OTP Morning Brief: The tech sector’s decline dragged down stock markets on Friday

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

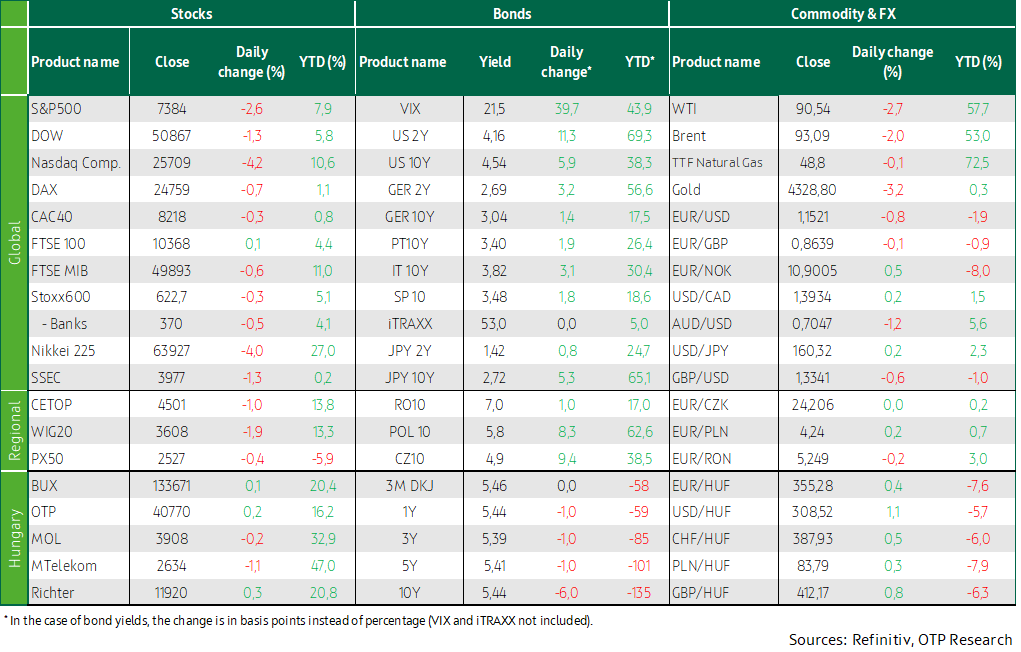

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

The world’s major stock markets closed lower on Friday and for the week as a whole, driven by the tech sector’s weak performance, amid investor sentiment further dampened by the unresolved conflict in the Middle East. Stock markets in the CEE region closed in the red on a weekly basis. The eurozone’s Q1 GDP was revised downward due to a significant revision of Ireland’s GDP. Much stronger-than-expected figures were reported in the May U.S. jobs report, which reinforced interest rate hike expectations. Although Brent and WTI prices fell on Friday, they rose over the week. Yields rose in developed bond markets. The dollar strengthened against the euro. On the back of the dollar’s strength, currencies in the CEE region weakened. Hungarian bond yields rose. Today, it will be worth keeping an eye on April’s industrial production data from Germany and the eurozone’s June Sentix Investor confidence index. The conflict in the Middle East escalated over the weekend, which could weigh on investor sentiment today.

On Friday—and over the week as a whole—the leading European indices fell, with the technology sector showing weakness; stock markets in the CEE region also declined over the past week

Leading European stock markets—except for the UK’s FTSE 100—ended Friday in negative territory and also posted weekly losses, with the pan-European Stoxx 600 slipping 0.3% on Friday and recording a 0.5% decline for the week. The technology sector—after a notable rise of around 30% over the past two months—underperformed, as semiconductor and AI companies’ shares led the fall. Confidence in the sector was further undermined by Broadcom’s disappointing results published on Wednesday, which intensified concerns. Earlier in the week, the European Commission presented legislative proposals aimed at boosting Europe’s cloud, artificial intelligence, and semiconductor industries while reducing dependence on major US corporations. Meanwhile, the unresolved conflict in the Middle East kept investors cautious; persistently elevated energy prices, driven by the continued disruption of safe passage through the Strait of Hormuz, strengthened CPI concerns and expectations of further rate hikes. In this unfavorable market environment, a notably strong US labor market report for May reinforced expectations of additional policy tightening, further weighing on equity market sentiment.

Due to a significant revision of Irish GDP, euro area Q1 growth was adjusted from +0.1% to -0.2% quarter-on-quarter and from 0.8% to 0.3% year-on-year, while excluding Ireland, annual growth reached 1%. The most important macro release of the week was the eurozone’s CPI, which rose to 3.2% in May, published on Tuesday; the increase was driven primarily not by energy or food prices but by higher service costs. This composition of inflation strengthens expectations that the ECB will raise interest rates at its meeting scheduled for Thursday.

