OTP Morning Brief: The US signaled it could impose additional tariffs

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

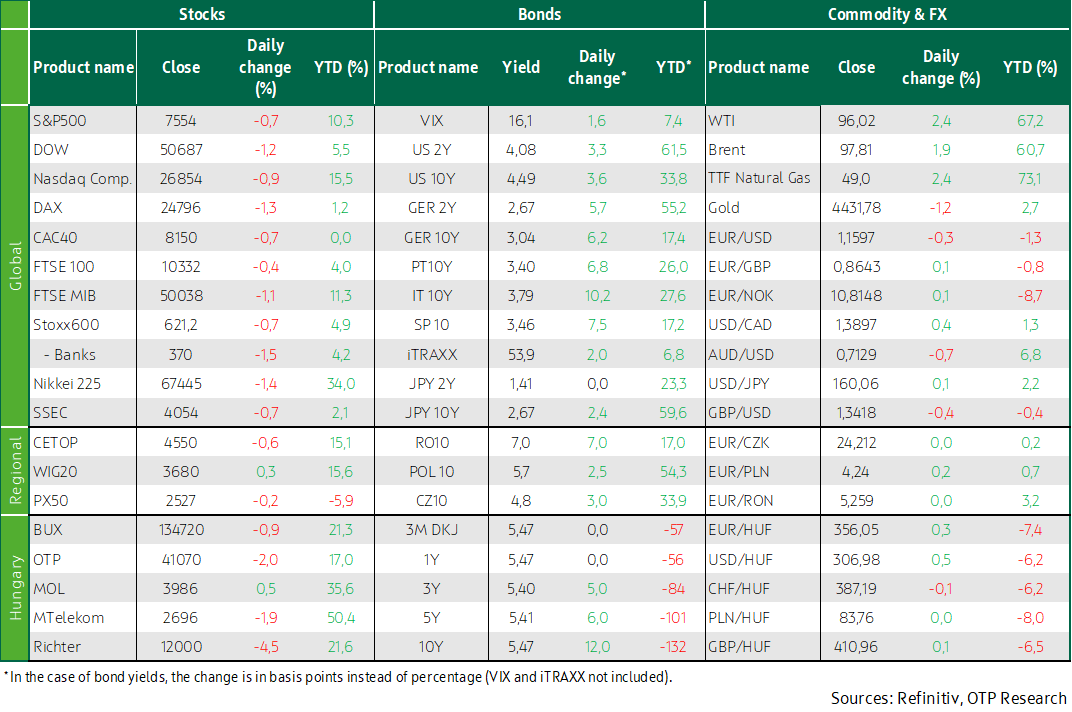

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

European indices declined yesterday; the US would impose further tariffs; uncertainty related to the Iran war persisted; euro area producer price CPI came in higher than expected in April. Overseas indices declined yesterday; oil prices rise; macro data painted a mixed picture of the economy; Broadcom reported after the close. Developed market long-term yields rise, while regional currencies weakened slightly. Today, retail sales data will be released from the euro area and Hungary, while in the US the usual weekly initial jobless claims figures are due.

European indices declined yesterday; the US would impose additional tariffs; uncertainty surrounding the Iran war persisted; euro area producer price CPI in April came in above expectations

A risk-off sentiment dominated European equity markets, fueled by geopolitical tensions in the Middle East and the rise in oil prices. The Stoxx 600 index declined by 0.7% compared to the previous close. The US Trade Representative indicated it could impose additional tariffs of up to 12.5% on around 60 trading partners, citing limited progress in curbing imports linked to forced labor. Economies potentially affected include China, the European Union, and Japan. Meanwhile, a European Union spokesperson called the planned measures unjustified and stated that the EU will fulfill the tariff commitments outlined in the joint statement by the end of June.

Investors continued to monitor developments in US–Iran tensions, after Washington reported that Tehran had launched further attacks despite the ceasefire. In an interview, US President Donald Trump stated that Iran had “agreed” not to pursue nuclear weapons, while adding that Tehran’s position could still shift. Israeli Prime Minister Benjamin Netanyahu said in an interview that there are “tactical disagreements” between him and Trump on handling the Iran conflict, and also noted that efforts are underway to develop alternative routes to bypass the Strait of Hormuz.

The financial sector was dragged lower by a 16.3% drop in the shares of Swiss private equity firm Partners Group, triggered by restrictions on capital withdrawals. Akzo Nobel fell by 17.4% after Nippon Paint and Sherwin-Williams withdrew their takeover interest, while Inditex, the Spanish retail chain that owns Zara stores, stood out with a gain of nearly 1.5% following a better-than-expected Q1 earnings report.

Euro area producer prices rose by 0.6% month-on-month in April, following a 3.4% surge in March and exceeding market expectations of 0.4%. Although the correction in energy prices helped contain the increase, underlying price pressures excluding energy strengthened, particularly for raw materials, pointing to persistent cost-side CPI pressures. On an annual basis, the indicator accelerated to 4.9%, marking a more than two-year high and suggesting that industrial inflation remains robust overall.

Regional markets showed a mixed performance: the BUX and the Czech index declined, while Poland’s WIG20 rise. Among domestic blue chips, only MOL posted gains, while the other three stocks moved lower.

Overseas indices declined yesterday; oil prices rise; macro data painted a mixed picture of the economy; Broadcom reported after the close

US equities declined yesterday, while oil prices and US Treasury yields rise amid inflation concerns linked to the escalation of the US–Iran conflict; oil prices increased following fresh US and Iranian strikes; markets increasingly priced in the possibility that the Fed could deliver another rate hike by year-end; equities were also weighed down by declines in technology and AI-related stocks, with Nvidia, Dell, Oracle, and Microsoft all posting notable losses; after the close, chip designer Broadcom reported results, posting stronger-than-expected earnings but slightly weaker revenue than forecast, and although management raised its guidance for the next quarter, the negative market sentiment led investors to focus on the downside, pushing the stock lower following the release.

