OTP Morning Brief: Global markets fell amid tariff uncertainty

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

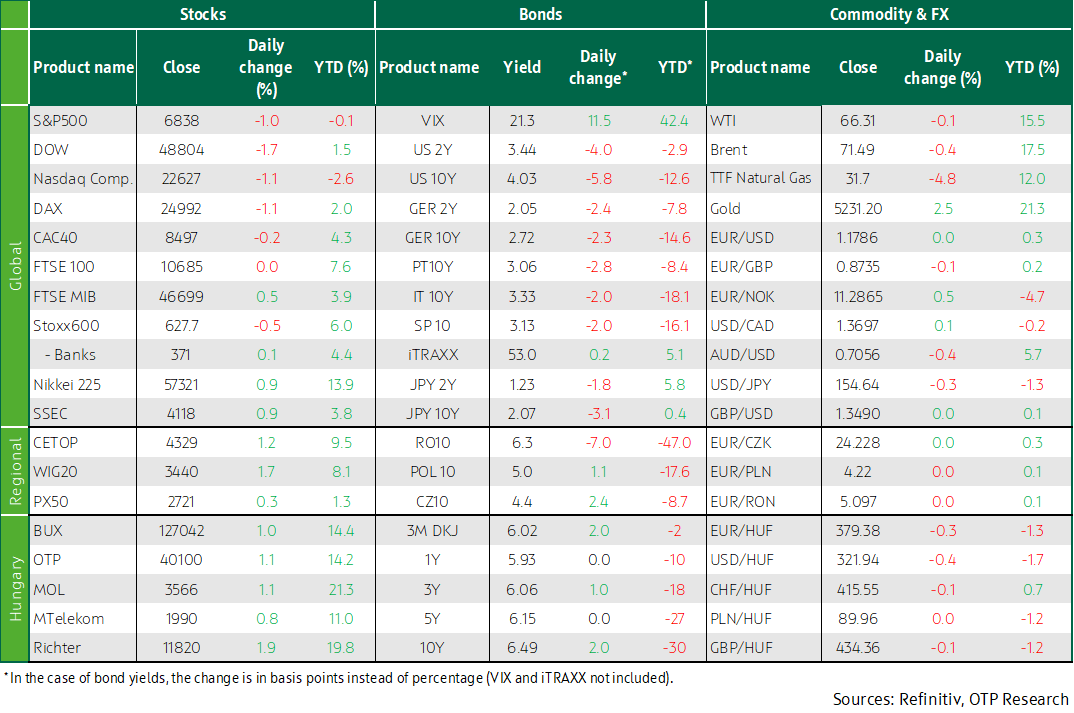

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Europe’s stock markets opened the week on a bad footing, amid renewed uncertainty over US tariff policy. Western Europe’s stock indices declined in the shadow of a possible new tariff war, but the BUX made up for Friday's loss. President Trump's global tariff announcements and fears about the AI reshuffle caused a minor sell-off in Wall Street on Monday, the major indices lost more than 1%. Many investors sought risk-free assets, thus long yields fell, and the EUR/USD closed below 1.18. The EUR/HUF ended at 379.4. Today the MNB’s Monetary Council makes interest rate decision, where the 6.5% base rate may be reduced by 25 basis points.

Western Europe’s stock markets retreated on Monday as tariff war flared up again

Europe’s stock exchanges started this week on a weak footing, as uncertainty over the US tariff war resurfaced on markets after the US Supreme Court on Friday overturned Donald Trump's country-specific tariff orders, in response to which the president imposed global tariffs of 10% and 15%. The Stoxx600 (-0.5%) and the DAX (-1.1%) slipped while the FTSE100 closed flat on Monday. One of the biggest losers was Novo Nordisk (-16.5%) as the latest trials indicated that the Danish drugmaker’s new anti-obesity drug, CagriSema, was less effective than Eli Lilly's Tirzepatide. However, industrials and financial services also fell even sharper on Monday. In industrials, Siemens Energy slipped 1.8% and Airbus nose-dived 3.5%. The broader defence sector retreated 1.6%, after Reuters reported that Iran was willing to make concessions on its nuclear program if the USA met certain demands. Having hit a new all-time high on Friday, France’s Exosens plunged nearly 10% even though the defence company raised its medium-term outlook on Monday. Johnson Matthey also dived 16%, as the chemical company lowered the purchase price for its catalyst technology unit, which it plans to sell to Honeywell. Utilities were the day’s winners among the Stoxx600 sectors, boosted by a nearly 7% rally in Enel.

