OTP Morning Brief: Global stock markets brush off jitters over Iran amid AI optimism

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

Equity indices in Europe and overseas alike rose on Tuesday, as the AI rally pushed Wall Street benchmarks to new highs, while this morning the Nikkei surpassed the 68,000 level for the first time in its history. No progress was made toward a settlement in the Middle East, while crude oil prices continued to edge higher. In the euro area, May inflation data were released yesterday; the headline CPI rose in line with expectations, while core CPI accelerated more than anticipated. In the US, job creation expanded more than expected in April. Developed market bond yields edged lower, while the decline in domestic yields also continued. The EUR/USD remained flat, while the EUR/HUF slipped close to the 355 level. Today, we will focus on April producer price data from the euro area, as well as the ADP labour market report, the ISM manufacturing index, and factory orders from the US. The Fed will release its latest Beige Book, and Broadcom is set to report.

The technology sector drove the pan-European Stoxx 600 index higher

European equity indices rose on Tuesday, led by the technology sector, after French chipmaker STMicroelectronics raised its revenue outlook for its data centre business, signalling strong demand driven by the expansion of artificial intelligence, and on improved prospects the company’s share price soared by 15% to its highest level since September 2000, while among its sector peers Infineon gained nearly 10% and Schneider Electric advanced by 4%.

French pharmaceutical company Abivax saw a significant move, losing more than 40% of its market value after releasing late-stage clinical trial results for its inflammatory bowel disease treatment, as investors focused on safety concerns despite the therapy’s strong efficacy; Prosus rose by 9.4% after the Financial Times reported that Tencent, the largest holding in the Dutch tech investor’s portfolio, is preparing to launch an embedded AI application for the 1.4 billion Chinese users of its WeChat messaging platform; meanwhile, British American Tobacco declined by 2.5% after highlighting weakening sales trends in both heated tobacco products and traditional cigarettes, and at the sector level, basic resources and technology outperformed, while healthcare lagged the most based on Stoxx 600 sector indices.

