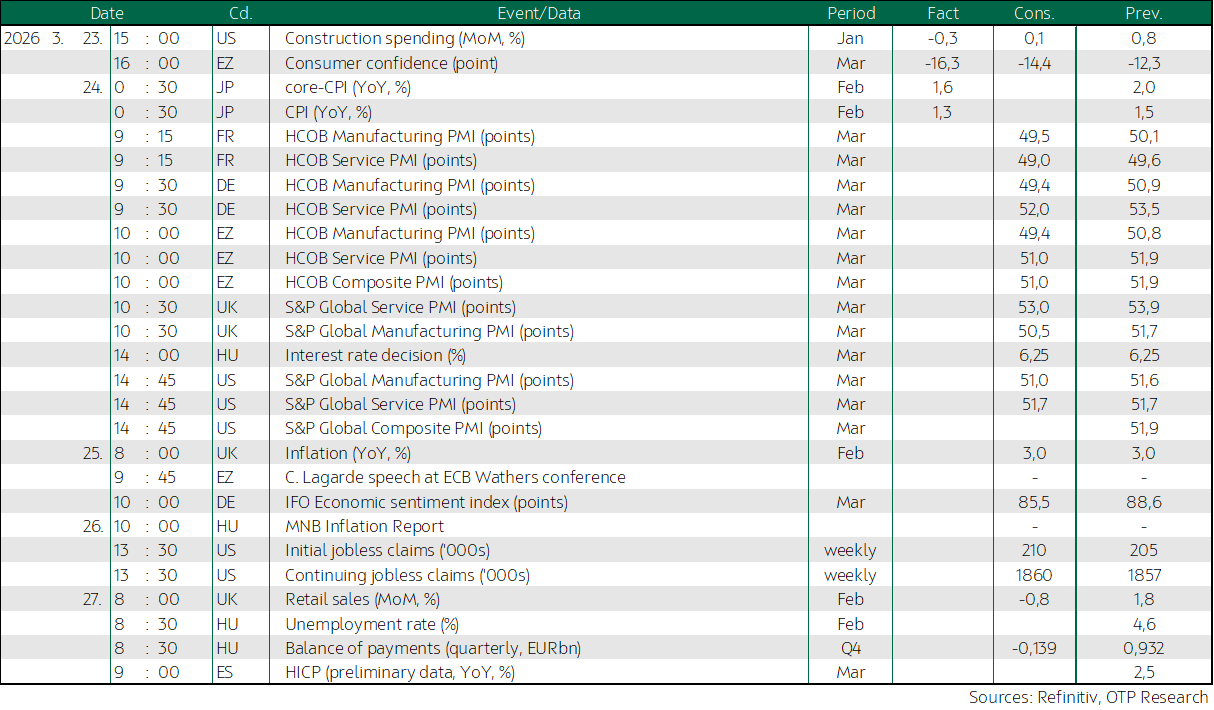

Today’s highlights

The leading stock indices in Asia-Pacific traded in the green ahead of today’s close, making up for Monday's reversal in European and US markets. Japan’s February inflation data reflected a slowdown in price increases; the month-on-month index decreased, the year-on-year indicator fell from 1.5% to 1.3%, and the core index dropped from 2% to 1.6% YoY. The preliminary data released today showed that the manufacturing and services sector PMIs also deteriorated in March.

Index futures did not bode well for today’s trading. It is hardly surprising, given the mixed news surrounding the US-Iran talks and Iran's overnight missile attacks on Israel. The Strait of Hormuz remained closed. Crude oil prices have already risen by 3-4% in Tuesday's trading.

Preliminary March PMIs from the eurozone, its member states, and the USA are due today. They are expected to have declined compared to February amid the Middle East conflict, rising energy prices, as well as inflation and growth fears.

In Hungary, the most important event of the day will be the MNB's interest rate decision. Hungary’s central bank is widely expected to leave the interest rate unchanged in the suddenly adverse international environment.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more