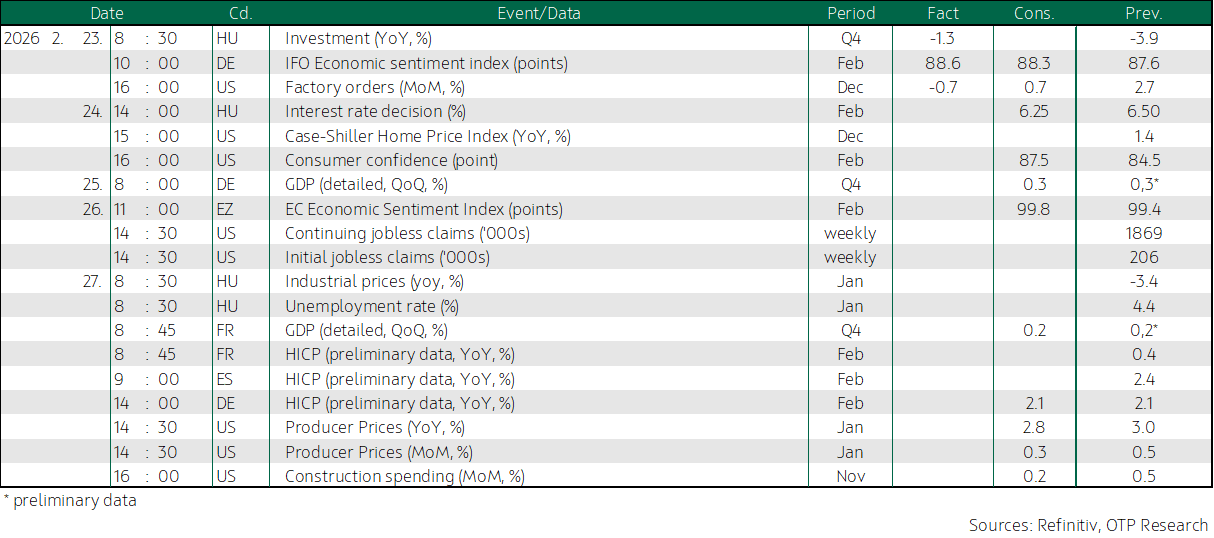

The sentiment in Europe was fragile, even though Germany’s IFO index for February came in slightly stronger than expected and it has improved from the level seen a month earlier. The 88.6 point reading is the highest one since August 2025, and the current conditions and the expectations components improved to the same degree.

On Monday, Hungary’s stock market made up for Friday’s missed rally; the BUX’s 1% gain ranked it in the middle of the CEE league table. Poland’s WIG20 (+1.7%) and Czechia’s PX (+0.3%) upped in Monday's trading. Of Hungary’s blue chips, Richter jumped by nearly 2%, OTP and Mol grew 1.1% each, while MTelekom added 0.8%.

In Hungary, fourth-quarter investment statistics showed a 1.3% year-on-year decline, based on raw data. The seasonally adjusted indicator showed 1.7% contraction year-on-year and a 0.1% uptick on a quarterly basis. Details have not yet been released, but 2025 was the third year in a row when investment shrank; it fell by 4.3% last year.

European natural gas prices edged lower on Monday, trading near 31 EUR/MWh. The USA-Iran conflict appears to be easing for now, despite reports of Iranian military exercises and US military preparations in the region, and traders appear to be pricing in lower risks of immediate supply disruptions. In addition, milder weather in Europe, continued shipments from Norway, and stronger renewable energy production in Germany are strengthening the supply side.

