OTP Morning Brief: Weaker-than-expected US jobs report moved the markets on Thursday

Related content

OTP Morning Brief: Airstrikes eased in the Middle East

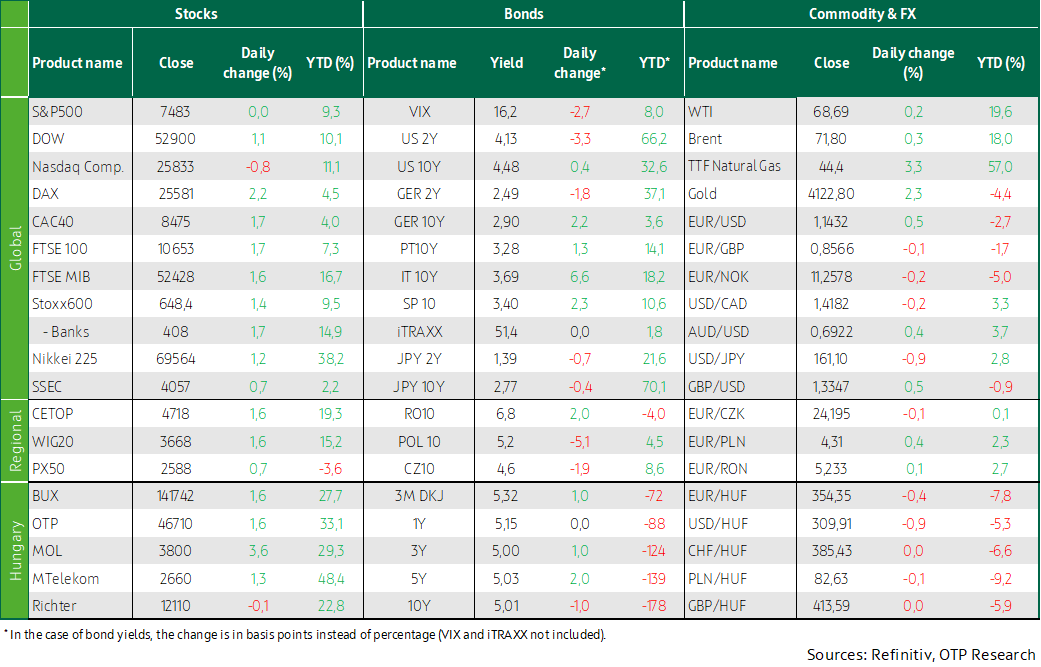

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

OTP Morning Brief: Oil prices climbed back above $100, while tech sector earnings reports drove market movements

Global equity indices moved lower after earnings reports from leading technology companies revealed a significant rise in artificial intelligence-related investment costs. At the same time, developments in the Middle East pushed Brent crude prices above $100 per barrel, once again bringing CPI trends into investors' focus. Driven by macroeconomic data and the rise in oil prices, US and European government bond yields increased, while the ECB left its key interest rates unchanged, in line with expectations. The Trump administration will replace the expiring 10% global tariff with a new set of tariffs.

Nonfarm payrolls in the US grew less than expected in June, and the previous month’s figures were also revised downward, easing interest rate hike expectations in the US. Leading European indices closed higher yesterday; the Stoxx 600 hit a new high. Thursday’s trading on Wall Street ended mixed, with the technology sector underperforming. Stock markets in the CEE region closed higher. German and U.S. 10-year yields rose slightly, while the euro strengthened against the dollar. There was strong demand at yesterday’s ÁKK auction. The forint strengthened against the euro, falling back below the 355 level. May's industrial production statistics are due out from France. U.S. markets are closed today for a holiday.

Stoxx 600 Closes at a Record High; Technology Sector Falls; BUX Rises

European equity markets closed higher on Thursday. After Wednesday’s decline, the pan-European Stoxx 600 rose by 1.4% yesterday, reaching a new record high as strong performances in the healthcare, consumer, and defense sectors offset weakness in artificial intelligence-related technology stocks. Investors welcomed weaker-than-expected US labor market data, which eased expectations of further interest rate hikes by the Federal Reserve.

