OTP Morning Brief: Tension is growing in the Strait of Hormuz

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

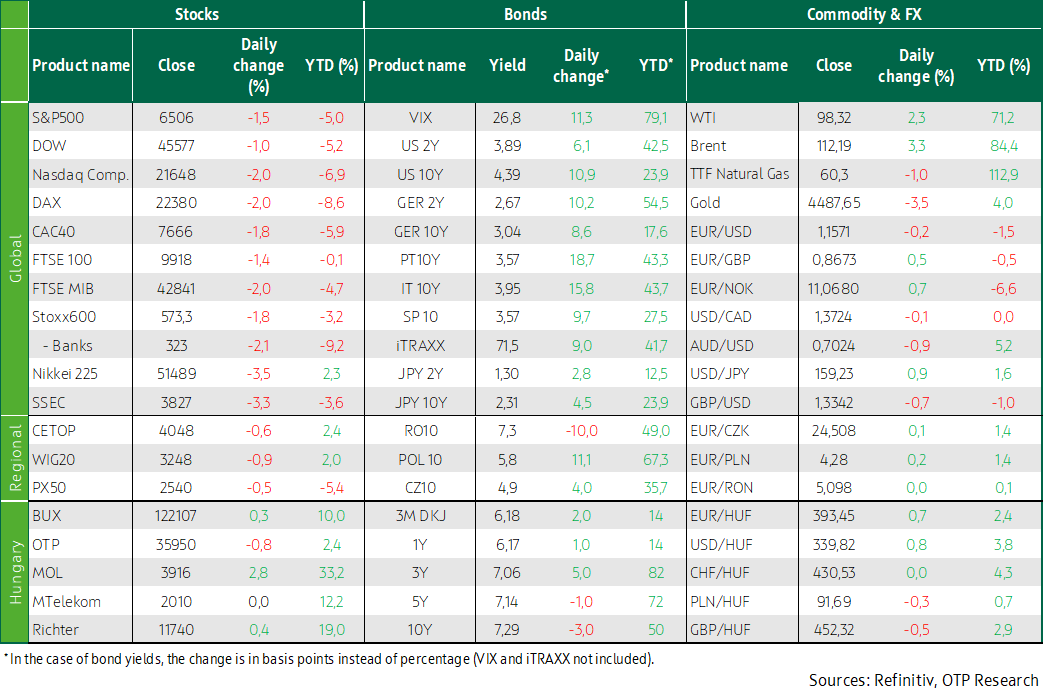

The Middle East conflict continues to rule market developments. Uncertainty over the control of the Strait of Hormuz is fuelling energy prices’ growth. WTI crude shot up almost 50%, nearing USD 100, and Brent jumped by 55%, beyond USD 112 in the past three weeks. The markets expect higher interest rate from the ECB and flat interest rate from the Fed this year. The USA’s and Europe’s key indices closed in the red on Friday and suffered hefty losses last week. On Friday, the BUX’s uptick was the best performance in the CEE region, where only Poland’s WIG20 declined week/week. Soaring energy prices are raising inflation risks, and the yield curve has shifted upwards in developed and developing countries alike. The dollar weakened slightly, while the forint has practically stagnated against the euro last week. The euro area’s March consumer confidence index is due today. Later this week, PMIs will be published in Europe and America, and Hungary’s MNB makes rate decision.

