OTP Morning Brief: The Bank of Japan raised its interest rate to 0.75%, the highest level in 30 years.

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

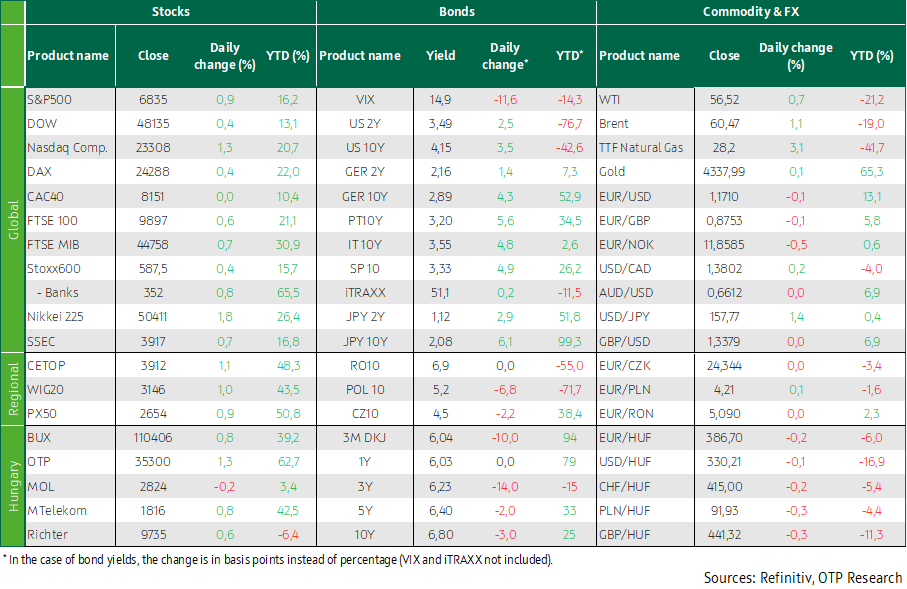

The 10-year Japanese government bond yield climbed above 2%, marking a 26-year high. European and U.S. stock market indicies rose further. OTP’s share price hit a historic high, exceeding 35,000 forints. The forint strengthened slightly after weakening earlier in the week. Domestic bond market yields continued to decline on Friday. Wage growth in Hungary remains slightly below 10%.

European stock markets rose, OTP shares hit an all-time high

European equities continued to climb, with most Western European indices gaining around 0.5%, except for the flat French market. For the week, Germany’s DAX rose 0.4%, France’s CAC 40 added 1%, STOXX 600 advanced 1.6%, and the UK’s FTSE 100 surged more than 2.5%, supported by the Bank of England’s rate cut. Friday’s rally was again led by defense and banking stocks, while consumer goods lagged—particularly sportswear makers, as Adidas fell 1.2% and Puma dropped 3% after Nike reported disappointing sales in China.

Two minor macro updates hit Europe on Friday: German consumer confidence unexpectedly fell to a two-year low, while the ECB’s wage indicator pointed to slower-than-expected moderation, projecting wage growth near 3%.

In Central Europe, regional markets gained close to 1% on Friday, with Hungary’s BUX up 0.8%. Weekly performance was mixed: BUX rose less than 1%, Poland’s WIG climbed over 2%, and Prague’s PX gained 3%. The main drag was MOL, down 0.2% Friday and 4% for the week, while OTP soared 1.3% on Friday to a new all-time high of HUF 35,300, driven by a massive end-of-session transaction worth HUF 27 billion.

The U.S. equity rally continued

After early-week declines, American indices rose on Thursday and Friday, driven mainly by the technology sector. The Dow Jones gained just 0.4%, the S&P 500 advanced 0.9%, and the Nasdaq Composite climbed 1.3%. Among tech leaders, Oracle jumped 6.6%, Nvidia rose 4%, and Alphabet added 1.5%. Despite the late-week rebound, U.S. markets underperformed Europe: the Dow ended the week down 0.7%, the S&P was flat, and even the best-performing Nasdaq posted less than a 1% gain.