Sentiment in CEE equity markets was also unfavorable on Friday, with both the WIG20 and PX50 closing in negative territory, while the BUX managed to edge slightly higher by the end of the session. Among the main Hungarian blue chips, only OTP and Richter moved higher into the close. On a weekly basis, regional indices declined, while among domestic heavyweights OTP and Magyar Telekom advanced.

According to preliminary data published by the Hungarian Central Statistical Office (KSH) on Friday, industrial production in April exceeded the previous year’s level by 0.9%, while seasonally adjusted output fell by 1.1% month-on-month. The most important domestic macro release of the week was the detailed estimate of Hungary’s Q1 GDP, showing an expansion of 1.7% year-on-year and 0.8% quarter-on-quarter (SA).

Fitch Ratings maintained Hungary’s sovereign rating at BBB and kept the outlook negative in its review on Friday.

In line with the rise in global energy prices, the TTF natural gas price on the Dutch exchange climbed back close to EUR 50/MWh. European gas storage levels stood at 39% on May 28, marking the lowest level since the 2022 energy crisis.

The technology sector underperformed; leading Wall Street indices fell; the US labor market showed stronger-than-expected momentum in May

On Friday, Wall Street’s nine-week rising streak came to an end after technology stocks—previously soaring to record highs—posted their largest daily decline of the year. The pullback was primarily driven by a stronger-than-expected US labor market report for May, which amplified concerns about a tighter-than-anticipated monetary policy stance from the Fed. Selling pressure was concentrated mainly in chipmakers and other technology names that had seen significant gains in recent weeks, dragging the Nasdaq down by more than 4%. The S&P 500 fell 2.6%, while the Dow declined 1.4% on Friday.

In May, non-farm employment in the US increased by 172,000—the strongest gain so far this year—while the unemployment rate remained unchanged at 4.3%, and wage growth came in at 0.3% month-on-month following 0.2% in the previous month. This dataset, along with earlier releases this week—namely April job openings and the ADP Institute’s May employment figures—reinforced the picture of a resilient labor market. Rate hike expectations clearly strengthened, as these data points give the Fed room to focus on price stability within its dual mandate of maximum employment and stable prices, increasingly supporting not just a hold but the case for further tightening.

On a weekly basis, the Nasdaq fell by 4.7%, the S&P 500 declined by 2.6%, and the Dow slipped 0.3%, in line with the downturn in the technology sector and mounting concerns related to the unresolved conflict in the Middle East.

Driven by hopes for a potential agreement between Iran and the US, as well as progress in negotiations between Israel and Lebanon, oil prices fell by around 10% in the last week of May; however, as the conflict entered its fourth month, last week saw a renewed rise in crude markets, as positions appeared no closer despite earlier promises. Although crude prices dropped by more than 2% on Friday, on a weekly basis WTI still rose by nearly 4%, while Brent increased by slightly more than 1%.

Over the weekend, OPEC+ members decided on another production quota increase; following the June hike of 188,000 barrels, a similar-scale increase was approved for July, although several Gulf countries remain unable to raise output due to the closure of the Strait of Hormuz.

Domestic and developed market bond yields moved higher; the dollar strengthened against the euro; and regional currencies weakened amid the stronger dollar

For the first time in a long while, developed bond markets last week were driven primarily not by oil prices. The Strait of Hormuz remained closed, but in the first half of the week there was still a prevailing narrative from the US suggesting that Iran, Israel, and Lebanon had agreed to a conditional ceasefire, although a swift resolution remains uncertain. Macroeconomic news strengthened expectations of rate hikes. In Europe, CPI rose to 3.2% in line with expectations, while core inflation and services inflation exceeded forecasts, soaring to 2.5% and 3.5%, respectively. In the US, following earlier rising inflation data, most of the released labor market figures pointed to a distinctly strong and stable employment environment. In line with this, the market-implied probability that the Fed will be forced to deliver at least one rate hike this year climbed to 80%, while the likelihood of two hikes by next summer stands at 60%. After the strong May labor market report, the US 10-year yield rose by 8 basis points on Friday afternoon and by a total of 10 basis points over the week, approaching 4.55%. Over the same period, the German 10-year yield also moved higher by 10 basis points, nearing 3.05%. Following the US labor market data on Friday, the dollar strengthened by 0.8% against the euro and by more than 1% over the week as a whole, with EUR/USD trading around 1.152.