Tensions escalate in the Middle East; crude oil prices rose further

The Middle East conflict continues to rule market developments as the fight that started on 28 February is expanding geographically and the anxiety around the Strait of Hormuz is heating up. Donald Trump gave Iran a 48-hour ultimatum on Saturday evening (Sunday morning, CET) to open the strait, otherwise he threatened to obliterate Iranian power plants. In response, Iran said that if the enemy attacks its fuel and energy infrastructure, it will target all energy infrastructure, IT, as well as water purification and desalination facilities in the region. Earlier last week, President Trump called on his NATO allies to help protect tankers passing through the strait from Iranian attacks as Iran has attacked energy production facilities in the Persian Gulf. Iraq declared force majeure on Friday for all oil fields operated by foreign companies, citing the attacks. Reportedly, the Pentagon may send thousands more Marines to the Middle East, which points in the direction of ground strikes. WTI crude oil prices have jumped by almost 50%, to around 100 USD/barrel, while Brent has skyrocketed 55%, going beyond USD 112 in the past three weeks. In Europe’s natural gas market, TTF prices have reached 60 EUR/MWh, in an increase of more than 85% in three weeks. Meanwhile, the US domestic natural gas price (Henry Hub) has risen by around 8% from a low during this time. The soaring oil prices have revived inflation and growth concerns and have erased expectations of interest rate cuts – instead, expectations of interest rate hikes are building up.

Europe’s stock markets decline for the third consecutive week

Europe’s stock markets have slipped for the third week in a row. Oil prices grew in the second half of last week, as the attacks on energy facilities in the Middle East quickly dispelled the calm felt at the beginning of the week. The STOXX 600 slid 1.8% on Friday, bringing its weekly loss to 3.8%. Western Europe’s leading stock markets slumped 1.5%—2.0% on Friday, and their weekly loss was more than 3%. All sectors fell on Friday, in particular defence, utilities, and financial stocks – only the oil & gas sector posted weekly gain.

Last week’s most anticipated event was the ECB’s interest rate decision, where the key lending and deposit rates were left unchanged, as expected. Christine Lagarde’s comments made investors rather wary. The market is currently pricing in three 25-basis-point hikes by the ECB this year, with the first increase likely in June. Elsewhere, the Bank of England also left its key interest rate on hold last week, as expected.

On Friday, Hungary’s BUX (+0.3%) was top gainer in the CEE region, where Poland’s WIG20 and Czechia’s PX turned red. Of Hungarian blue chips, only MOL (+3%) and Richter (+0.4%) posted gains. In weekly comparison, the PX50 (+1%) performed best, the BUX added 0.3%, while the WIG20 eased by 0.8%.

Wall Street’s indices fell deeper; US rate cut expectations for this year have faded away

Wall Street’s indices plunged on Friday as oil prices increased further. The Dow (-1%), the S&P500 (-1.5%) and the NASDAQ (-2%) all slipped; the technology sector saw the worst losses. America’s major indices have been dropping for the fourth consecutive week, losing 2% last week.

Investors have practically priced out any rate cut this year in the USA – they were replaced by rate hike expectations. This comes despite Jerome Powell’s speech at the Fed's rate-setting meeting last week that energy price shocks typically have a temporary impact on inflation, and the dot plot (which summarizes policymakers' expectations) is consistent with a 25-basis-point reduction this year, but there is also significant support for holding interest rates; none of them expects a hike this year.

Developed economies’ bond yields rose further; Hungary’s yield curve has flattened

The events of the Middle East conflict influenced the sentiment in developed economies’ bond markets last week. Soaring energy prices add to inflation risks, and the yield curves in both developed and developing countries have shifted higher. Many central banks of advanced economies – including the Fed, the ECB, the Bank of England, the Swiss National Bank, the Bank of Japan, and the Reserve Bank of Australia – held monetary policy meetings last week, and although they left key interest rates on hold, policymakers raised their inflation forecasts, expressed concern about the already significant inflation risks due to higher energy prices, and committed themselves to achieving inflation targets. All of this ultimately led to a significant increase in developed economies’ bond yields on Friday. In the USA, the market has priced out the previously expected two rate cuts by the end of this year, and the 10Y US yield rose to almost 4.4% on Friday, which is a 13-basis-point yield increase in a single day, 15 bps rise in one week, and a 50-basis-point growth in three weeks. This brings the US 10Y bond yield closer to the middle of its post-covid trading range. In Europe, the money market yield curve is now consistent with three 25-basis-point interest rate hikes (whereas permanent hold was expected a few weeks ago); the first increase may happen as early as in April. The 10Y German yield jumped by nearly 10 basis points on Friday and rose above 3%, to its highest in the past 15 years; the Bund yield appears to be breaking above its post-covid trading range. The dollar weakened slightly from the eight-month peak of 1.14 reached in the previous week, closing in the vicinity of 1.155.

