OTP Morning Brief: Markets mostly rose on Thursday following news of a ceasefire between Israel and Lebanon

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

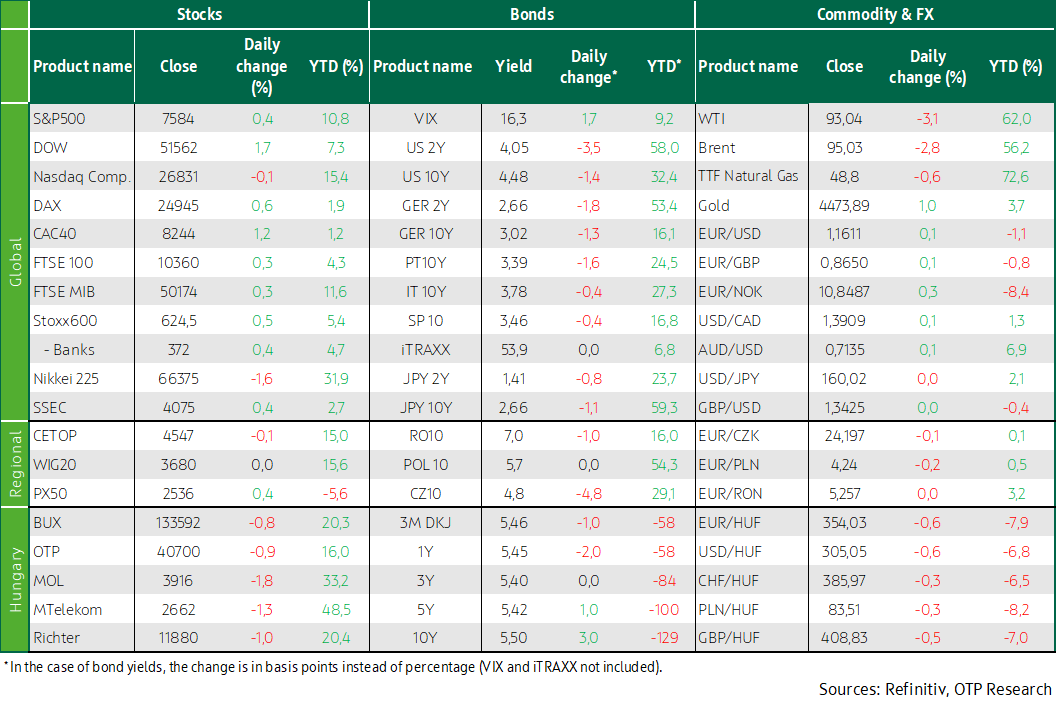

Oil prices fell on news of the Israel–Lebanon ceasefire, while Western European stock markets rose. However, the BUX underperformed. In the US, disappointing results from Broadcom dragged down semiconductor stocks, but news related to the ceasefire and a House resolution curbing Trump’s war plans improved sentiment. Long-end developed market yields fell, rate hike expectations eased, and regional currencies edged higher. Domestically, the statistical office will release industrial production data today, while Fitch’s rating review is due in the evening. In the US, the May labor market report could be the most noteworthy.

Oil prices fell on news of the Israel–Lebanon ceasefire, while Western European stock markets rose. However, the BUX underperformed

European equity markets rose on Thursday as oil prices declined, although investors remained cautious about whether the latest developments in the Middle East would lead to a lasting peace agreement. Brent crude futures fell 2.8% to $95 per barrel after Israel and Lebanon agreed on Wednesday to implement a ceasefire, however hopes for broader de-escalation were dampened after Hezbollah rejected the deal, while Israel stated it would not withdraw its troops from Lebanon, complicating US President Donald Trump’s efforts to secure a peace agreement with Iran. The pan-European STOXX 600 index closed 0.5% higher, driven mainly by strength in the healthcare sector, with French biotech firm Abivax surging 17.8% to recover earlier losses from the week, while the STOXX 600 remains on track for a modest weekly decline.

