OTP Morning Brief: Optimism surrounding a Middle Eastern peace agreement drove equity markets on Thursday

Related content

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

OTP Morning Brief: Oil prices climbed back above $100, while tech sector earnings reports drove market movements

Global equity indices moved lower after earnings reports from leading technology companies revealed a significant rise in artificial intelligence-related investment costs. At the same time, developments in the Middle East pushed Brent crude prices above $100 per barrel, once again bringing CPI trends into investors' focus. Driven by macroeconomic data and the rise in oil prices, US and European government bond yields increased, while the ECB left its key interest rates unchanged, in line with expectations. The Trump administration will replace the expiring 10% global tariff with a new set of tariffs.

While Europe closed mixed in the shadow of monetary tightening, optimism surrounding a Middle Eastern peace agreement lifted Wall Street indices on Thursday, as well as Asian markets this morning. Shipping conditions in the Strait of Hormuz have improved; however, caution is advised as US Vice President JD Vance cancelled his trip to Switzerland today, meaning peace talks will not continue today. The price of crude oil fell close to early March levels, weighing on energy stocks in both Europe and the US, while the travel industry benefitted from the sharp decline in oil markets. Chipmakers rose further, but IT service providers fell sharply following Accenture’s 18% plunge. Bond yields moved mostly sideways, while rate hike expectations strengthened in the US, and the EUR/USD slipped toward 1.145. Regional currencies weakened, with the forint closing above 352 vs the euro. The Nikkei and Kospi reached record highs intraday. US markets are closed today due to a public holiday.

European equities closed mixed on Thursday, while rate hike expectations increased following the Fed’s hawkish communication

Although European equity markets still closed in positive territory on Wednesday, sentiment deteriorated on Thursday as rate hike expectations strengthened following the Fed’s policy meeting the previous evening. US President Trump signed a memorandum of understanding with Iran, suspending the war for 60 days and restoring tanker traffic through the Strait of Hormuz. Crude oil prices fell close to the levels recorded on the first trading day after the outbreak of the US–Israel war against Iran in early March. The Stoxx 600 ultimately slipped by 0.3%, while the FTSE 100 lost 1%, even as the Stoxx 50 reached a new all-time high and both the DAX and CAC 40 rose by 0.4%. Oil and gas companies declined significantly, and pharmaceuticals also came under pressure. News of easing tensions in the Middle East was initially welcomed by investors, driving a notable increase in the travel sector, but enthusiasm later faded amid concerns over potential monetary tightening. A stronger dollar following the signing of the agreement weighed on the materials sector, which delivered the weakest performance among Stoxx 600 sectors yesterday. Industrial stocks rose sharply, with Airbus, Safran, and Schneider gaining about 3%. Infineon surged by 7%, tracking the recent rise in chipmakers globally. In contrast, SAP fell by 4.7% due to weakness in the software sector, while German automakers, as well as UK pharmaceutical and mining companies, also declined. Automakers became the laggards, with Mercedes-Benz, Volkswagen, and Stellantis dropping 3–5%, while BMW, after an 8% decline following Tuesday’s profit warning, lost a further 4% yesterday. IT service providers also had a weak session, with Accenture plunging 18% after unexpectedly lowering its annual revenue forecast. In tandem, Capgemini shed nearly 9%, while CanCom, Atos, and Reply declined by 2–7%. French voucher issuer Edenred jumped 17% on takeover speculation. Banks mostly advanced, with UniCredit and Intesa Sanpaolo rising by 0.7%.

The price of European benchmark TTF continued to fall in line with crude oil, closing the day near EUR 41.

At their policy meetings yesterday, neither the Bank of England nor the Swiss National Bank changed their benchmark interest rates, while the Czech central bank raised rates.

Among regional indices, the BUX declined the least, edging down by just 0.4%, while the PX fell by 1.3% and the WIG20 dropped 1.6%. Among local blue chips, only Magyar Telekom did not weaken.