President Trump’s global tariff announcements over the weekend and fears about AI disruption caused sell-off in Wall Street on Monday

America’s markets were also bearish on Monday: the Dow, the S&P500, and Nasdaq Composite all lost more than 1%. Concerns about AI-induced disruptions and the US Supreme Court’s Friday decision on tariffs caused investors to flee, while a bigger-than-expected drop in factory orders for December did not cheer them either. The court’s ruling against tariffs brought back Donald Trump’s erratic statements on trade policy, which have led to significant market volatility in the first year of his second term.

Gold soared: the safe-haven asset gained nearly 3%.

Software companies deleted more than 4% gain, while the S&P500’s financial sector lost more than 3% on fears about AI-induced disruptions. A massive snowstorm blanketed much of the USA, paralyzing travel in the Northeast. Flightaware.com said 89-98% of flights were cancelled at New York airports, Reuters reported. Airlines and travel & leisure stocks descended nearly 4%. The Dow Transports sub-index gave back almost 3%. The healthcare sector, however, strengthened, with Eli Lilly rallying nearly 5% after Novo Nordisk’s fiasco. Domino Pizza’s better-than-expected quarterly revenue numbers were rewarded with a 4% increase in the share price. PayPal jumped nearly 6% on news of a possible acquisition interest. In the risk-averse sentiment, utilities, real estate, raw materials, energy, and the non-cyclical consumer discretionary sectors achieved gains.

As the fourth-quarter earnings season is coming to an end, only 77 of the S&P 500 companies have not shared their reports. Of those that have already reported, 73% have beaten expectations, and analysts estimate the annual earnings growth for the S&P500 as a whole at 13.9%, according to LSEG data; this is well above the 8.9% forecast at the beginning of 2026.

A few giants are also expected to report this week, including Nvidia’s report on Wednesday, and later those of Home Depot, Lowe's, Salesforce and Universal Health Services.

Oil prices eased on Monday as tensions between the USA and Iran eased. President Trump said yesterday that he would prefer a deal with Iran in the talks that resume on Thursday, but warned Tehran that it would be very bad off if a nuclear deal was not reached. Gold was up just 1.1% at the close on Monday, while silver grew by 3%.

Uncertainty over the tariff war and concerns about AI’s disruptive impact on markets led investors towards risk-free assets; long yields sank, and the EUR/USD ended below 1.18; the EUR/HUF closed at 379

Uncertainty over US tariff policy and stock market fears over artificial intelligence drove investors towards bonds, thus US and German bond yields dropped by 3-5 basis points. The ten-year US yield sank below 4.05%, and the German one declined to 2.7%. Although the dollar weakened in the morning and the EUR/USD rose to around 1.185, the cross eventually returned below the 1.18 mark.

The forint held up well yesterday and, after a brief weakening, the EUR/HUF returned to 379. Hungary’s benchmark bond yields inched up 1-2 basis points, but the 10Y yield remained below 6.5%. At the ÁKK’s switch auction, Treasury Bills worth HUF 35 billion changed hands, amid strong demand.

Today’s highlights

The sentiment on Japan’s and China’s reopened stock markets was positive in today's trading, and so was on Korea’s and Taiwan’s stock exchanges, while the benchmarks of Hong Kong and India were in the red ahead of today's close. Japan’s Nikkei and China’s Shanghai Composite rose by 0.9% each, China’s CSI300 blue chip index was seen 1% higher. Taiwan’s benchmarks are up around 3%. In Japan, companies related to artificial intelligence were top performers, while the uncertainty about US tariffs cast a shadow on India’s markets.

Most index futures boded well for Europe and the USA.

In Hungary, the MNB’s Monetary Council holds its February rate-setting meeting today, where the 6.5% base rate may be reduced by 25 basis points, ending an almost 18-month pause.

The ÁKK auctions 3M discount T-Bills, offering HUF 30 billion.

On the international stage, the US consumer confidence index and housing market price statistics are in focus today. Wholesale inventory statistics and the Richmond Fed manufacturing index will also be published. France releases business confidence index.

Home Depot, food company Keurig Dr Pepper, among others, will report today. In Europe, earnings reports from Standard Chartered, Endesa, Telefónica and Telekom Italia may be in the spotlight.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more