OTP Morning Brief: US–Iran draft deal details ahead of Friday signing

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

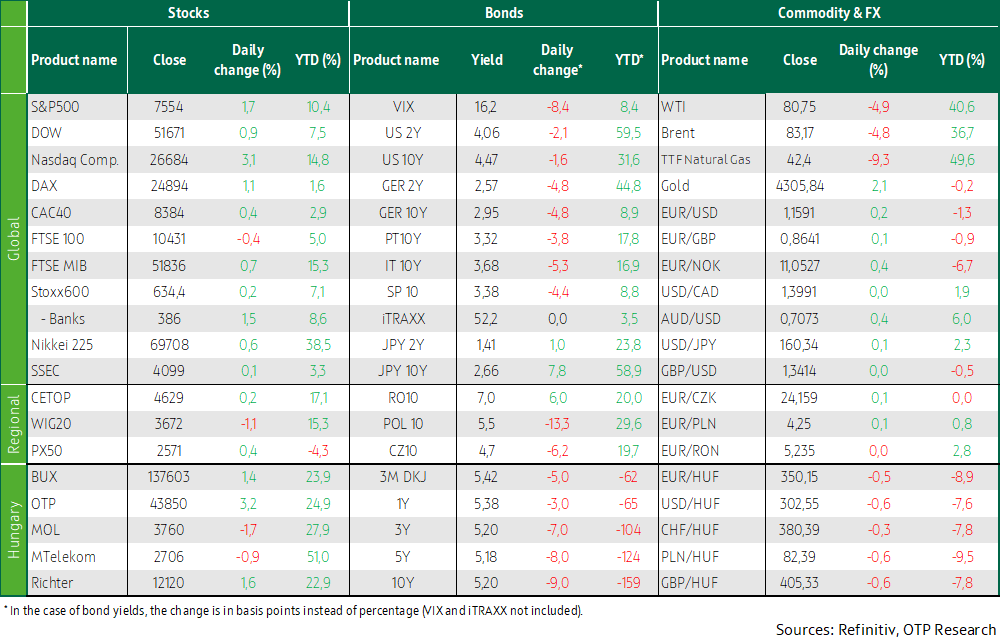

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Monday’s trading on European stock markets was optimistic, with most major indices closing in positive territory. The BUX rose 1.4%, while Hungarian blue chips closed mixed. Brent and WTI crude oil prices fell, leaving the former 15% and the latter 20% above pre-escalation levels of the Middle East conflict. Wall Street indices edged higher; the Dow closed at a new record high. Bond yields in developed markets fell slightly. The euro strengthened somewhat against the dollar. On the Hungarian bond market, yields fell to a four-year low. The forint closed below 351 against the euro. At its meeting today, the Bank of Japan raised its benchmark interest rate to 1.0%, a level not seen since 1995. Today, it will be worth watching whether the market's momentum, fueled by confidence in a resolution to the Middle East conflict, can be maintained.

Following positive news over the weekend, Monday’s trading on major European stock markets was optimistic; the Stoxx 600 closed at a new high; the BUX rose 1.4%

Major European stocks mostly rose on Friday on the promise of an agreement to be signed on Friday as a first step toward resolving the Middle East conflict. The pan-European Stoxx 600 closed at a new high, up 0.2%, with most of its sector indices posting gains. The biggest decline was seen in the energy sector, which fell along with oil prices, while the financial sector, as well as automakers and airlines, which are particularly sensitive to oil prices, led the gains. The British FTSE 100, the only one of the leading European indices to turn red, was unable to rise amid the generally optimistic mood precisely because energy giants and defense sector stocks—which also fell on hopes of a permanent easing of tensions in the Middle East—carry significant weight in the index. The Euro STOXX volatility index fell to its lowest level since the end of January.

Among company news, it is worth noting Renault’s (+3.7%) announcement that the car manufacturer is developing a military vehicle in collaboration with the defense technology company Thales. Schneider Electric rose 1.8% after entering a strategic partnership with Taiwan’s Foxconn to develop and expand infrastructure for artificial intelligence data centers.

Data front: markets focused on the eurozone’s April industrial production data (+0.1% MoM). Industry held up surprisingly well against high energy prices, supported by stronger exports and inventory buildup due to war-related uncertainty. While the reopening of the Strait of Hormuz is fundamentally positive for energy-intensive sectors, it does not in itself provide a significant boost to production, as energy prices may remain persistently high, and eurozone industry must also face the challenge of overcapacity in China’s manufacturing sector.

Among the stocks in the CEE region, only the WIG20 fell into negative territory, while the BUX was the top performer, rising 1.4%, and the PX gained 0.4%. The Warsaw Stock Exchange (-1.1%) fell, like the FTSE100, due to its unique structure, as energy and natural resource giants carry significant weight in the index. Hungarian blue chips closed mixed; OTP performed the best among them, while MOL, which fell along with oil prices, recorded the largest loss.

The news of the imminent Middle East agreement caused not only crude oil prices but also natural gas prices to fall. The European TTF price dropped to around 42 EUR/MWh, which is still 30% higher than the level before the conflict erupted.

The leading Wall Street indices closed Monday trading with a rise; crude oil prices declined

Wall Street indices closed the first trading day of the week with a rise, as—similarly to Europe—investor sentiment was buoyed by a potential agreement taking shape between the US and Iran; Brent crude fell below $84 per barrel (-4.2%), still standing 15% above pre-conflict levels, while WTI dropped by nearly 5% on Monday to below $81, remaining 20% higher than its February 27 price; the decline in oil eased CPI concerns and supported a rise in energy-sensitive sectors such as airlines and shipping companies, while the technology sector also performed strongly as softer inflation worries increased investors’ risk appetite; the Dow closed at a record high, supported by industrial and tech firms benefiting from lower energy costs; the Philadelphia Semiconductor Index posted a sharp surge, driven by chip giants such as Nvidia (+3.5%) and Micron (+10.8%), both of which saw their shares jump following multiple target price upgrades; Fox shares plunged (-15.2%) after announcing a $22 billion acquisition of Roku (-1.9%), whose stock also declined; meanwhile, SpaceX—after debuting on Friday—continued its soar, following a 19.2% gain with a further 19.6% rise on Monday.