Among individual stocks, Bayer was one of the day’s top performers, soaring nearly 9% after the company announced that it would consolidate its US Roundup business into a newly established unit called Ruveon, following a key legal victory in a case related to the alleged side effects of one of its products. AI-linked technology stocks, including Soitec and Aixtron, declined as investors became increasingly cautious after the sector’s rapid surge in recent months.

Stock markets across the CEE region also moved higher, with the BUX rising 1.6%. Among Hungary’s blue-chip stocks, all closed in positive territory except Richter.

Wall Street Indices Close Mixed; Weaker-Than-Expected Labor Market Data Released

US equity markets closed mixed on Thursday, with the technology-heavy Nasdaq falling 0.8%, the S&P 500 ending virtually unchanged, and the Dow rising 1.1%, marking its fourth consecutive week of gains. The broad weakness in the technology sector reflected profit-taking by investors following the strong share price appreciation seen this year. The US semiconductor sector’s leading and most widely followed benchmark declined for a second consecutive day, falling 5.4% yesterday. Tesla dropped 7.5% after its recent gains despite reporting better-than-expected Q2 delivery figures. According to the Financial Times, OpenAI is considering offering a 5% stake to the US government in an effort to ease mounting political pressure on AI companies.

The most important data release of the day was the June US labor market report. Nonfarm payrolls increased by a smaller-than-expected 57,000, while data for previous months were revised downward by a combined 74,000. Employment growth was driven almost entirely by the healthcare and social assistance sectors, while job creation in cyclical industries came to a virtual standstill. Although the unemployment rate declined to 4.2%, this was primarily due to a significant increase in the number of people leaving the labor force rather than stronger employment growth. Annual wage growth stood at 3.5%, remaining relatively robust. However, the decline in employment within the leisure and hospitality sector was unusual for the summer holiday season, particularly during the FIFA World Cup, suggesting a strong likelihood of positive revisions to the sector’s data in the coming months. Meanwhile, weekly jobless claims data released yesterday showed that both continuing claims and initial claims were broadly unchanged. Taken together, the latest figures suggest that the labor market has stabilized in recent months.

Oil prices edged lower yesterday after Qatar indicated that progress had been made in the US-Iran negotiations aimed at resolving the conflict in the Middle East. However, prices were virtually unchanged over the course of the day, as investors remained cautious about positive developments regarding a potential end to the conflict.

Rate Hike Expectations Ease Across Developed Markets; Forint Strengthens Against the Euro; Strong Demand at Yesterday’s ÁKK Auction

Developed bond markets were primarily driven by the weaker-than-expected July US labor market report. Expectations for a Fed rate hike in September eased somewhat, although market pricing still implies at least one 25-basis-point increase this year. This followed Wednesday’s easing in rate hike expectations in the euro area after June CPI accelerated by less than expected, although markets continue to anticipate at least one additional 25-basis-point hike from the ECB this year. Speaking in Sintra on Wednesday, Christine Lagarde noted that inflation and growth risks had become more balanced compared with a few weeks ago, while Kevin Warsh once again emphasized his commitment to the 2% CPI target. Yesterday, both US and German 10-year government bond yields edged higher following Wednesday’s more pronounced move, ending at 4.48% and 2.9%, respectively, while the front end of the yield curve shifted lower. Against the backdrop of easing US rate hike expectations, the euro strengthened against the dollar, with EUR/USD rising to 1.143.

On the Hungarian government bond market, Thursday’s trading resulted in only modest movements of 1–2 basis points. According to the ÁKK’s early afternoon benchmark quotations, the 10-year yield stood at 5.01%. Regional currencies strengthened against the euro, with EUR/HUF slipping back below the 355 level.

