OTP Morning Brief: The technology sector once again drove US indices higher on Monday

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

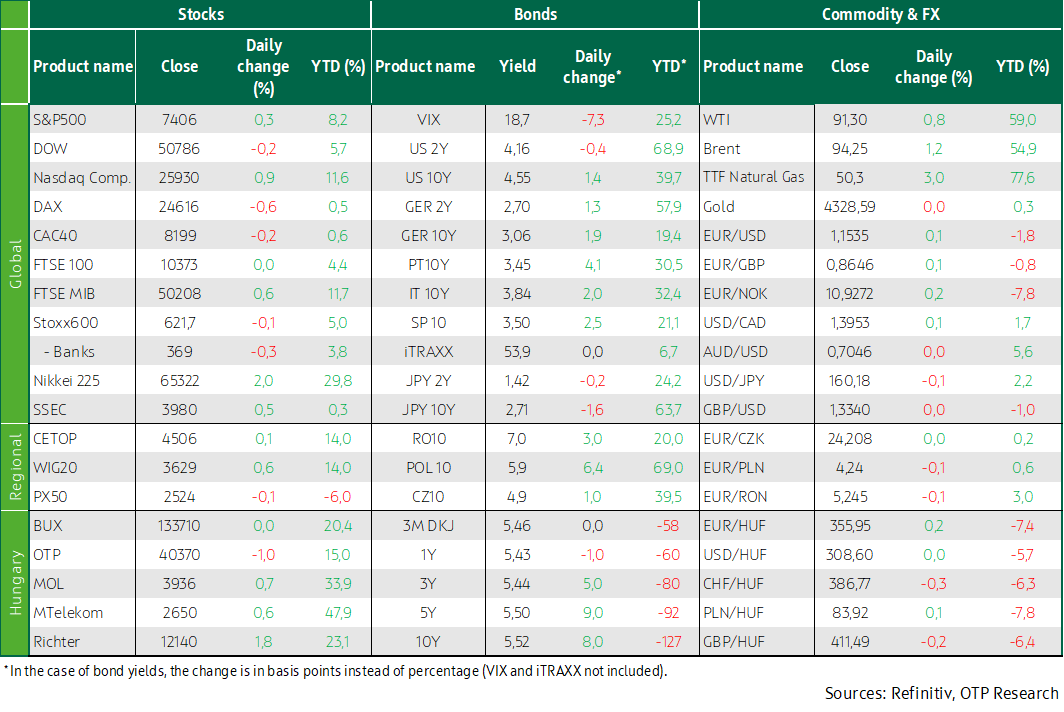

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Following the weekend escalation of the Middle East conflict, oil prices saw a notable rise at the Monday open, while long-term bond yields surged. During the session, at the urging of the US, Iran and Israel halted their attacks, and news of the ceasefire led oil prices to correct. Equity sentiment remained subdued in Europe, while in the US the technology sector regained momentum following Friday’s pullback. Although gains were narrow in breadth, both the S&P and the Nasdaq ended the session higher. Both developed market and domestic bond yields ended the day higher, with EUR/USD around 1.153 and EUR/HUF finishing Monday’s trading just below 356. OpenAI has announced plans to go public, following the path of companies like SpaceX and Anthropic. Sentiment in Asia is positive today, with Japanese and South Korean equity indices trading higher ahead of the morning close. Investors will be watching domestic CPI data, as well as Germany’s trade and industrial production figures.

Developments in the Middle East over the weekend weighed on European equity markets, with major benchmarks closing the day slightly lower

Renewed airstrikes by Iran and Israel pushed oil prices higher on Monday morning, while European equities opened the day in negative territory, however sentiment improved later after President Trump urged a halt to the actions, and the Iranian military’s announcement of a ceasefire helped stabilize markets, the Stoxx 600 rebounded from its two-week intraday low and ultimately closed down just 0.2%, Germany’s DAX lost nearly 1%, France’s CAC 40 declined by half a percent, while the FTSE 100 ended the session close to Friday’s closing level, Italy’s FTSE/MIB also finished slightly lower despite a positive market reaction to Intesa Sanpaolo’s €30.6 billion takeover bid for Monte dei Paschi di Siena, with the latter soaring 13% although the potential acquirer slipped by more than 1%, among Stoxx 600 sector indices technology delivered the strongest performance rising 1.3%, while the chemical sector saw the steepest decline as Goldman Sachs highlighted downside risks for the European chemicals industry citing faster-than-expected demand erosion and pressure from Chinese imports, on the stock side Zealand Pharma stood out with shares plunging 23% after many participants discontinued trials of its weight-loss injection due to side effects.

