OTP Morning Brief: President Trump threatened Iran with further attacks due to the prolonged negotiations

Related content

OTP Morning Brief: Airstrikes eased in the Middle East

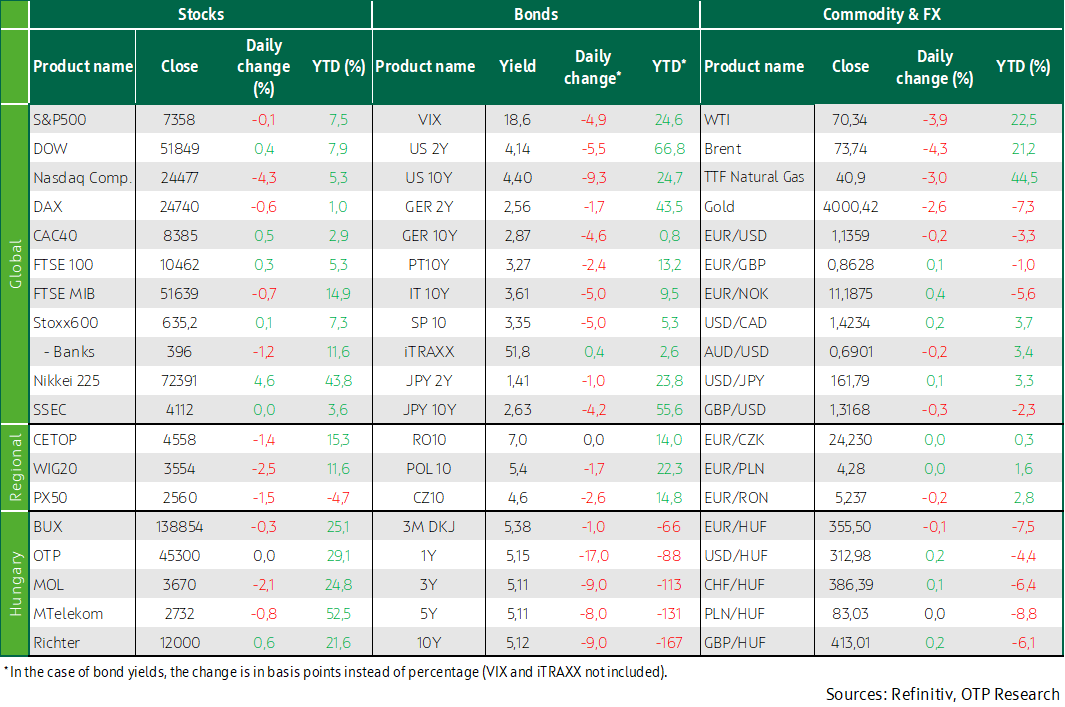

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

OTP Morning Brief: Oil prices climbed back above $100, while tech sector earnings reports drove market movements

Global equity indices moved lower after earnings reports from leading technology companies revealed a significant rise in artificial intelligence-related investment costs. At the same time, developments in the Middle East pushed Brent crude prices above $100 per barrel, once again bringing CPI trends into investors' focus. Driven by macroeconomic data and the rise in oil prices, US and European government bond yields increased, while the ECB left its key interest rates unchanged, in line with expectations. The Trump administration will replace the expiring 10% global tariff with a new set of tariffs.

