OTP Morning Brief: The Middle East ceasefire and the tech sector remain under pressure

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Although tensions in the Middle East eased on Monday, a downed Apache helicopter and an attack on a southern Lebanese port city triggered a renewed rise in instability. By morning, escalation had already materialized, with both the US and Iran launching strikes against each other. Meanwhile, the decline in the technology sector continued, weighing on markets in both Europe and overseas. The Bux fell by 0.3% on Tuesday. German economic data showed some improvement in the country’s economic performance. Domestic inflation stood at 1.8% in May, which could provide room for a rate cut. Yields declined. Oil prices moved in an uncertain direction. The forint remained below the 356 level against the euro. Following Wednesday’s surge, Asian stock markets fell sharply. Today, attention will be on the release of US CPI data.

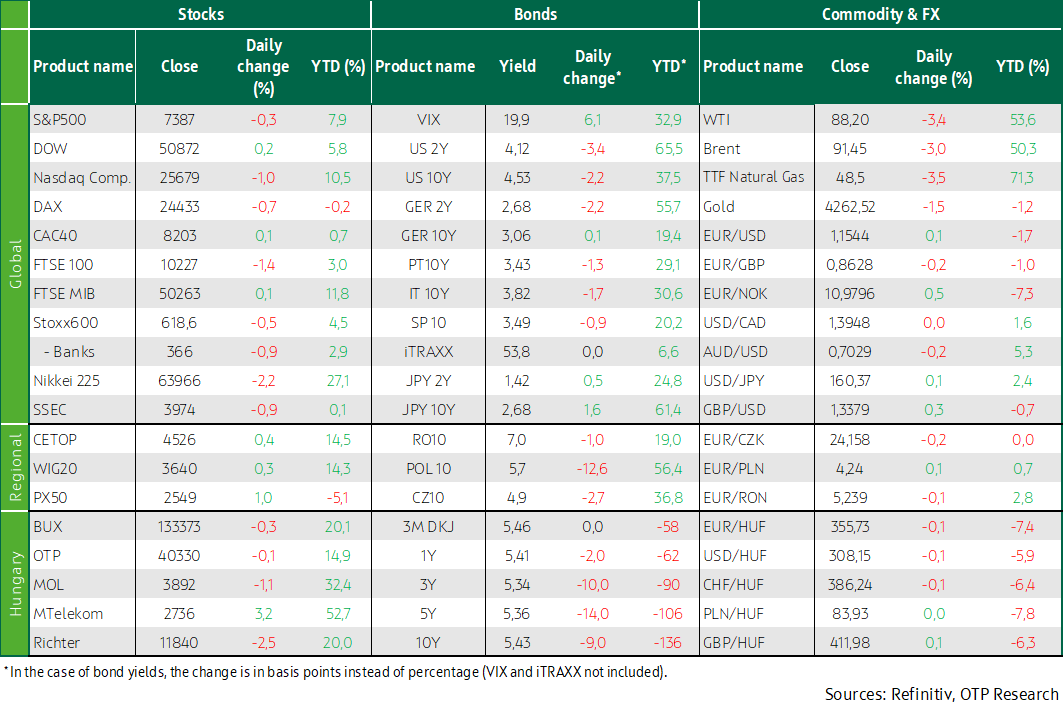

European equities declined again on Tuesday, German exports saw a notable rise, and domestic CPIcame in at 1.8% in May

European equities reversed course in the second half of Tuesday’s session, giving up earlier gains and extending their losing streak to a third consecutive day, driven primarily by weakness in commodity-related stocks as investors weighed the fragile ceasefire between Iran and Israel. The pan-European STOXX 600 index declined by 0.5%, with the FTSE 100 dropping 1.4%, the DAX falling 0.7%, and the CAC 40 posting a slight increase. Within the STOXX, mining and energy shares led losses, declining by 2.5% and 2.4% respectively, while European technology stocks also moved lower, ending 1.3% down after showing notable volatility recently. In other sectors, telecom stocks fell by 2%, partly due to declines in Ericsson and Nokia following news that Nvidia may develop technology for mobile networks, while European defense stocks slipped 0.7% after Morgan Stanley downgraded the sector.