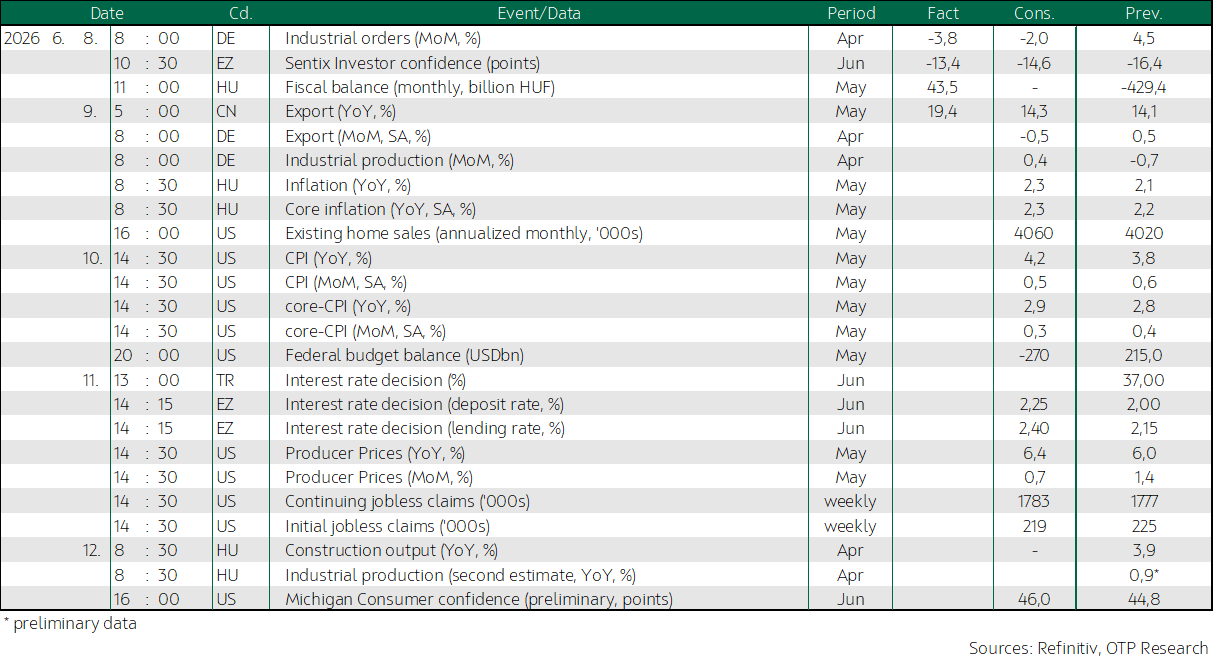

The macro data released yesterday were mixed: German factory orders fell by 3.8% month-on-month in April, coming in below market expectations, while the previous month’s figure was also slightly revised downward, at the same time the Sentix euro area investor confidence index showed a modest improvement, whereas the market had expected a further decline.

Trading in the CEE region got off to a mixed start to the week, with Poland’s WIG20 rising 0.6%, the BUX edging 3 basis points higher, while the Czech PX slipped 0.1%, among Hungarian blue chips Richter stood out with a nearly 2% gain, while Mol and Magyar Telekom advanced 0.7% and 0.6% respectively, whereas OTP declined by close to 1%.

According to data released yesterday, the domestic budget posted a surplus of HUF 45.3 billion in May.

European gas prices followed a path similar to crude oil on Monday: after an initial sharp surge, quotes fell by nearly EUR 2 from around EUR 51/MWh, however by the end of the day uncertainty surrounding the situation drove prices higher again and trading ultimately closed near EUR 50/MWh, up 3%. Israeli Prime Minister Benjamin Netanyahu stated that Israel is temporarily suspending its attacks against Iran but will respond if Tehran resumes hostilities, while Iranian media signaled a similar stance. Meanwhile, traffic through the Strait of Hormuz remained significantly constrained, raising concerns about whether Europe will be able to replenish its gas reserves before winter.