Wall Street indices rose on optimism surrounding the reopening of the Strait of Hormuz

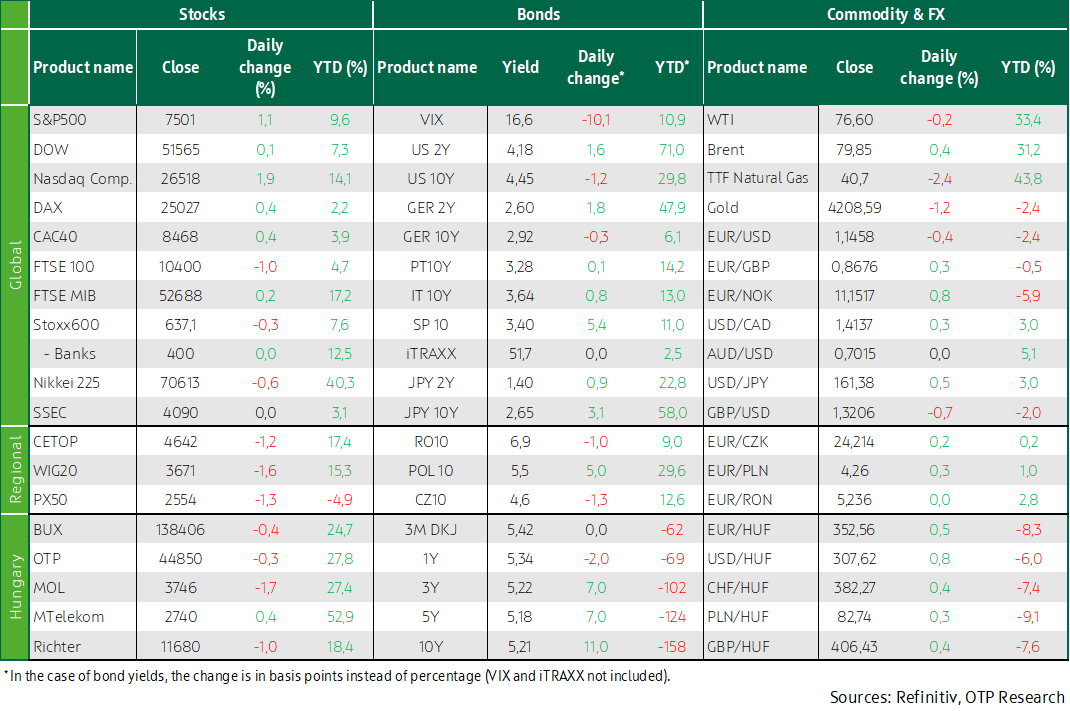

Optimism surrounding the Iranian peace agreement lifted equity indices in the US on Thursday, with the S&P 500 rising 1.1% and the Nasdaq Composite climbing 1.9%, while the Dow edged up 0.1% as inflation concerns eased, even though the market assigns a greater than 50% probability to both a September and a December rate hike. The small-cap Russell 2000 rose 2% to close at a record high.

Among S&P sector indices, IT and consumer discretionary posted the strongest gains, while the Philadelphia Semiconductor Index rallied 6%. Intel soared nearly 11% to a record high after Donald Trump announced that Apple had reached an agreement with Intel to design and manufacture its chips in the US. The consumer sector was driven by travel-related companies, with optimism over lower oil prices supporting gains in shipping firms and airlines.

Software service companies fell to a two-month low: Accenture’s 18% plunge dragged down peers, with Cognizant Technology Solutions dropping 10.5%, Gartner declining 4.6%, and IBM falling 5.0%. Retailer Kroger lost more than 8% after reporting weaker-than-expected quarterly results, although it maintained its full-year outlook. SpaceX declined for a second consecutive day, following an almost 5% drop on Wednesday with a further 3.6% fall, after a strong rally in the days following last Friday’s market debut.

Due to the June 19 public holiday, US stock markets will be closed today; on a weekly basis, the S&P gained 0.9%, the Nasdaq rose 2.4%, and the Dow added 0.7%.

Crude oil prices continued to fall on Thursday, with Brent dropping below USD 80 per barrel and WTI closing at USD 76.6. Following the agreement, traffic through the Strait of Hormuz picked up, with the US Central Command announcing the lifting of restrictions on shipping to and from Iranian ports and coastal waters. Oil tankers previously stranded in the area began leaving the strait on Thursday, while Kuwait announced plans to increase production. As a result, oil prices have almost fully erased the gains recorded since the start of the Middle Eastern conflict in late February.

Developed market bond yields closed near the previous day’s levels, while EUR/USD slipped below 1.146. The stronger dollar weighed on regional currencies, and the domestic 10-year yield edged up to 5.2%

Yesterday in Asia and Europe, bond markets were still driven by the Fed’s hawkish decision on Wednesday evening, with yields edging higher, as the Japanese 10-year rose above 2.6% and the German approached 2.95%, although the latter ultimately closed lower. In the US market, yields corrected following the significant rise the day before, with the 10-year Treasury falling by 5 basis points to near 4.45%. Meanwhile, the dollar continued to strengthen, reaching a more than one-year high against the euro, approaching the 1.145 level.