The CEE region’s currencies held up relatively well last week. The EUR/HUF closed at 393 on Friday, essentially flat week-on-week; neither did the zloty or the koruna weaken meaningfully. However, interest rate hike expectations stuck at elevated levels: the market expects three 25-basis-point interest rate hikes by the end of 2026 from all three regional central banks – as well as from the ECB. Hungary’s bond yields mostly declined on Friday; the curve flattened slightly over the past week: the 3Y yield rose, while yields at the long end of the curve shed about 10 basis points; the 10Y yield was at 7.3%.

Today’s highlights

The weekend’s threats from both sides over the Strait of Hormuz have further deepened investors’ concerns, so the major stock exchanges of the Asia-Pacific region are expected to close this morning's trading with painful losses. Index futures suggested that Europe and America would open in the red today.

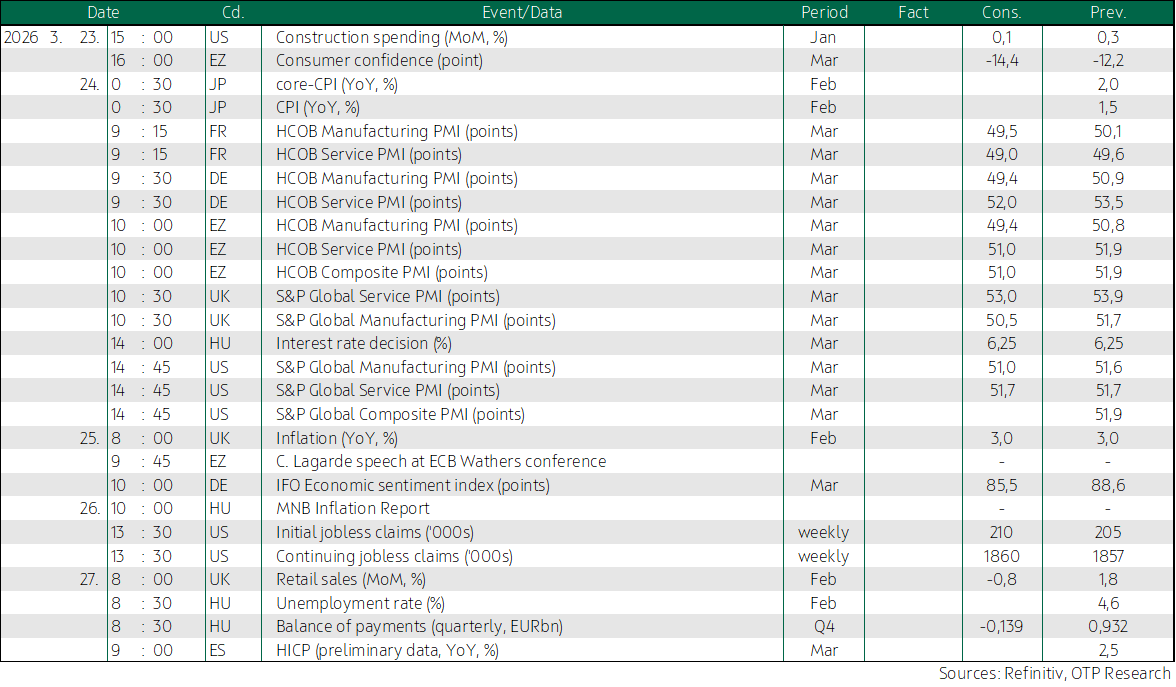

The March reading of the eurozone’s consumer confidence index is due today; it is expected to fall deeper.

Later in the week, purchasing managers’ indices (PMIs) will be published in Europe and in the USA. In Hungary, the MNB’s rate-setting meeting may move markets on Tuesday.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more