US macro data continue to paint a resilient yet increasingly complex picture of the economy: a 4.8% rise in factory orders and a climb in the services PMI to 54.5 both signal that demand remains robust, supported in part by front-loaded purchases and an acceleration in services activity; however, the composition of growth is uneven, as expansion in manufacturing has been driven largely by transportation equipment, particularly aircraft orders, while in services employment continues to weaken, pointing to greater corporate caution; at the same time, price pressures are strengthening, primarily through rising energy costs, indicating persistent CPI risks; overall, growth momentum appears stable in the short term, but the combination of a softening labor market and elevated inflation continues to pose challenges for monetary policy.

According to ADP data, the labor market strengthened modestly in May: the increase of 122k slightly exceeded expectations of a 117k gain and the previous month’s 105k rise, yet it still points to relatively subdued momentum in a historical context; the composition of growth improved, driven primarily by service sectors, while the information and materials segments underperformed; wage dynamics remained stable without meaningful acceleration, suggesting that labor market tightness is gradually easing, as firms continue to follow a cautious hiring approach.

The Fed’s Beige Book yesterday painted a mixed picture of the economy: growth persisted across most regions, but increasingly concentrated among higher-income groups, while lower-income households continued to be heavily burdened by elevated prices; the report highlighted that consumption is becoming more polarized by income, with middle-income households turning more cautious and spending more selectively; alongside strengthening CPI pressures driven by the Iran conflict, price increases continued at a “moderate to strong pace,” as businesses and consumers adjusted in different ways; meanwhile, the labor market overall stagnated, with little meaningful change observed in the majority of the Fed’s 12 districts.

Developed market long-term yields rise, while regional currencies weakened slightly

Tensions in the Middle East rise, with oil prices up by 2–3%, once again approaching the $100 level; moreover, following previously released job openings data, yesterday’s ADP report also pointed to the strength of the US labor market, leading markets to price in a Fed rate hike already this year; as a result, bond yields moved higher again, with the US 10-year yield jumping 5 basis points to 4.5% and the German 10-year rising 6 basis points to around 3.05%; the dollar strengthened, with EURUSD falling below 1.16.

Regional currencies weakened slightly, with the forint falling by 0.3% to around 356; demand was weak at the Hungarian debt agency’s six-month T-bill auction, where only HUF 21.5bn was sold versus the announced HUF 30bn, at an average yield of 5.56%; by contrast, interest was strong at switch auctions, with nearly HUF 25bn of the 2033 bond and HUF 60bn of the 2041/A issuance exchanged for papers maturing this year and next; meanwhile, benchmark yields rise by 5–10 basis points, with the 10-year yield once again approaching the 5.5% level.

Today, the Hungarian debt agency will offer one-year T-bills as well as 10- and 20-year benchmark bonds at its auctions.

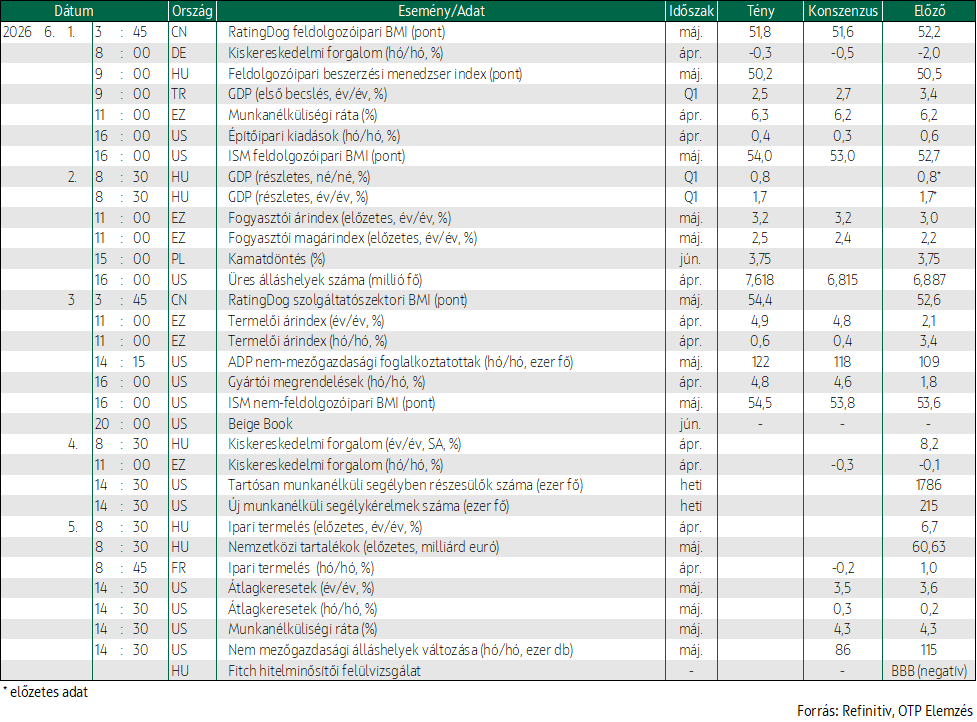

Today's highlights

Asian indices were mostly lower this morning, as investors focused on developments in the Middle East.

Today, retail sales data will be released from the euro area and Hungary, while in the US the usual weekly initial jobless claims figures will be published.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more