OTP Morning Brief: Fed held its interest rates unchanged, while markets declined on the back of a more hawkish-than-expected tone

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

European markets still managed to rise on Wednesday, as investors waited ahead of the Fed’s rate decision. Although the Fed ultimately left rates unchanged, policymakers signaled a possible rate cut by year-end, which triggered a broad and significant decline across US markets. Bond yields rose, the dollar strengthened, and regional currencies weakened, with the forint also moving back above the 350 level against the euro. Asian markets rose, with Japan ready to step in to support the weakening yen. Today, attention will focus on the interest rate decisions in the UK and the Czech Republic.

European markets rose on Wednesday, while wages in Hungary increased by 11.2%

European equities edged higher on Wednesday, as investors awaited details of a peace agreement between the US and Iran, as well as the Federal Reserve’s monetary policy outlook, with the pan-European STOXX 600 index closing 0.5% higher and marking its fifth consecutive day of gains, while the DAX and FTSE 100 posted more modest increases and the CAC 40 underperformed with a 0.1% decline, as auto stocks led the losses with a 3.3% drop, their steepest one-day fall in nearly a month, with BMW sliding 8.3% after lowering its annual profit outlook due to weakness in the Chinese market and the impact of the US–Iran conflict, whereas bank stocks provided support with a 1.9% rise driven by Commerzbank (+5.2%), Deutsche Bank (+2.5%) and Barclays (+3.4%), while technology shares advanced 1.5% as Aixtron jumped 6.7% and both BE Semiconductor and ASML gained around 4%, and defense sector stocks added 0.5%, meanwhile on the macro front UK CPI remained unchanged at 2.8% in May, holding at April’s 13-month low and coming in below both economists’ expectations and the Bank of England’s forecast according to official data released on Wednesday, one day ahead of the central bank’s next rate decision.

Most markets in the region also rose, with the BUX adding 0.1% and the PX gaining 0.2%, while the WIG 20 declined by 0.2%, with OTP standing out among Hungarian blue chips with a 1.4% increase, whereas Mol fell by 2.0%, meanwhile in April 2026 gross average earnings in Hungary reached HUF 772,200, representing a 9.0% rise year-on-year, while net wages grew by 11.2% supported by expanded family tax benefits and additional allowances for mothers, and amid declining oil prices and a strengthening forint, Péter Magyar announced an initiative in Parliament to phase out regulated fuel pricing.

The Fed held its interest rates unchanged, while markets declined on the back of a more hawkish-than-expected tone