On Friday, regional currencies weakened due to the strengthening dollar, with the Czech koruna and the zloty slipping by 0.1%, while the forint declined by 0.4% on the day and by 0.5% over the week as a whole, reaching around the 356 level. Reference yields published by the Hungarian Government Debt Management Agency (ÁKK) in the early afternoon still showed a slight decline of a few basis points compared to Thursday, but the global rise in yields following the US labor market data also hit the domestic market, pushing yields 5–10 basis points higher by the end of the day; the Hungarian 10-year yield climbed to around 5.55%, roughly 20 basis points above the previous week’s close. Czech and Polish yields also moved higher last week, rising by 10–15 basis points at the 10-year maturity, somewhat less than the increase seen in Hungary.

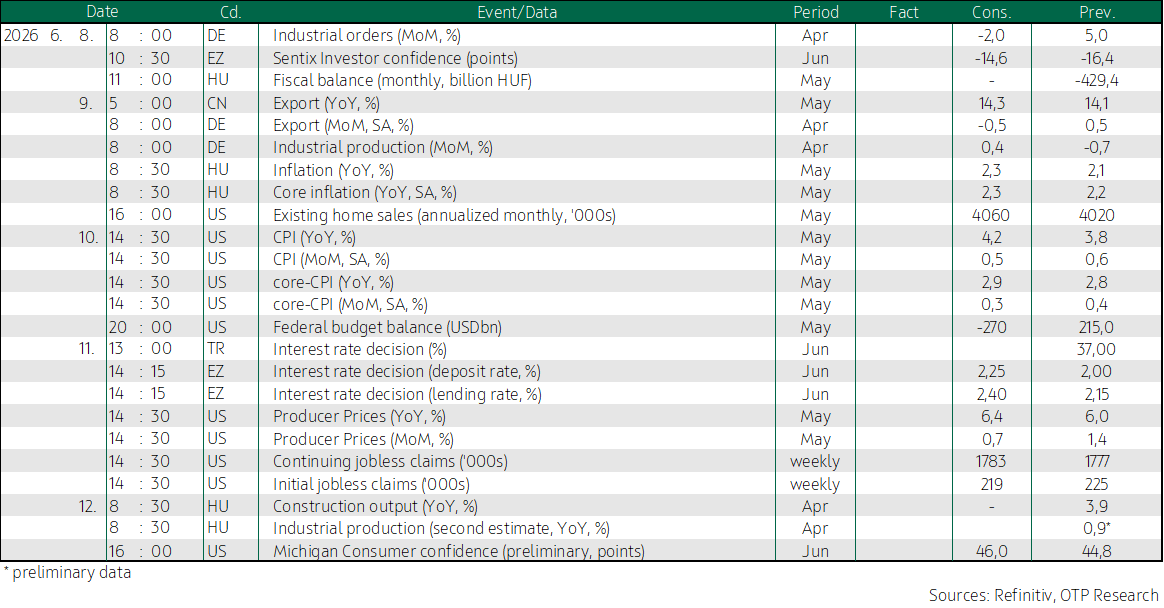

Today's highlights

Leading Asia-Pacific markets opened the week with declines following weekend developments in the Middle East. On Saturday, a new exchange of fire broke out between Iran and the US, followed on Sunday by the most severe escalation since April, as Israel and Iran responded to each other’s attacks. Israel intercepted a missile launched from Yemen, from the base of the Iran-backed Houthi militia, marking an unprecedented development since April.

Futures indicate mostly negative openings in Europe, while on Wall Street the Dow may start the day in the red, whereas the S&P 500 and the Nasdaq could move higher.

Today, attention will focus on April industrial production data from Germany and the eurozone’s June Sentix investor confidence index. In the former case, the market expects a noticeable decline following the rebound in the previous month, while in the latter, the index may remain in negative territory despite a slight improvement.

Later this week, Hungary’s May CPI data will be released; according to our expectations, the pace of price growth remained at 2.1% year-on-year, similar to April, while the median forecast of analysts surveyed by Reuters points to a 2.3% annual figure.

CPI data for May will also be released from the US, with expectations pointing to a further acceleration in the pace of price growth.

The ECB will hold a rate-setting meeting on Thursday, where markets expect a 25 basis point increase in both the key refinancing rate and the deposit rate.

Among corporate news, the biggest highlight of the week could be SpaceX’s IPO scheduled for June 12: Elon Musk’s space company plans to raise USD 75 billion, potentially marking the largest public offering of all time. The current record holder, Saudi Aramco, raised USD 25.6 billion in its 2019 debut. It will also be worth watching how investors react to Sunday’s announcement that Italy’s Banco BPM has invited Banca Monte dei Paschi di Siena to begin talks on a potential merger, which could create Italy’s second-largest banking group.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more