OTP Morning Brief: ECB raised interest rates

Related content

OTP Morning Brief: Oil prices climbed back above $100, while tech sector earnings reports drove market movements

Global equity indices moved lower after earnings reports from leading technology companies revealed a significant rise in artificial intelligence-related investment costs. At the same time, developments in the Middle East pushed Brent crude prices above $100 per barrel, once again bringing CPI trends into investors' focus. Driven by macroeconomic data and the rise in oil prices, US and European government bond yields increased, while the ECB left its key interest rates unchanged, in line with expectations. The Trump administration will replace the expiring 10% global tariff with a new set of tariffs.

OTP Morning Brief: Middle East Escalation and Earnings Reports Drove Markets on Wednesday

The escalation of the Middle East conflict continued to push energy prices higher. TTF natural gas rose by more than 4%, while Brent crude climbed 3.4%, moving above USD 94 per barrel. The rise in oil prices fueled CPI concerns, leading to higher Hungarian and international government bond yields. Despite these developments, the major Western European equity indices managed to post gains on Wednesday. CPI Came in Lower Than Expected in the United Kingdom. US equity markets moved lower. After the close, Alphabet and Tesla reported earnings, with the initial market reaction proving unfavorable. The substantial investment plans announced by US technology companies, including Alphabet and Tesla, provided support to the share prices of Asian chipmakers. The ECB is expected to keep its key deposit rate unchanged at 2.25% today.

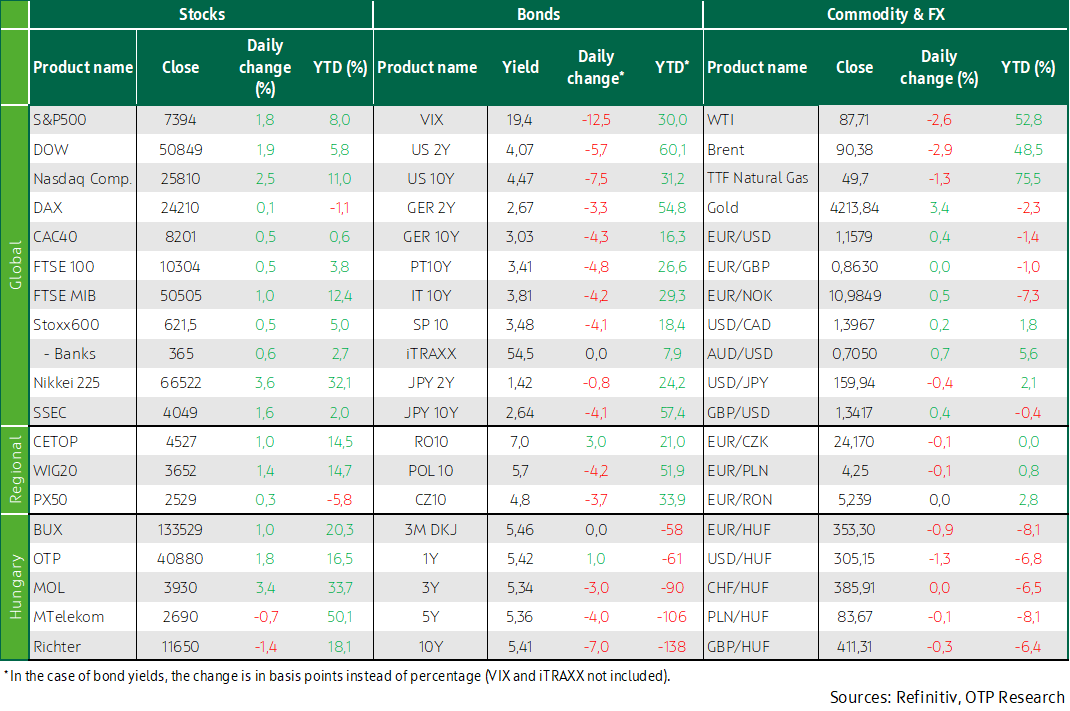

After four days of decline, the pan-European STOXX 600 rose again. In line with expectations, the ECB raised its key deposit rate by 25 basis points yesterday. The ECB projects CPI at 3% this year and 2.3% next year. On positive developments in the Middle East, US indices surged sharply by the close. President Trump walked back the tough strikes he had promised earlier in the day and later spoke of a near-term agreement. After a significant drop, Brent is trading below $90 this morning. US producer prices rose more than expected in May. Bond yields declined on positive developments in the Middle East. Trading in SpaceX shares could begin today on the Nasdaq.

