OTP Morning Brief: Skepticism surrounding the technology sector weighed on markets on Thursday

Related content

OTP Morning Brief: Rising oil prices and US labor market data pushed developed market bond yields higher

Supported by favorable corporate earnings reports, leading Western European stock indices mostly posted modest gains on Thursday. In contrast, US equity markets closed lower. Eurozone retail sales fell by 0.3% month-on-month in June, while the May figure was revised upward. German industrial orders increased by more than expected. The data released on Thursday continue to support the resilience of the US labor market. Developed market bond yields rose alongside higher oil prices. The forint weakened by 1% against the euro, underperforming its regional peers. Following stronger readings in May, Hungarian retail sales and industrial production declined month-on-month in June. Today, the primary focus will be on July CPI data released by the HCSO and US labor market figures.

OTP Morning Brief: Strong corporate earnings buoyed the Stoxx600 and the Dow to new all-time highs, technology sector came under pressure

Key European equity indices edged higher on Wednesday supported by strong corporate earnings, with the Stoxx 600 and the DAX closing at record highs. In the US, however, the technology sector came under pressure, as shares fell sharply despite better-than-expected quarterly results from SpaceX and AMD, amid concerns surrounding AI-related investment spending. As a result, the S&P 500 and the Nasdaq declined, although the Dow closed at record high. The decline in oil prices came to a halt, while long-term yields in developed bond markets dropped further. Interest rate hike expectations eased in the US and the euro area as well. In the FX market, EUR/USD rose to 1.155, while the EUR/HUF closed below 362. Hungarian long-term bond yields declined. In Germany, factory orders data will be released, while euro area retail sales figures will also be today’s highlights. In Hungary, preliminary June industrial production figures and retail sales data are in the focus. In the US, weekly jobless claims data and Q2 productivity figures could also attract attention. In Europe, earnings reports from Siemens, Rheinmetall and Deutsche Telekom will be in investors’ focus, while in the US, results from Cloudflare and Datadog may be worth watching.

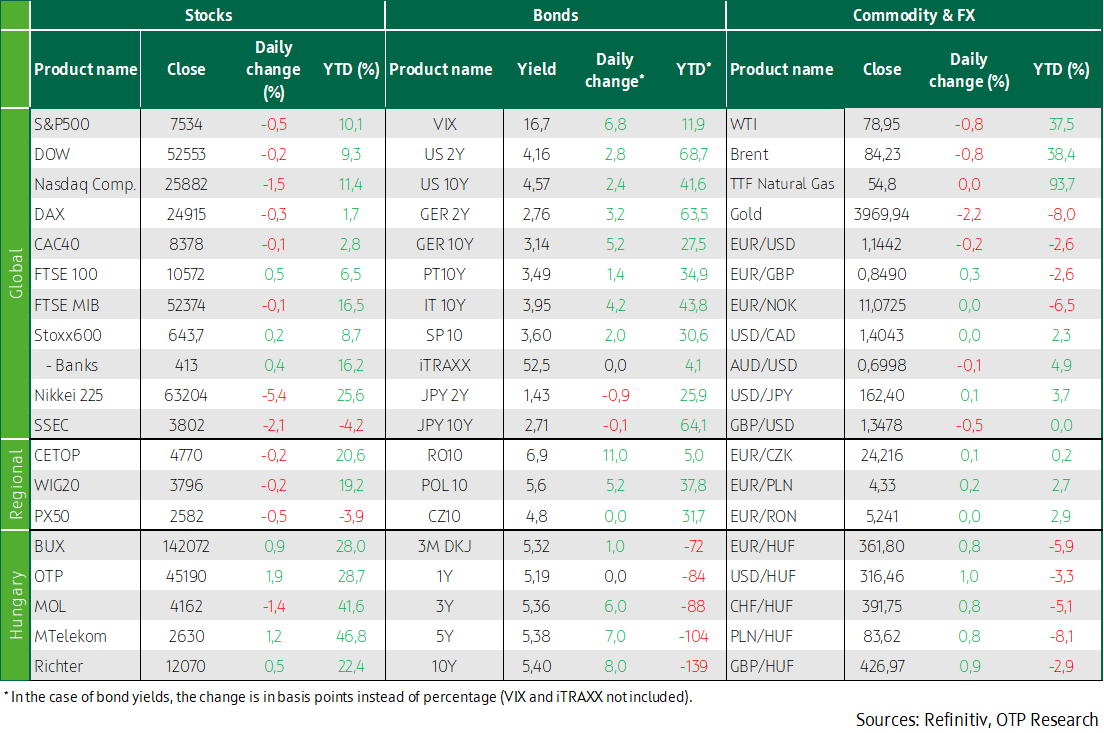

European markets delivered a mixed performance on Thursday, supported primarily by the telecommunications sector, while the BUX advanced. Russian and Ukrainian strikes drove up global wheat prices. Net wages in Hungary rose by 11%. Major US indices declined, led by the technology sector. Retail sales met expectations, while weekly labor market data indicated continued stability. The spread between US and German bond yields narrowed, while the forint weakened to a two-month low. Asian markets were also hit by weakness in the technology sector. Today, the focus will be on economic data releases from the US.