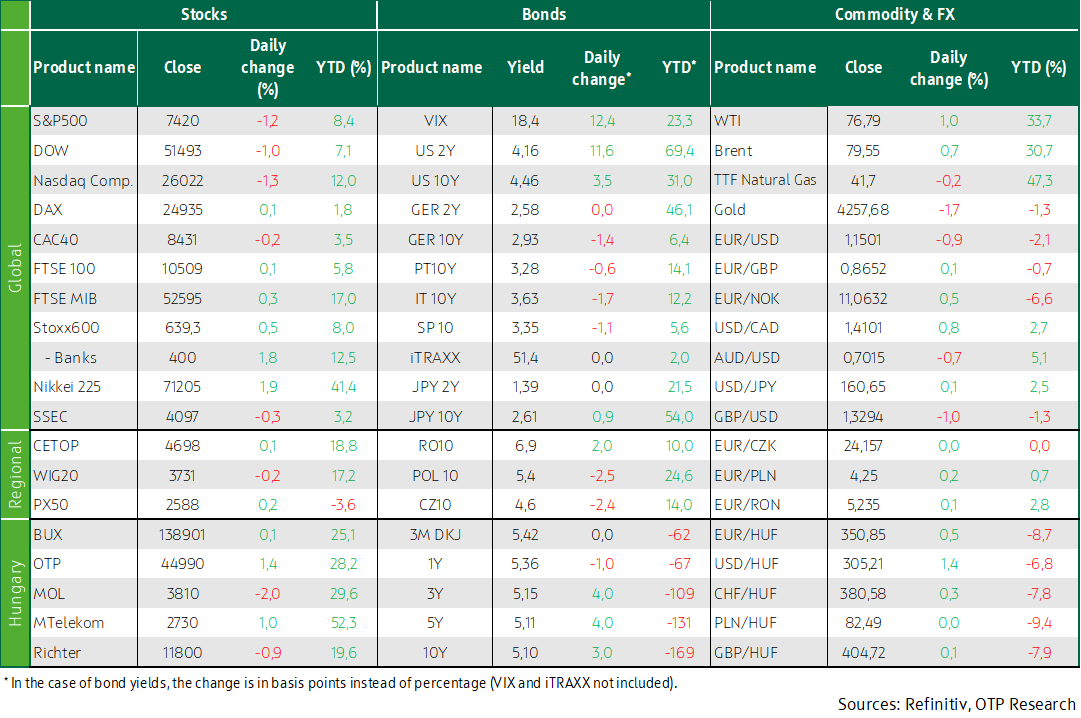

The Federal Reserve left interest rates unchanged on Wednesday in line with expectations, but policymakers signaled a potential rate hike later this year amid rising concerns that CPI could remain above the central bank’s 2% target, with the new quarterly projections showing that nine Fed officials now expect a rate increase by the end of 2026, while the updated monetary policy statement removed the previous reference suggesting a likelihood of further easing this year, which according to the new Fed Chair Warsh had been justified by earlier economic conditions, meanwhile the Fed now sees GDP growth in 2026 at 2.2%, down from the 2.4% projected in March, while the 2027 forecast remains unchanged at 2.3%, and CPI projections were revised higher to 3.6% for this year from 2.7% and to 3.3% for 2027 from 2.7%, with policymakers noting that both economic growth and the labor market remain stable, and following the meeting CME FedWatch data showed that 67.1% of investors now expect a rate hike by September, up sharply from 29.1% on Tuesday.

The Fed’s hawkish tone weighed on markets, with the Dow falling 1.0%, the S&P 500 declining 1.2%, and the Nasdaq dropping 1.3%, while all 11 major S&P 500 sector indices ended lower, led by communication services with a roughly 3% decline, whereas the industrial sector proved the most resilient, closing just 0.1% lower, and regional banks underperformed their larger peers as the KBW Regional Banking Index fell 1.8% compared with a 0.2% drop in the S&P 500 bank index, with one analyst cited by Refinitiv noting that higher interest rates tend to weigh more heavily on regional lenders and also highlighting the 2.3% decline in the State Street SPDR S&P 500 Homebuilders ETF, as a higher rate environment typically puts pressure on the housing market, while among individual stocks SpaceX stood out, snapping its post-listing skyrocketing trend and correcting by 4.9%.

Brent rose by more than 1% on Wednesday to nearly $80 per barrel after US President Donald Trump warned that bombing of Iran could resume if Tehran does not “behave appropriately,” raising fresh uncertainty around a potential ceasefire agreement, adding that a memorandum of understanding with Iran has not yet been finalized and that the possibility of military action remains on the table, despite the fact that the US and Iran had already released the text of a temporary agreement signed by both presidents aimed at ending the conflict.

Yields also reacted to the Fed’s decision, while the forint moved back above the 350 level

Following the Fed’s decision, expectations for rate hikes and the dollar strengthened, while bond yields rose, with the 10-year US Treasury yield barely moving ahead of the announcement but climbing by 6 basis points to 4.5% afterward, as the dollar soared, appreciating by 1% against the euro to the 1.15 level.

The Fed triggered a correction across regional and domestic markets, with regional currencies generally weakening yesterday, particularly in the afternoon, as the zloty slipped by 0.2% and the forint weakened by half a percentage point, moving back above the 350 level, while reference yields published by the Government Debt Management Agency rose by around 5 basis points, with the 10-year yield reaching 5.1%, and demand at the six-month T-bill auction was subdued with only two-thirds of the announced HUF 30 billion issued, whereas at the switch auctions, where investors could exchange bonds maturing this and next year for seven- and fifteen-year securities, HUF 40 billion worth of bonds changed hands.