Based on data released yesterday for April, German industrial production recorded a 0.4% monthly rise, falling short of analysts’ expectations, but showing a marked improvement compared to previous months. Meanwhile, German exports exceeded forecasts, posting a 0.9% monthly increase instead of the anticipated 0.5% decline.

Sentiment in the CEE region was mixed, with the WIG 20 gaining 0.3% and the PX rising 1%, while the BUX declined by 0.3%. Among Hungarian blue chips, all but Magyar Telekom moved lower, with Richter posting the steepest drop at 2.5%. Domestic CPI stood at 1.8% year-on-year in May, coming in below our expectation of 2.0%, the market consensus of 2.3%, and the central bank’s forecast, suggesting that the low reading could provide room for the MNB to consider a rate cut. Core inflation came in at 2.0% over the same period.

Downed helicopter threatens the ceasefire, while the tech sector continued to decline

Investors continued to monitor developments in the Middle East conflict. Although tensions between Israel and Iran appeared to ease on Monday following Trump’s intervention, the US president announced Tuesday evening that Iran had shot down a US Apache helicopter in the Strait of Hormuz and vowed retaliation, further deepening doubts about the prospects for peace between the two countries. Meanwhile, an Israeli strike in southern Lebanon left eight people dead, adding further complexity to the situation. According to reports this morning, the promised countermeasures have materialized, with the US military stating on X that it had targeted Iranian air defense units, ground control stations, and surveillance radar systems near the strait. In response, Iran’s Revolutionary Guard announced that it carried out attacks on a US base in Jordan as well as 21 additional targets across the Gulf region on Wednesday.

The S&P 500 and Nasdaq indices declined on Tuesday, with the former slipping 0.3% and the latter falling 1%, driven partly by developments in the Middle East and partly by the fading rebound in technology stocks. The Cboe Volatility Index (VIX) climbed to its highest level since April 7 during the session. By the close, the technology index dropped 1.8%, while the semiconductor index ended 1.9% lower. Shares of Broadcom fell 1.1% on Tuesday, while Nvidia edged down just 0.2%. Beyond the chip sector’s decline, the broader AI space also came into focus after OpenAI, the developer of ChatGPT, announced it had filed for an IPO, just over a week after its rival Anthropic, behind Claude, made a similar move. Apple shares closed 3.6% lower as investors and analysts reacted cautiously to the company’s latest product unveilings and announcements at its annual Worldwide Developers Conference.

Yields declined, while the forint remained below 356

Commodity traders were still pricing in de-escalation on Tuesday, pushing oil prices down by 2.5% to around $90, though they began to rise again by morning. The US 10-year Treasury yield fell to around 4.5%, while European yields declined more modestly, with the German 10-year yield holding near 3.05%. The dollar weakened slightly, with EURUSD recovering to 1.115.

The forint’s exchange rate against the euro remained largely unchanged, holding below the 356 level, while neither the zloty nor the koruna showed any meaningful movement. Weaker-than-expected CPI data and a decline in external yields led to a drop in benchmark yields on the domestic bond market by around 10 basis points, with the 10-year yield easing to 5.4%. At the Government Debt Management Agency’s (ÁKK) three-month T-bill auction, demand was subdued, yet HUF 38 billion worth of securities were sold versus the announced HUF 30 billion, at an average yield of 5.54%.

Today's highlights

Asian equity markets declined on Wednesday as risk aversion increased following a renewed flare-up in military tensions between the US and Iran, while the earlier rebound in technology stocks also lost momentum. South Korea’s KOSPI was the region’s worst performer, dropping 6.5%, dragged lower by further losses in leading chipmakers after Monday’s sharp decline. Chinese (SSEC -0.9%) and Japanese (Nikkei -2.2%) equities also moved lower, as local inflation data amplified concerns about the inflationary impact of a potential conflict involving Iran.

Today, alongside developments in the Middle East, the focus will be on the release of US May CPI data, which is expected to further reinforce inflation concerns: the market anticipates core inflation of 0.3% month-on-month and headline inflation of 0.5%.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more