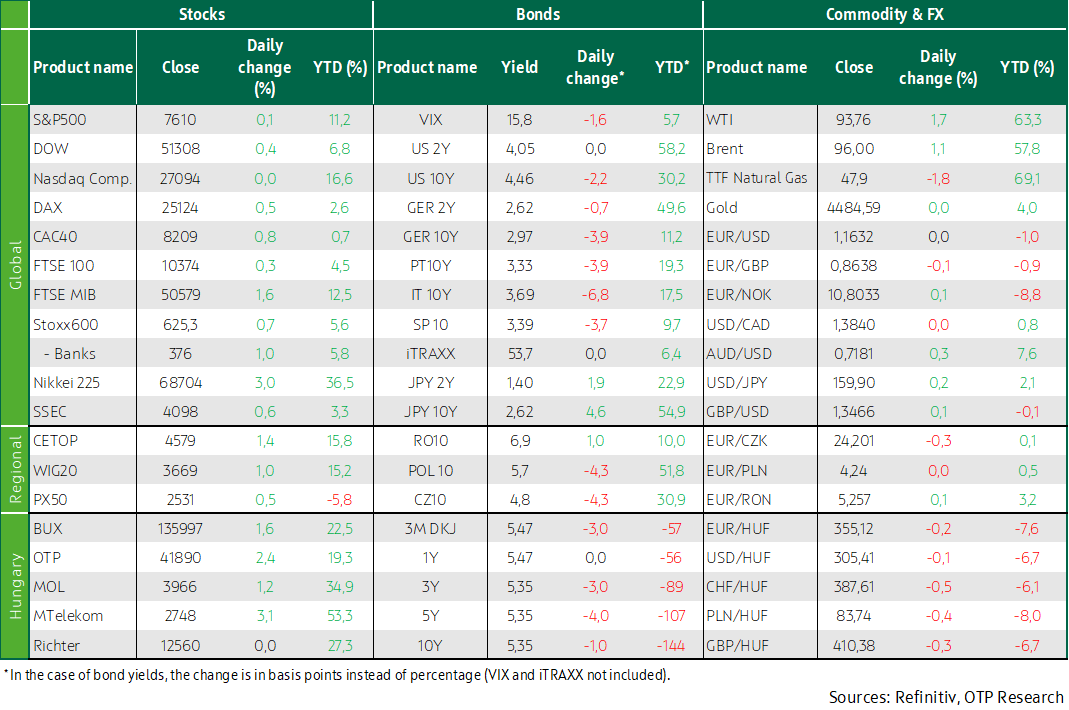

Risk appetite was also supported by tentative signs of progress in US–Iran peace talks aimed at resolving the three-month-long conflict in the Middle East, with Iranian media reporting that Tehran is currently reviewing Washington’s ceasefire proposal, although contacts with the US have reportedly been inactive for several days, and ultimately the Stoxx600 Europe rose by 0.7%, the DAX by 0.15%, while the FTSE 100 gained 0.3% and the CAC 40 closed 0.7% higher, as oil prices only edged up modestly, leaving CPI concerns unable to derail the positive market sentiment.

Although the May euro area inflation figures released yesterday raised concerns, with headline CPI accelerating to 3.2% in line with expectations, core CPI soared to 2.5% from 2.2% in April, exceeding the forecast of 2.4%, thereby reinforcing expectations that the ECB will deliver a 25 basis point rate hike at next week’s meeting, while it was also reported that a European Parliament committee approved the removal of EU import tariffs on several US goods, marking a step toward fulfilling last year’s trade agreement with the US.

Regional equity indices also rose in the favourable market environment: the BUX surged by 1.6%, the WIG20 gained 1%, and the PX advanced by 0.5%, while among Hungarian blue chips, Magyar Telekom jumped by over 3% and OTP rose by 2.4%, Mol added 1.2%, and Richter remained flat.

Detailed Q1 Hungarian GDP data released on Tuesday confirmed preliminary figures, showing growth of 0.8% quarter-on-quarter and 1.7% year-on-year, with the breakdown revealing that household consumption played a leading role in the more favorable expansion compared to previous periods, as already indicated by strong March retail sales data, while the figures also suggest that one-off effects contributed to Q1 performance, as both industrial output and retail sales showed an unusually strong rise in March following relatively subdued readings in January and February, and the weakness in goods exports observed in March and April increases the likelihood that the strong industrial production data recorded in March were driven by inventory accumulation, which significantly supported overall GDP growth.

European TTF gas prices ultimately fell by nearly 2%, closing below EUR 48/MWh.

Wall Street indices closed at new highs as enthusiasm for artificial intelligence outweighed tensions in the Middle East

US equity indices rose on Tuesday, primarily driven by optimism surrounding artificial intelligence, while oil prices only edged higher amid uncertainty over a potential agreement to resolve the Middle East conflict, and Anthropic announced on Monday that it had filed for a US initial public offering, moving ahead of its rival OpenAI in the closely watched race to enter public markets, while Google’s parent company Alphabet is also preparing to raise USD 80 billion to expand its AI infrastructure, a move that was not welcomed by investors as its share price fell by nearly 4%, and Hewlett-Packard’s earnings release published the previous day also supported strong sector performance on Wednesday, with the company itself soaring by nearly 20% in Tuesday’s trading, while chipmaker Marvell Technology, described by Nvidia’s CEO as a future trillion-dollar company, surged by 32.5%.

The Dow rose by 0.45%, the S&P 500 gained 0.1%, and the Nasdaq Composite edged higher by a few points after indices pulled back from the all-time highs reached on Monday during the first part of the trading session, while the small-cap Russell 2000 outperformed large-cap benchmarks with a 0.9% rise, and semiconductor stocks continued to rally, with the Philadelphia Semiconductor Index surging by 5.9%, while among the S&P sector indices utilities and technology posted the strongest gains, whereas the communication services sector recorded the largest decline.

According to data from the Department of Labor, the number of new US job openings—a key indicator of labour demand—rose more than expected in April, soaring to its highest level in nearly two years.

WTI rose by nearly 2% and Brent gained 1% on Tuesday amid uncertainty surrounding the resolution of the Middle East conflict.

Despite uncertainty in the Middle East, long-term yields in developed markets edged lower, with domestic yields also declining, while the forint strengthened against the euro, approaching the 355 level

Although negotiations continued, no breakthrough was achieved regarding the Iranian conflict, leaving oil prices to rise modestly by around 1%, while in the US the number of job openings unexpectedly increased, highlighting the continued strength of the labour market, and in the euro area May data released yesterday showed CPI rose to 3.2% in line with expectations, while core CPI accelerated more than anticipated to 2.5%, partly due to Easter effects, and US bond yields showed no meaningful change, with the 10-year Treasury yield remaining just below 4.5%, while in the euro area yields edged lower by a few basis points, with the 10-year German yield slipping slightly below 3%, and the EUR/USD remained unchanged at 1.163.