Chip stocks weakened, with Infineon Technologies and STMicroelectronics falling by 3.4% and 2.6%, respectively, after US-based Broadcom reported weaker-than-expected second-quarter revenue. Software and IT shares continued to rise, extending their recovery from the earlier sharp sell-off driven by disruptions related to artificial intelligence, with Capgemini, Nemetschek, Dassault Systemes, SAP, and Sopra Steria climbing between 6.39% and 8.79%.

Shares of UK financial firms with exposure to China fell after Chinese media reported that mainland residents are facing stricter restrictions when opening offshore accounts at major Hong Kong banks. HSBC, Standard Chartered, and Prudential declined between 1.8% and 7.6%.

Among individual stocks, Rémy Cointreau rose 9.8% after its CEO, Franck Marilly, outlined the company’s three-year plans and said the beverage group aims to increase operating profit by around €100 million. Shares of Puma gained 4.5% after Citigroup upgraded the stock to “buy” from “neutral.”

Regional markets showed a mixed picture: the Czech market managed to rise, while the BUX underperformed with a 0.8% decline (the Polish WIG20 was closed). All domestic blue chips ended the session in negative territory, with MOL posting the largest drop, falling 1.8%.

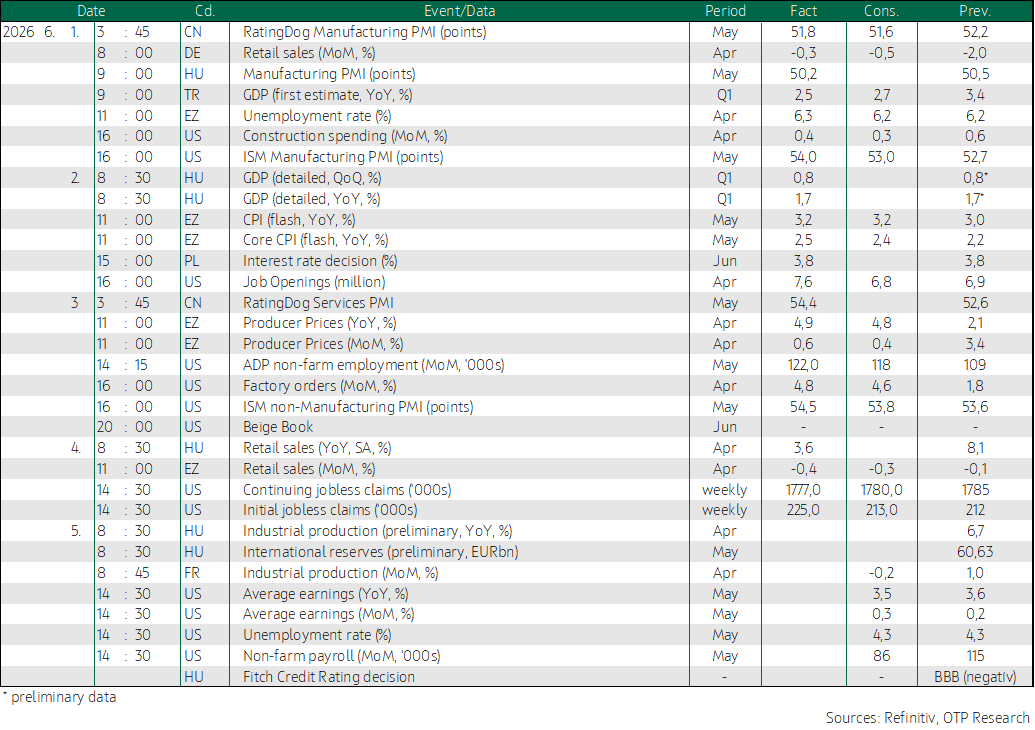

In Hungary, retail sales weakened on a monthly basis in April, declining by 1.2% (adjusted for calendar and seasonal effects) following a nearly 2% month-on-month increase in March. The dynamics were largely driven by fuel sales, and excluding this factor, the indicator slipped by 0.7% after the fading of the Easter effect.