Following Friday’s sell-off, sentiment reversed once again, with the technology sector leading the indices higher

Following Friday’s downturn, Monday trading on US equity markets brought a correction, although the session also started in negative territory due to the escalation of the Middle East conflict. The latest wave of attacks marked the largest direct confrontation between Iran and Israel since the April ceasefire. The halt in strikes helped calm markets, while news from the technology sector once again provided strong momentum to indices after the previous sell-off. The S&P technology sector index rose by nearly 2%, while the Philadelphia Semiconductor Index soared by more than 6%. The S&P closed up 0.6% and the Nasdaq gained 1.3% after US-listed chipmakers suffered roughly $1 trillion in losses on Friday. However, Monday’s equity market rise was narrow-based, with 60% of S&P 500 companies ending in the red, and among sector indices only IT and energy finished in positive territory.

Intel shares surged by 11% on Monday after The Information reported that Google had placed an order for more than 3 million Tensor Processing Units (TPUs) to be produced by 2028. Apple CEO Tim Cook opened the company’s annual developer conference by stating that the announcements would focus on Apple Intelligence and Siri, later unveiling an updated version of the assistant, yet Apple still closed 1.9% lower. Meanwhile, amid heightened sentiment, chipmakers continued to rise, with Nvidia up 1.7% and Broadcom 2.8%, while AMD jumped 5% and Micron skyrocketing by nearly 10%. Tesla also climbed more than 4.5% as Elon Musk’s SpaceX approaches its Friday IPO. The SpaceX listing will serve as a major test for US equity markets, with investors remaining cautious toward the exuberance surrounding the offering. Among other notable gainers in the technology sector was Marvell Technology, which soared nearly 10% after the chipmaker was confirmed to join the S&P 500 effective June 22.

Energy sector companies also performed well on Monday amid rising oil prices, while within healthcare Eli Lilly stood out with a 1.6% gain after the drugmaker’s clinical trial results showed that its new anti-obesity medication, retatrutide, not only supported weight loss and alleviated knee pain but also reduced the severity of sleep apnea.

Brent closed Monday trading at USD 94 per barrel and WTI at USD 91, marking an increase of around 1% compared to Friday following a significant escalation in Middle East tensions over the weekend. Although Iran and Israel agreed on Monday to suspend attacks against each other, raising hopes for the continuation of peace talks, and the ceasefire remains in place, the Strait of Hormuz is still effectively shut due to a dual blockade by the US and Iran, severely constraining the transport of crude oil, refined fuels and natural gas to global markets.

Bond yields in both domestic and developed markets continued to rise on Monday; the EUR/USD hovered around 1.155, while the forint closed with a slight weakening against the euro

Trading yesterday opened in a strongly negative mood due to the renewed escalation of the Middle East conflict, with oil markets opening up 5% and bond yields rising sharply. However, news pointing again to the proximity of a ceasefire emerged, easing the rise in oil prices to around 1–2%. Despite this, bond markets still closed with higher yields, with the US 10-year rising by 5 basis points to approach 4.6%, while European yields increased by 2–4 basis points, pushing the German 10-year above 3.05%. The dollar weakened slightly, with EUR/USD moving toward 1.155.

Regional FX markets opened in a gloomy mood, with the forint jumping from around 355 to above 357, but it recovered by the end of the day and closed just below 356 with only a marginal 0.1% depreciation. The Czech koruna and the zloty posted slight gains. Government bond benchmark yields published by the ÁKK early in the afternoon, before the improvement in the external environment, reflected an increase of 6–10 basis points, with the 10-year yield rising to 5.5%.

Today's highlights

Sentiment is strong across Asian equity markets this morning, with most Japanese indices posting gains of 1–2%, the Shanghai Composite up 0.5% in early trading, and South Korean indices skyrocketing by 7–8%. China’s exports exceeded expectations, expanding by 19% year-on-year in May.

OpenAI, the developer of ChatGPT, also announced its intention to launch an IPO on US stock exchanges on Monday, joining its rival Anthropic. The company did not disclose the size or terms of the offering and noted that the timeline has yet to be determined. However, Reuters reported that the AI giant could target a valuation of up to $1 trillion at its market debut, which could take place as early as September. In prediction markets betting on future events, most participants expected OpenAI to file for its IPO ahead of Anthropic.

US equity index futures point to a positive opening, while Europe may see a mixed start to the day.

Later in the day, the focus on the international stage will be on German industrial production and foreign trade data, as well as US existing home sales figures.

Domestically, the May CPI release is set to be in focus, which according to our expectations could show a 2.1% year-on-year increase in prices, similar to April, while the median forecast of analysts surveyed by Reuters points to a 2.3% annual rate.

Today, the ÁKK will offer three-month Treasury bills, with a planned issuance amount of HUF 30 billion.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more