Demand was strong at yesterday’s government bond auctions conducted by the ÁKK, with the 12-month, 10-year, and 15-year maturities all heavily oversubscribed. The debt management agency accepted more bids than originally offered at all auctions except for the longest maturity. The strongest demand was seen at the 10-year government bond auction, where bids exceeding HUF 200 billion were submitted against an announced volume of HUF 25 billion. Of this, the ÁKK accepted HUF 128 billion at an average yield of 5.0%, which was 10 basis points lower than the average yield achieved at the previous auction. At the 12-month discount Treasury bill auction, the ÁKK accepted HUF 48 billion instead of the initially announced HUF 30 billion, while at the 15-year government bond auction it accepted the originally offered HUF 20 billion.

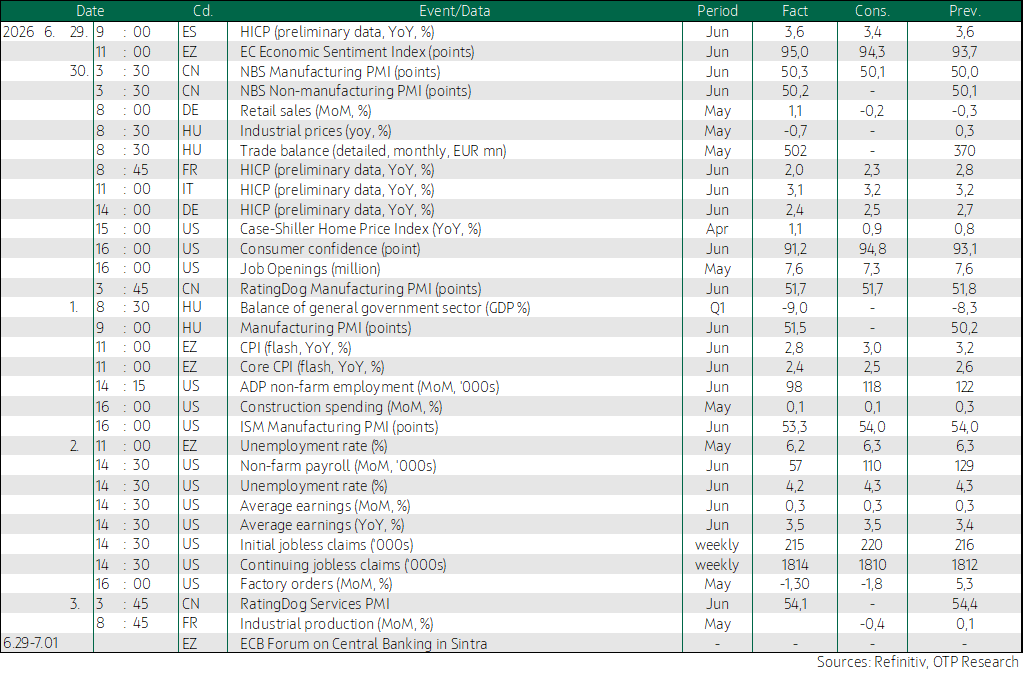

Today's highlights

Asia-Pacific equity markets moved higher this morning, supported by easing US rate hike expectations and purchasing managers’ index data released across the region pointing to improving economic activity. China’s services PMI moderated compared with May but came in above expectations and continued to signal expanding activity. In Japan, the final June readings of both the manufacturing and services PMIs were revised higher than the preliminary estimates, with both indicators remaining above the 50-point threshold that separates expansion from contraction. The Japanese yen has experienced heightened volatility in recent days, weakening to a 40-year low against the US dollar earlier this week, prompting market expectations of another intervention following the authorities’ action at the beginning of the year. Today’s trading began with further dollar strength against the yen, pushing the USD/JPY exchange rate higher.

France will release its May industrial production data today, with consensus expectations pointing to a 0.4% month-on-month decline in output following the modest expansion recorded in the previous month. This would be consistent with the picture painted by purchasing managers’ surveys, which suggest that production accelerated in March after the outbreak of the Middle East conflict as companies sought to build inventories ahead of potential shortages and further price increases. Since then, however, supply chain disruptions and higher costs have begun to weigh on output, leading to some moderation in industrial activity.

US markets are closed today due to a public holiday.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more