European indices rose again, while theECB raised interest rates

After four days of decline, the pan-European STOXX 600 closed in positive territory again, rising 0.5%. The DAX edged up 0.1%, while the CAC 40 and the FTSE 100 each gained 0.5%.

In line with expectations, the ECB raised its key deposit rate by 25 basis points yesterday. Based on its updated macroeconomic projections, the European Central Bank expects headline CPI at 3% this year and 2.3% next year, revising its March inflation forecast upward. Growth projections for 2026–27 were lowered by 0.1–0.1 percentage points, with the ECB now forecasting euro area GDP growth of 0.8% this year and 1.2% next year. The post-decision statement highlighted the inflationary impact of the Middle East conflict, emphasizing upside risks to inflation and downside risks to growth. Policymakers may still be strongly influenced by the 2021–2022 energy crisis, when central banks reacted with a lag to mounting price pressures, as well as by the slightly stronger-than-expected increase in May core CPI (2.5%). Arguing against further tightening, however, is the weakening economic backdrop since the start of the year (see, for example, the composite PMI).

Interest rate-sensitive sectors underperformed. The financial services sector fell 0.7%, with asset managers ICG and Partners Group down 4.7% and 3%, respectively. Real estate stocks declined 0.8%. Technology shares delivered mixed performance. Within the index, semiconductor manufacturers drove gains, as BE Semiconductor and ASM International rose 6.6% and 7.3%, respectively. Oracle’s 8.5% slump—after guiding for higher-than-expected capital expenditure—weighed on software names, with SAP dropping 6.6%, Capgemini 4.2%, and Dassault Systemes 5.8%.

Hugo Boss rose 9.1% after the UK-based Frasers Group made a $2.3 billion takeover bid for the German fashion company, while Wizz Air jumped 6% as its annual profit beat expectations.

Serbian President Aleksandar Vučić spoke about the possibility of his resignation. An agreement between Mol and the Serbian state—under which Mol, among other commitments, undertook to continue operating the Pančevo refinery at its previous capacity—may give the green light to a deal that would see Mol acquire a majority stake in the Serbian oil company (NIS). In the region, the BUX rose 1%, the WIG20 gained 1.4%, and the PX50 edged up 0.3%.

US indices surged sharply on the back of positivedevelopments in the Middle East

US indices closed the day with sharp gains as headlines on the Iran conflict were increasingly dominated by expectations of a near-term agreement. The S&P 500 rose 1.8%, the Dow Jones gained 1.9%, and the Nasdaq Composite climbed 2.5%.

After the escalation in exchanges over the past weekend, President Trump on Thursday signaled a “very tough strike” against Iran, also hinting that the US could seize Kharg Island, the central hub of the country’s oil infrastructure. Notably, however, oil prices did not react materially to these developments, which may be explained by positive news regarding progress in negotiations. Later in the day, President Trump spoke about a potential agreement that could be reached as early as this weekend and walked back the previously announced attack. Another key factor shaping oil prices is whether, and when, a prolonged conflict would lead to a physical supply shortage. There is no clear consensus on this, with energy analysts divided on the issue. In its latest Global Economic Prospects report, the World Bank’s baseline scenario assumes an average Brent price of $94 for 2026, consistent with a gradual easing of supply disruptions already over the summer. Brent is trading below $90 this morning.

Chipmakers rallied and contributed significantly to the S&P 500’s advance, with the PHLX Semiconductor index jumping 7.9%. Oracle was among the day’s laggards, slumping 8.5% after signaling higher-than-expected capital expenditures for fiscal 2027.