The stronger dollar once again weighed on regional currencies, with the Czech koruna — despite the expected central bank rate hike — and the zloty weakening by 0.2–0.3%, while the forint declined by nearly 0.5%. Demand was strong at government debt auctions, where one-year Treasury bills, as well as 10-year floating- and fixed-rate bonds, were offered. HUF 60 billion of Treasury bills were sold, against bids exceeding HUF 140 billion and an average yield of 5.4%. HUF 25 billion of floating-rate bonds were issued, with demand twice that amount. For the 10-year fixed-rate bond, bids totaled HUF 200 billion, of which around HUF 70 billion was accepted by the debt manager, at an average yield of 5.18%. Benchmark yields — also reacting to Wednesday evening’s Fed decision — rose by 5–10 basis points from previous lows, with the 10-year once again reaching the 5.2% level.

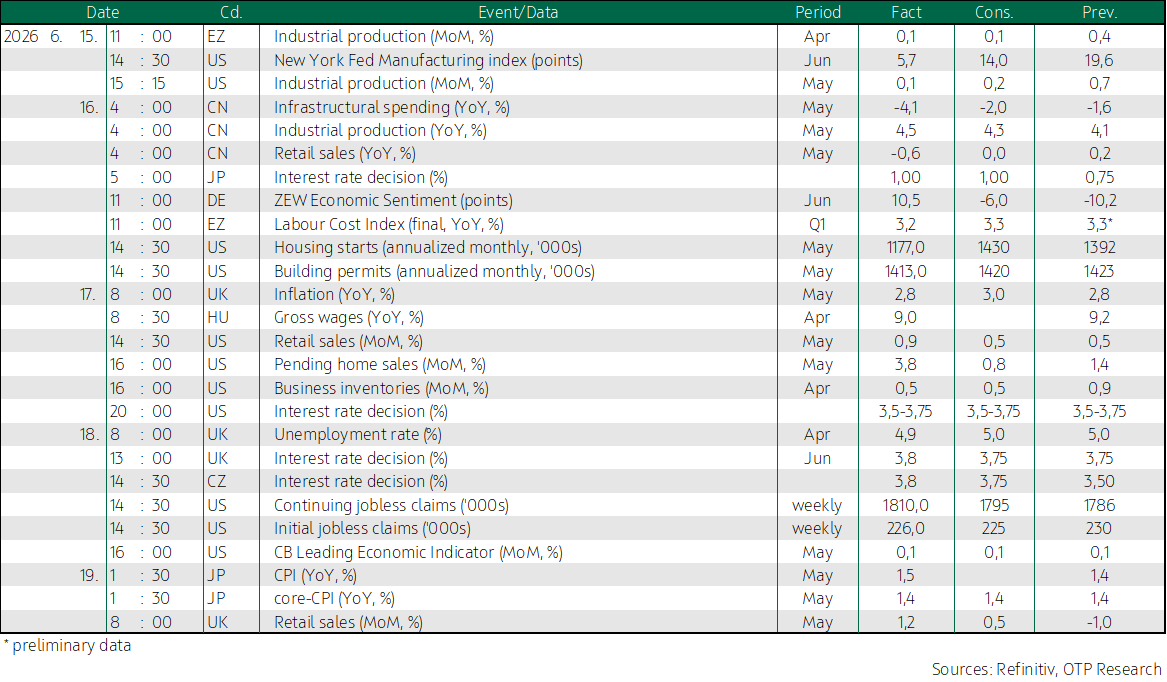

Today's highlights

Hopes surrounding a Middle Eastern peace agreement pushed equity indices to record highs in Japan and South Korea, with the Nikkei rising 0.8% to mark a fifth consecutive record day and a weekly gain above 8%, while South Korea’s Kospi climbed as much as 3%, bringing its weekly advance to 15%. Markets in China, Hong Kong, and Taiwan were closed on Friday due to a public holiday.

US Vice President JD Vance cancelled his planned trip to Switzerland on Friday, where discussions were to be held on the details of the peace agreement. According to a statement from the Swiss foreign ministry, the talks between the US and Iran scheduled for Friday at the Bürgenstock mountain resort in Switzerland will not take place.

Equity futures point to a mostly negative open in Europe, while US markets will be closed today due to the June 19 public holiday.

In Japan, headline inflation measures released today showed an acceleration in May, while core CPI remained unchanged at 1.4% in line with expectations.

Retail sales data will be released today in the United Kingdom, while Germany will publish its producer price index.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more