European markets delivered a mixed performance on Thursday, while earnings in Hungary rose by 11% in May

European equity markets moved in mixed directions on Thursday as investors focused on corporate earnings reports. Sentiment was weakened by a renewed escalation of geopolitical tensions in the Middle East, which rekindled concerns over CPI through the potential disruption of energy supplies. The pan-European STOXX 600 index gained 0.2%, supported primarily by the UK’s FTSE 100, which advanced 0.5%, while the DAX declined 0.3% and the CAC 40 slipped 0.1%. Among sectors, media and household goods outperformed, both rising 1.4%, whereas basic materials and telecommunications were the weakest performers, posting declines of a similar magnitude. Technology stocks came under pressure globally and, although ASML gained 3.2%, STMicroelectronics fell 4.9% and BE Semiconductor dropped 3.2%. One of the day's biggest losers was Norway’s Telenor, whose shares plunged 13.4% after the telecommunications company lowered its 2026 guidance following weaker-than-expected Q2 results. Russia and Ukraine intensified hostilities in the Black Sea and the Sea of Azov with missile and drone attacks, targeting ships, port infrastructure and logistics facilities on both sides, driving global wheat prices to a multi-year high.

Sentiment across the CEE region was similarly mixed. While the PX declined 0.5% and the WIG slipped 0.2%, the BUX closed the session 0.9% higher. The region’s outperformance was supported by a 1.9% gain in OTP shares, while all domestic blue-chip stocks advanced except for MOL. In May 2026, Hungary’s average gross monthly earnings stood at HUF 764,100, while average net earnings reached HUF 535,900. Average gross wages rose 8.7% year-on-year, net wages increased 11.0%, and real wages were 9.0% higher than a year earlier.

Technology stocks weighed on US markets, retail sales met expectations, and uncertainty in the Middle East persisted

Weakness among semiconductor stocks weighed on US equity markets on Thursday, continuing to play a key role in broader market movements despite generally favorable US economic data and a strong start to the Q2 earnings season. The Dow fell 0.2%, the S&P 500 declined 0.5%, and the Nasdaq dropped 1.5%. As a result, technology was the worst-performing sector among the S&P 500’s eleven major sectors, falling 1.8%, largely driven by a 4.3% sell-off in semiconductor shares. Memory chip manufacturers were among the biggest losers, with shares of SanDisk, Western Digital, Seagate Technology, and Intel declining between 5.8% and 12.6%. Losses in the Dow were partially offset by a 1.2% gain in UnitedHealth Group after the company reported better-than-expected results and raised its 2026 guidance, helping healthcare stocks advance 2.2% overall. In contrast, United Airlines fell 1.8% as sharply higher oil prices clouded the company’s outlook, while GE Aerospace shares dropped 4.1% despite the firm also raising its 2026 profit forecast.

Beyond corporate earnings, investors also monitored several economic releases during the session. Retail sales rose 0.2% in June, following an upwardly revised 1.0% increase in May, in line with analysts’ expectations. The modest growth in June retail sales was primarily attributable to lower fuel prices, which reduced revenues at gasoline stations. According to data from the US Energy Information Administration (EIA), the average gasoline price declined to USD 4.18 per gallon in June from USD 4.61 in May. Separately, data released on Thursday showed that initial jobless claims fell by 8,000 to 208,000 in the week ending July 11, coming in below the consensus forecast of 217,000. The current level is consistent with what economists describe as a “low-hiring, low-firing” labor market environment. At the same time, pending home sales declined more than expected, while homebuilder sentiment deteriorated further as elevated borrowing costs and worsening affordability continued to weigh on the housing market.

Brent crude futures fluctuated around the USD 85 per barrel level on Thursday, remaining near a one-month high as escalating tensions in the Middle East continued to support prices and weigh on investor sentiment. According to reports, the Iranian government instructed Houthi rebels to prepare for a potential closure of Red Sea oil shipping routes should US forces follow through on President Donald Trump’s threat next week and strike Iranian infrastructure targets in the absence of a diplomatic breakthrough. Meanwhile, the US stepped up its operations against Iran and, according to reports, targeted an oil tanker near the country’s main export terminal for the first time since reimposing a blockade on Iranian ports. In response, Iran launched attacks against US military bases in Kuwait and Jordan.