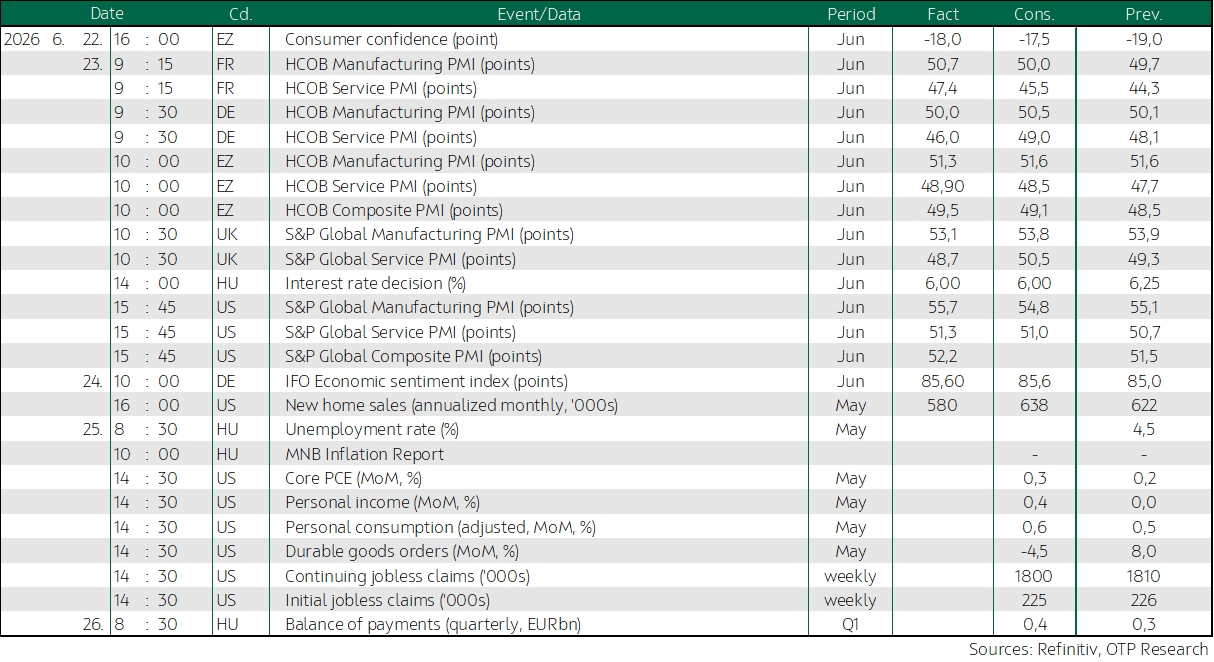

European indices closed mixed yesterday as investors monitored developments related to the war with Iran; Rheinmetall shares fell following a government decision; the IFO sentiment index rose in line with expectations. US indices closed mixed yesterday amid a correction in semiconductor stocks and a drop in oil prices; Alphabet rose; Micron released its earnings report; US new home sales for May came in below expectations. Long-term yields in developed markets declined, while the dollar continued to strengthen against the euro. The most important data release today will be the US core PCE rate; in addition, US household income and consumption figures, durable goods orders, and the usual weekly jobless claims will also be published, while Hungary’s unemployment rate will be released and the MNB will publish its CPI report.

European indices closed mixed yesterday as investors monitored developments related to the war with Iran; Rheinmetall shares fell following a government decision; the IFO sentiment index rose in line with expectations

European equity markets closed mixed on Wednesday as investors assessed developments in US–Iran negotiations, with the STOXX 600 index edging 0.1% higher while Germany’s DAX fell 0.6%; Rheinmetall shares plunged nearly 19% after Germany scrapped plans to build six F126 frigates due to project delays and cost overruns, a decision that hit the company particularly hard as it had been considered a strong contender for the contract, while in contrast Thyssenkrupp’s marine unit surged 16.1% after Berlin opted to procure smaller frigates instead; the technology sector also declined, partly extending the sharper correction seen the previous day, with most semiconductor and chip equipment makers weakening as investors awaited Micron’s earnings release, and according to market commentary the sector’s softness reflects short-term profit-taking similar to earlier corrections this year.

Oil prices fell to multi-month lows as a potential US–Iran peace agreement could ease concerns over supply disruptions, although uncertainty surrounding the details of the deal continued to keep investors cautious.

Germany’s IFO business climate index rose to 85.6 in June in line with analyst expectations, up from 85 in May, signaling a slight improvement in economic sentiment; the uptick was mainly driven by a more positive assessment of current business conditions, while easing geopolitical uncertainty helped stabilize expectations for the outlook, and market participants continue to focus on the central bank rate path, with pricing suggesting that the European Central Bank could still deliver one additional rate hike of around 25 basis points by year-end.

Regional markets declined yesterday: among Hungarian blue chips, Mol and Magyar Telekom shares fell, OTP was broadly unchanged, while only Richter managed to rise.

US indices closed mixed yesterday amid a correction in semiconductor stocks and a drop in oil prices; Alphabet rose; Micron released its earnings report; US new home sales for May came in below expectations

US equity markets closed mixed yesterday, with sentiment primarily shaped by weakness in the technology sector and uncertainty surrounding semiconductor industry prospects; the decline in chip stocks was led by Micron Technology, whose share price fell 5.3% ahead of its earnings release published after the close, while other players in the memory segment also underperformed and broader chipmakers came under pressure, and according to market assessments the pullback in the tech sector can be seen as a correction following a strong rally in the previous period that pushed expectations to elevated levels, increasing the risk of disappointment during the upcoming earnings season, however Micron’s post-close report ultimately exceeded expectations on both revenue and profit thanks to skyrocketing memory prices, sending its shares up more than 10% in after-hours trading.

Meanwhile, Alphabet shares rose after it was announced that the company will soon replace Verizon in the Dow Jones index, potentially generating additional investor demand for the stock; overall, yesterday’s trading was dominated by a correction in the technology sector and declining energy prices, while investors increasingly focused on reassessing corporate earnings outlooks as the reporting season approaches.

US new home sales fell to 580,000 in May from 626,000 in April, marking a notable decline and coming in below market consensus, which had expected a level of around 638,000; the negative surprise suggests that housing demand remains highly sensitive to the elevated interest rate environment, and from a macro perspective the housing market is particularly important as it is one of the fastest-reacting sectors through the interest rate transmission channel.

Long-term yields in developed markets declined, while the dollar continued to strengthen against the euro

US Treasury yields declined yesterday, mainly driven by falling oil prices: Brent dropped to multi-month lows as concerns over supply disruptions eased and an increasing number of tankers left the Strait of Hormuz; the decline in energy prices also weighed on CPI expectations, while the short end saw a more modest move, resulting in a slightly flatter 2–10 year segment of the yield curve, as market pricing currently implies more than a 65% probability of a September rate hike, putting upward pressure on short-term yields, while persistently above-target inflation continues to keep the central bank on a tightening path.

Meanwhile, German long-term yields also declined, the dollar extended its strengthening against the euro since last Wednesday’s Fed rate decision, while the forint remained largely unchanged following Tuesday’s more notable weakening driven by signals related to the MNB’s rate-cutting path.

Today's highlights

Asian indices were mixed this morning, while technology-heavy Japanese and Korean benchmarks surged following Micron’s earnings released yesterday; shares of Alibaba listed in Hong Kong fell by nearly 3% after Anthropic accused the Chinese tech company of attempting to acquire its artificial intelligence capabilities.

Today, on the domestic front, Hungary’s unemployment rate and the MNB’s CPI Report will be published, while tomorrow will see the release of several key US macroeconomic indicators, led by core PCE, the Fed’s preferred gauge and therefore a key driver of rate expectations; additionally, household income and consumption data will provide insight into the current state of domestic demand, durable goods orders will offer feedback on investment activity, and the usual Thursday jobless claims data will give an indication of labor market tightness.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more