In the US, disappointing results from Broadcom dragged down semiconductor stocks, but news related to the ceasefire and a House resolution curbing Trump’s war plans improved sentiment

After an initial decline, the Dow and the S&P ended the session in positive territory, with the former closing at a new record high. News related to the end of the Iran war improved investor sentiment, while disappointing results from Broadcom triggered a sell-off in chip stocks, limiting gains in the Nasdaq. The Dow reached an all-time high, driven by healthcare and financial shares, but gains in the S&P 500 were more moderate, while the Nasdaq remained flat. Chipmaker Broadcom missed revenue expectations, leading to an 11.2% drop in its share price and casting a shadow over the AI-driven rally that has lifted semiconductor stocks by nearly 95% so far this year. Among the 11 main sectors of the S&P 500, healthcare and financials posted the largest percentage gains, while technology stocks recorded the steepest declines.

Chipmaker Marvell Technology rose 5.6%, while Advanced Micro Devices, Micron Technology, and Qualcomm fell between 1.9% and 4.1%. The healthcare sector was lifted by UnitedHealth, which surged 5.0% after Bank of America upgraded the stock to “buy.” The rebound in the financial index followed a sharp decline in the previous session, triggered by renewed concerns over private credit. Blackstone became the latest asset manager to restrict withdrawals from its private credit fund amid rising redemption requests, although its shares climbed 7.1% yesterday. Meanwhile, Elon Musk-led SpaceX launched its investor roadshow on Thursday ahead of its June 12 listing, with the company aiming to raise capital through a record $75 billion IPO, implying a valuation of $1.75 trillion.

Meanwhile, the US House of Representatives on Wednesday passed a proposal that would prevent President Donald Trump from continuing the war against Iran without congressional approval. In addition, the ceasefire agreement between Israel and Lebanon brokered by the US—considered a key condition for Iran’s willingness to enter into a peace deal—boosted optimism about a near-term resolution to the conflict. The decline in near-term crude oil futures reflected growing hopes that tanker traffic through the strategically vital Strait of Hormuz could soon resume.

Long-end developed market yields fell, rate hike expectations eased, and regional currencies edged higher

After three days of gains, oil prices turned lower yesterday afternoon, leading to declining yields and a weaker dollar. Macroeconomic data released yesterday were mixed, with eurozone retail sales coming in below expectations, while in the US initial jobless claims slightly exceeded forecasts, and productivity growth slowed rather than accelerated compared to preliminary estimates. Rate hike expectations eased, and bond yields declined across developed markets, with both US and German 10-year yields falling by 1–2 basis points, the former dropping below 4.5% and the latter remaining slightly above 3%. The EURUSD rose 0.1% to 1.162.

In an improving global environment by the afternoon, the forint strengthened yesterday by nearly half a percent to around 354 against the euro. Demand remained strong at government debt auctions. Bids totaling HUF 240 billion were submitted for one-year discount treasury bills, of which the debt manager accepted HUF 155 billion at an average yield of 5.53%. For the 10-year benchmark bond, incoming bids approached HUF 80 billion, with roughly half accepted at an average yield of 5.47%. Meanwhile, demand for the 2051/G 20-year green benchmark bond reached HUF 110 billion, of which HUF 50 billion was issued at an average yield of 5.42%. Reference yields published early in the afternoon by the debt manager still pointed higher, with the 10-year yield again reaching 5.5%, but in line with developed markets, yields declined by around 5 basis points by the evening.

Today's highlights

Asian indices are mixed this morning, with the Nikkei 225 falling 1.6%, while the SSEC is up 0.4%. European futures are slightly in negative territory, while Nasdaq futures are down 1%. Investors remain focused on news related to the Iran war and AI stocks.

Domestically, the statistical office will release industrial production data today, while Fitch’s rating review is due in the evening, while in the US the May labor market report could be the most noteworthy.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more