Detailed data from the Hungarian Central Statistical Office confirmed that GDP rose by 0.8% quarter-on-quarter and 1.7% year-on-year in Q1, with the acceleration in growth largely driven by strong consumption and rising inventories, while the forint strengthened slightly yesterday to the 355 level against the euro, alongside a modest gain in the zloty and a 0.3% rise in the Czech koruna, and at the Government Debt Management Agency’s three-month Treasury bill auction demand was moderate, with HUF 40 billion sold instead of the planned 30 billion at an average yield of 5.57%, while domestic bond yields continued to edge lower by 3–5 basis points, with the 10-year yield approaching 5.3% again.

Today's highlights

Market sentiment was mostly positive across Asian equities this morning, with the AI rally continuing to drive stock markets higher: Japanese indices surged by 2–3%, with the Nikkei surpassing the 68,000 level for the first time in its history, while Chinese and South Korean indices also traded in positive territory, albeit with more moderate gains, and the Hang Seng slipped by 0.8% in early trading, while Taiwan’s tech-heavy indices posted gains of 1–2%, and China’s Rating Dog services PMI rose to 54.4 in May based on data released this morning.

Equity index futures point to a mixed open in Europe and declines for the major US indices.

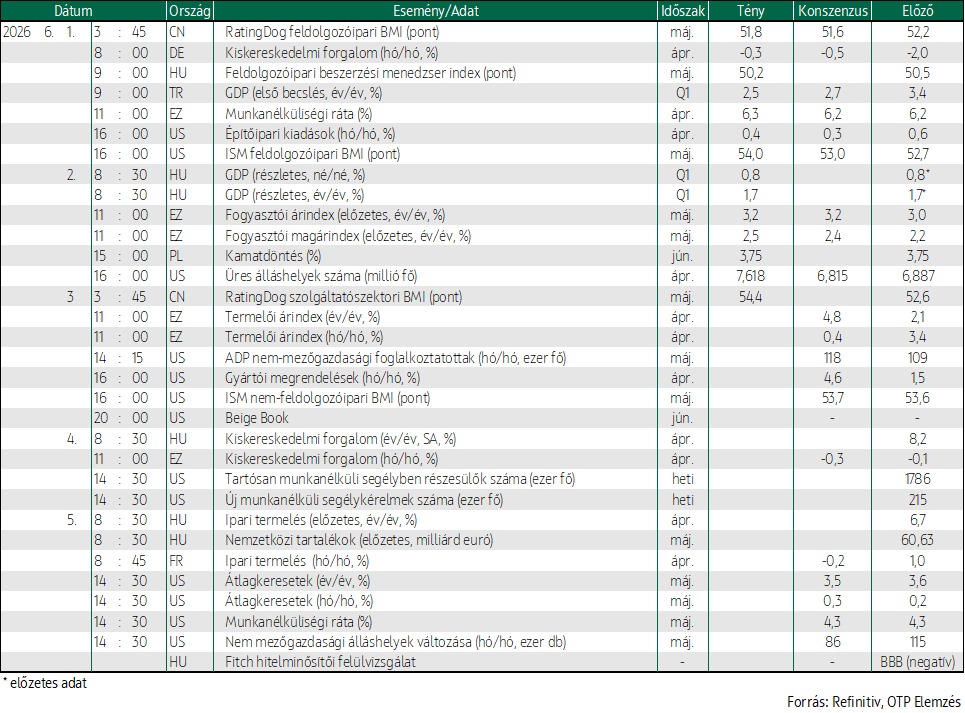

During the day, attention will focus on April producer price data from the euro area, along with ADP labour market figures, the May ISM index, and April factory orders in the US, while the Fed will also release its latest Beige Book.

Broadcom is set to release its earnings report after market close today.

Today, the Government Debt Management Agency will offer six-month Treasury bills with a planned issuance of HUF 30 billion, and at the switch auction investors can acquire HUF 15 billion each of the 2033/C and 2041/A bonds in exchange for securities maturing this year and next.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more