Among the published data, the most relevant release was US industrial production for May, which showed a 0.1% month-on-month rise, falling short of expectations, while figures for previous months were revised upward; the subdued reading was mainly driven by stagnation in manufacturing, although the outlook is supported by a pickup in mining activity and an acceleration in oil production.

Developed market bond yields edged slightly lower, while the forint closed below 351 against the euro

Despite favourable news regarding the Middle East conflict, little of the initial optimism remained in developed bond and FX markets; both European and US bond markets opened with a notable decline in yields of up to 5 basis points, but by the close this had narrowed to 1 basis point in the US 10-year yield and 3 basis points in the German benchmark, with the former finishing below 4.5% and the latter below 2.95%; EURUSD followed a similar path, initially strengthening by around half a percent from 1.157, before retreating below the 1.16 level by the evening.

Regional currencies all opened with a rise, but by the end of the session both the koruna and the zloty weakened slightly; meanwhile, the forint reached the 350 level against the euro and still closed below 351 in the evening, marking a 0.3% appreciation; in the bond market, yields fell to new four-year lows, with short-term yields dropping to 5.4% and longer maturities to 5.2%.

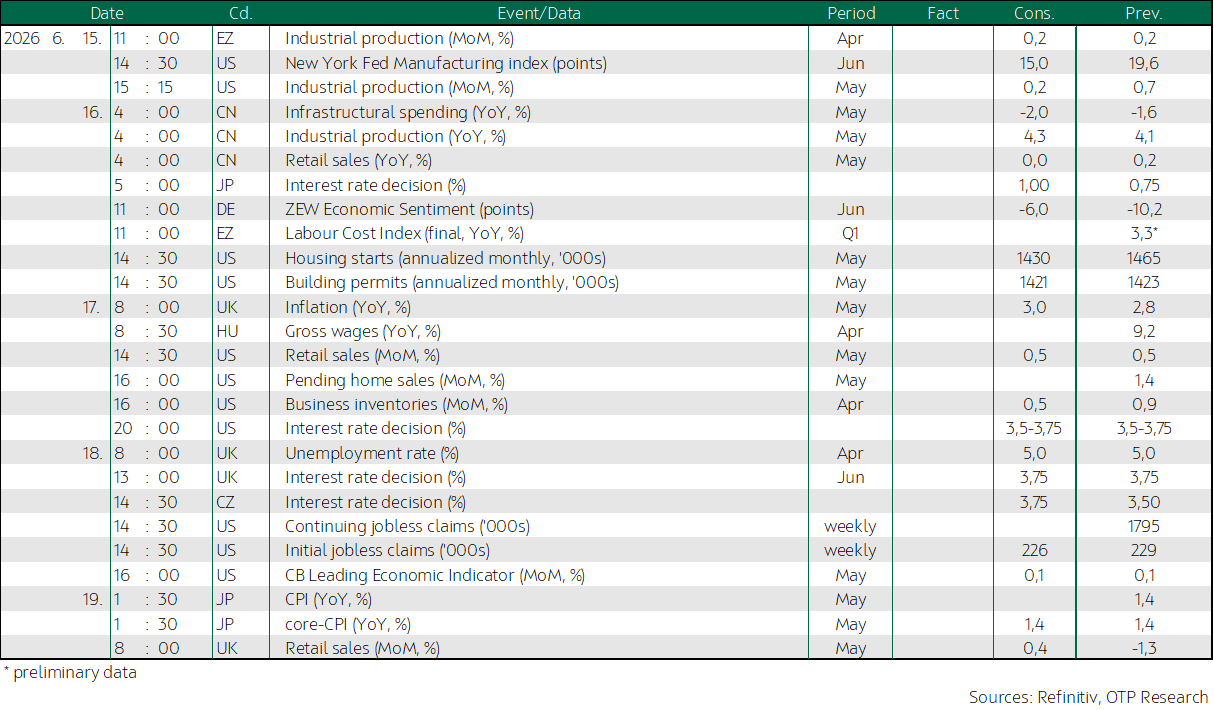

Today's highlights

Mixed movements were seen this morning across Asia-Pacific equity markets, with Japan’s Nikkei 225 even touching a new intraday high; in line with expectations, the Bank of Japan’s Monetary Policy Board raised the benchmark rate to 1.00%, a level not seen since 1995, marking its first hike since last December; the Chinese macro data released this morning painted a mixed picture of the economy, as retail sales declined for the first time in more than three years and investment also contracted, while industrial production showed a rise; meanwhile, crude oil prices extended their decline in early trading today.

Equity index futures point to a mixed opening in both Europe and overseas markets.

The second estimate of the euro area’s Q1 labour cost index is due for release; the initial reading showed a 3.3% year-on-year rise, marking a notable slowdown compared to the CPI-driven period between 2022 and 2024, though the overall picture remains far from reassuring from an inflation perspective.

Germany’s June economic sentiment index from the ZEW Institute is due for release, which is expected to show an improvement compared to the previous month, though it will likely remain in negative territory.

US housing market data for May are due, with expectations pointing to no meaningful change compared to the previous month in either building permits or housing starts; in addition, investors will be closely watching the Fed’s Federal Open Market Committee meeting, which begins today and concludes tomorrow.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more