Today's highlights

Most Asian markets rose, with sentiment dominated by developments surrounding the end of the Iran war, as the Nikkei advanced 1.9%, while a government spokesperson stated that Japan stands ready to respond appropriately to exchange rate movements at any time, with the yen briefly weakening to 160.795 per dollar on Wednesday—near a two-year low—erasing gains following Tokyo’s April 30 intervention, before standing at 160.76 on Thursday, and although a weaker yen boosts corporate profits, it also increases the burden on companies and households through higher import costs, while the Bank of Japan’s rate hike on Tuesday—which lifted the policy rate to a 31-year high—did little to stabilize the pressured currency given that the benchmark rate still stands at just 1%, well below the Federal Reserve’s 3.50–3.75% range, meanwhile the Kospi also rose by 1.9%, while the SSEC edged slightly lower.

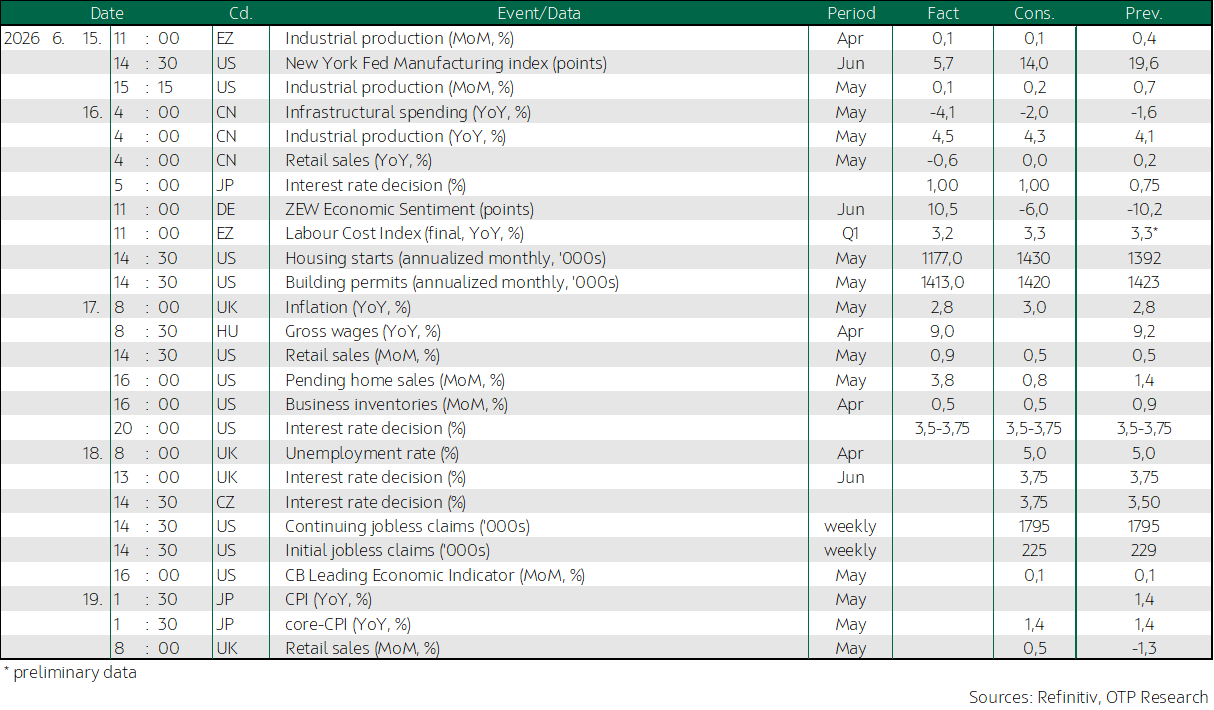

Today, attention in Europe will focus on interest rate decisions in the UK and the Czech Republic, while in the US the usual weekly labor market data releases are also due.

At today’s auction, the Government Debt Management Agency will offer one-year T-bills alongside 10-year floating-rate and 10-year fixed-rate bonds, with announced volumes of HUF 15 billion, HUF 20 billion, and HUF 30 billion, respectively.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more