The spread between US and German bond yields narrowed, while the forint weakened to a two-month low

US Treasury yields posted modest gains on Thursday after fresh data on consumer finances and labor market conditions largely failed to alter investors’ expectations regarding the Federal Reserve’s policy path. The benchmark 10-year US Treasury yield edged higher, although it had declined by a cumulative 6.5 basis points over the previous two sessions, marking its steepest two-day drop in three weeks. In Europe, the yield on the 10-year German Bund rose 3 basis points to 3.135%, reaching its highest level since May 20. As a result, the spread between German and US 10-year government bond yields remained close to a one-month low, as escalating tensions in the Gulf region pushed euro area yields higher this week, while softer CPI data in the US helped limit the increase in Treasury yields. Meanwhile, the dollar maintained its strength against major currencies.

In Hungary, longer-dated government bond yields moved higher, with the three-year yield rising 6 basis points to 5.36%, followed by increases of 7 basis points in the five-year yield, 8 basis points in the 10-year yield, and 9 basis points in the 20-year yield. Meanwhile, the forint extended its losses, weakening to EUR/HUF 362, its lowest level in two months.

Demand was robust at yesterday’s Treasury bill auction held by Hungary’s Government Debt Management Agency (ÁKK). Bids totaling HUF 59 billion were submitted for the HUF 30 billion on offer, of which the debt manager accepted HUF 30 billion at an average yield of 5.21%. Despite the strong investor interest, ÁKK accepted less than the announced amount at its government bond auction.

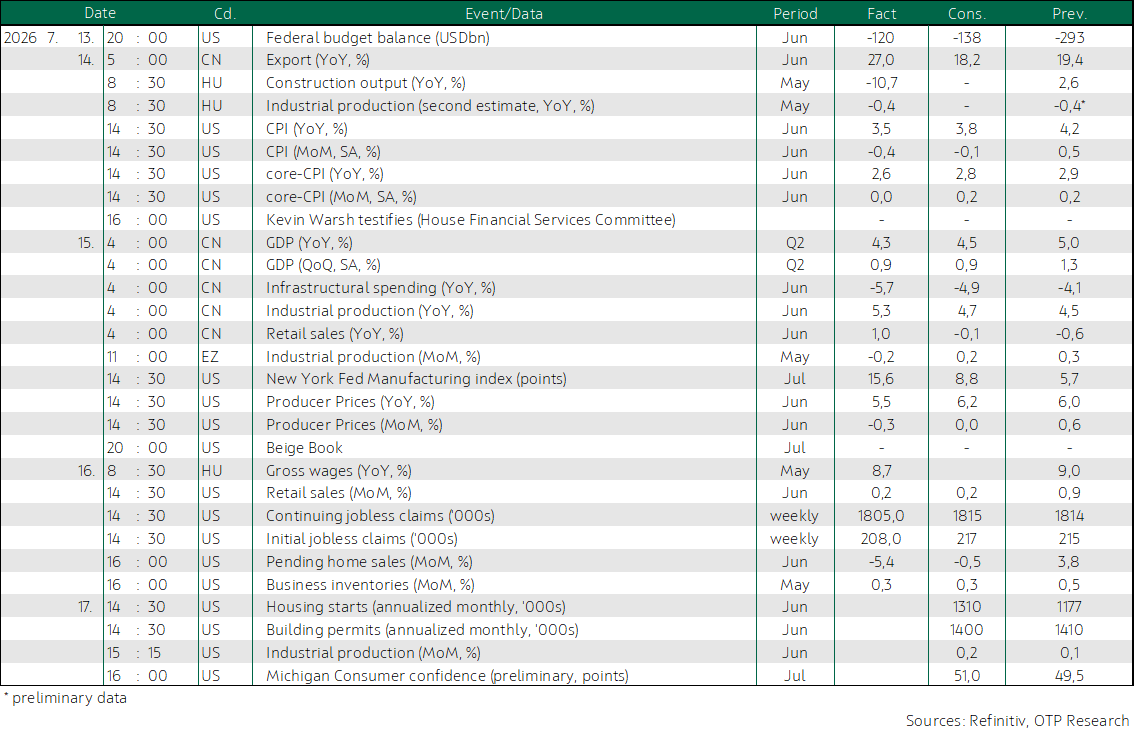

Today's highlights

Skepticism surrounding the technology sector hit Asian markets particularly hard, with Japan’s Nikkei plunging more than 5%, Taiwan’s benchmark index falling 5.7%, and China’s Shanghai Composite (SSEC) declining 2.1%, while South Korean markets remained closed due to a national holiday.

Today's focus will primarily be on US economic data releases, including June industrial production, housing starts and building permits, as well as the University of Michigan's consumer sentiment index for July.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more