On the macro side, the University of Michigan consumer sentiment index improved, though less than expected, while inflation expectations eased.

Gold price rose 0.3%, while silver jumped 2.5%, reaching a new all-time high above $67.

Both Japan’s key policy rate and the 10-year government bond yield hit multi-decade highs

After the ECB kept its key rate unchanged at 2% on Thursday, as expected, the Bank of Japan raised its policy rate by 25 basis points to 0.75%—a 30-year high—following November inflation data showing around 3% growth. The 10-year Japanese government bond yield also climbed above 2%, a 26-year high, after the BoJ signaled it would not intervene in market dynamics. This pushed European and U.S. yields higher on Friday: German, Italian, and French 10-year yields rose about 5 basis points, leaving weekly changes roughly the same and keeping European yields near the top of their post-pandemic trading range, as markets expect the ECB to hike rates in late 2026 or early 2027. In the U.S., the 10-year Treasury yield edged up 2 basis points Friday to around 4.15%, but posted a slight weekly decline amid rising unemployment and unexpectedly low November inflation, reinforcing expectations for at least two 25-basis-point Fed rate cuts in 2026.

The dollar strengthened against the euro on Friday and over the week, recovering from the prior week’s sharp drop, though EUR/USD remained above 1.17.

In Hungary, October data from the statistical office showed gross average wages up 8.7% year-on-year, keeping wage growth in the high single digits. The EURHUF rebounded Thursday and Friday to 386.5 from a midweek highs around the 390 levels. Early-week weakness was driven by two factors: the central bank cautiously opened the door to rate cuts at its December meeting—already priced in for Q1—and PM Viktor Orbán expressed concern about potential freezing of Hungary’s FX reserves. Markets now expect three 25-basis-point rate cuts in 2026, up from two previously priced. Domestic bond yields fell: discount treasury bills and bonds dropped 2–4 basis points Friday and 10–20 basis points for the week, with the 10-year yield dropping to 6.8% by Friday.

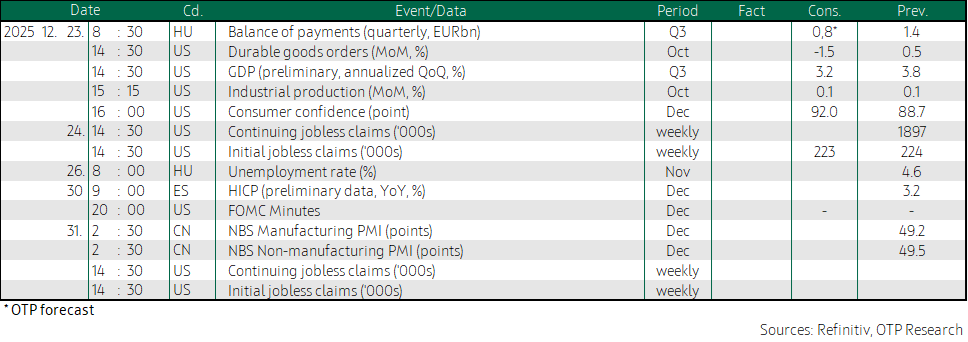

Today’s highlights

With Monday’s rate decision, China has now kept its benchmark loan prime rates (LPR) unchanged for the seventh consecutive month, in line with market expectations. The one-year LPR remains at 3%, while the five-year LPR stays at 3.5%.

As markets near the close, Asian indices are trading strongly in positive territory. The Nikkei and KOSPI are up by 1.7–1.8%, while the Hang Seng has gained 0.2% and the SSEC is up 0.8%.

Before Christmas, key macro data will still arrive on Tuesday. Alongside the U.S. third-quarter GDP, Hungary’s Q3 current account balance will also be released on December 23.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more