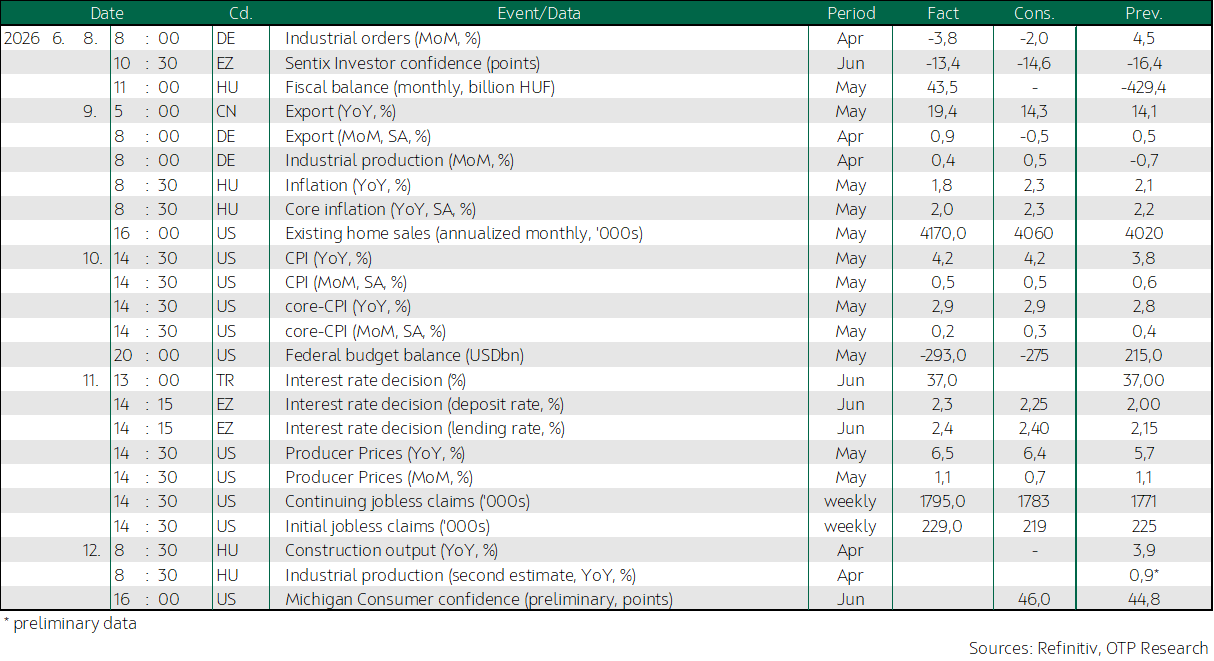

US producer prices rose more than expected in May (+1.1% m/m), signaling intensifying inflationary pressures amid the Middle East conflict. While labor market data—such as the weekly jobless claims released on Thursdays—continue to reflect overall stability, inflation dynamics are becoming increasingly concerning from the perspective of the Fed’s dual mandate. It is therefore not surprising that markets are now pricing in a 25 basis point rate hike by year-end. At next week’s rate decision, it will be worth watching how the updated dot plot changes compared to March, when the median FOMC projection pointed to one rate cut in both 2026 and 2027.

Bond yields declined on the back of positivedevelopments in the Middle East

The European Central Bank raised interest rates by 25 basis points in line with expectations, bringing the key deposit rate to 2.25%, while policymakers reiterated their commitment to achieving the 2% inflation target. The ECB noted that the war in the Middle East is amplifying already present inflationary pressures and revised its CPI projections upward, to 3% for 2026 (from 2.6%) and to 2.3% for next year (from 2.0%). Core CPI is expected to come in at 2.5% both this year and next (instead of 2.3% and 2.2%, respectively). Euro area GDP forecasts were lowered, to 0.8% for this year (from 0.9%) and to 1.2% for 2027 (from 1.3%). Producer price inflation in the US increased, with the headline figure at 6.5% and core CPI excluding volatile items at 4.9%; the former exceeded expectations, while the latter came in below them. Favorable developments emerged later in the day regarding the Middle East crisis, as US President Donald Trump first announced a delay to the planned major strike against Iran, then indicated that negotiations are progressing well, with a deal potentially reached as soon as this weekend, and the Strait of Hormuz possibly reopening next week. As a result, oil prices fell 4% by the evening, with Brent dropping below $90. Consequently, bond yields declined, with the US 10-year yield falling 10 basis points below 4.5%, while in European markets—which had already closed—yields dropped 5 basis points, with the German 10-year yield falling close to 3%. The dollar weakened, slipping nearly 0.5% against the euro, with EURUSD approaching the 1.16 level.

The forint strengthened slightly, while other regional currencies weakened, albeit to a lesser extent, with EURHUF reaching the 355 level again. Demand was very strong at yesterday’s government bond auction held by the ÁKK, particularly for the longest, 10-year maturity. Total bids across the three bonds comfortably exceeded HUF 400 billion. The ÁKK once again increased issuance meaningfully, though by less than in previous auctions, selling HUF 220 billion worth of bonds including the non-competitive tranche, at average yields 3–5 basis points below Wednesday’s benchmark levels. Yields declined slightly further after the auction, with reference yields falling 3–7 basis points compared to Wednesday, while the 10-year yield is approaching the 5.4% level.

Today's highlights

Asian equity markets are also rising sharply approaching the close. The Nikkei is up 3.6%, the KOSPI 8.4%, the SSEC 1.6%, while the Hang Seng is 2% higher.

In Hungary, the statistical office will release April construction output data and the second estimate of industrial production today. In the US, the University of Michigan’s consumer confidence index for June is due. SpaceX will be in focus, as it is expected to begin trading on the Nasdaq.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more