OTP Morning Brief: Global equities started the week on a negative note as the situation in the Middle East deteriorated

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

In Europe, major indices closed Monday in negative territory, primarily due to unfavorable news from the Middle East. Gas and oil prices also rose by around 5%. Goldman Sachs raised its price target for the Stoxx 600, while software companies also delivered strong performance. The negative sentiment also spread to regional markets, with the Czech, Polish, and Hungarian exchanges all closing lower on Monday. In the US, the tech sector continues to drive the market, led primarily by software companies. All three US indices moved higher, with the tech-heavy Nasdaq delivering the strongest performance. Among the S&P 500 sectors, only energy managed to rise alongside technology. Rising oil prices fueled concerns about CPI, pushing developed market yields higher. The forint weakened by around 0.5%. Today, we will be watching the Polish rate decision in the region, June CPI preliminary data from Europe, and job openings in the US.

Europe closed lower due to negative news from the Middle East

European equity markets declined on Monday as escalating tensions in the Middle East significantly reduced the likelihood of a near-term resolution to the conflict surrounding Iran. Investors also assessed takeover developments involving the UK’s easyJet.

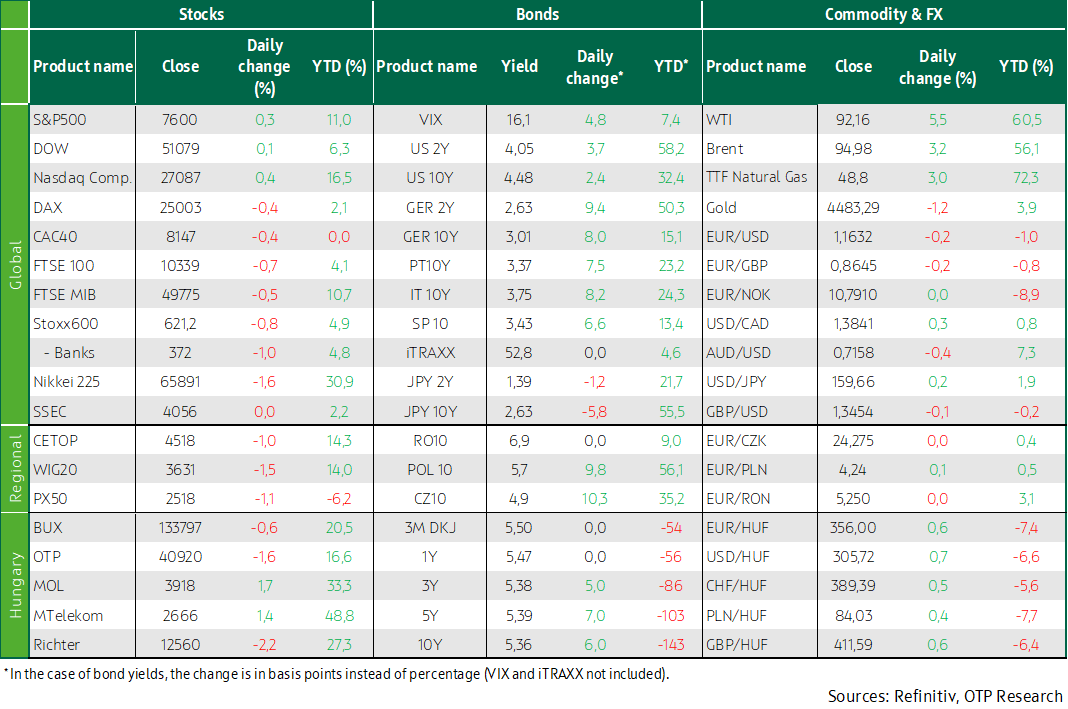

The pan-European STOXX 600 index closed down 0.8% at 621.24 at the end of a volatile trading session, marking its lowest level in more than a week. Trading already began on a negative note after the US and Iran confirmed that an armed incident had taken place between them over the weekend. Losses deepened after Iran’s Tasnim news agency reported that Tehran had suspended talks with Washington following attacks targeting Lebanon. According to Tasnim, Iran and its allies – the so-called “axis of resistance” – are also considering restricting traffic through the Strait of Hormuz, as well as other key maritime routes, including the Bab el-Mandeb Strait. Oil prices surged by more than 6.5%, further amplifying concerns about Europe’s heavy reliance on energy imports.

Most sectors closed in negative territory, with energy stocks standing out as an exception, rising by 1.7%.

Despite the uncertain environment, analysts say corporate earnings reports have so far shown greater resilience than expected. In light of this, Goldman Sachs raised its 12-month target for the STOXX 600 to 660.

Among corporate developments, EasyJet’s share price soared by 10% after investment firm Castlelake indicated it is considering the possibility of a takeover bid, although the British low-cost carrier described the timing as “highly opportunistic” in light of the impact of the Iran conflict, while gains in US technology stocks also lifted their European peers, with SAP, Europe’s largest software company, climbing 8.1%, and Sage, Dassault Systemes, Nemetschek, and Temenos each posting increases of 7–8%.

Among the notable movers, Wise stood out, with its share price plunging 8% after it emerged that the Brussels prosecutor is investigating the digital money transfer company over suspicious transactions worth around €500 million.

The European TTF gas price rose by 5% and closed above EUR 48.

Regional markets were not immune to the negative sentiment either, with the Czech PX and Polish WIG both falling by more than 1%, while Hungary’s BUX closed 0.6% lower on the day, as domestic blue chips showed mixed performance, with OTP and Richter declining, while Magyar Telekom and Mol managed to rise.

US equity markets continue to rise, driven by AI and software companies

US equity markets closed with modest gains on Monday, supported by outperformance in the technology sector, with the Nasdaq (+0.42%) and the S&P 500 (+0.26%) both rising to new all-time highs, while the Dow Jones (+0.09%) posted only a limited increase, and among S&P 500 sectors, only technology and energy finished higher, with utilities emerging as the biggest laggard.

Market sentiment continues to be shaped by geopolitical developments in the Middle East, and although US–Iran negotiations are formally ongoing, tensions between the parties persist, while the market viewed it positively that near-term escalation risks have eased following indications from the US that an Israeli ground offensive against Beirut is not expected.

The day’s gains were once again led by the technology sector (+2.5%), primarily driven by Nvidia’s advance (+6.3%), after the company unveiled a new AI chip specifically designed for personal computers, with the development – in partnership with Microsoft – expected to accelerate AI integration in the PC market and support demand across a broader segment, while Microsoft shares rose by 2.3%.

The semiconductor sector delivered mixed performance, with Micron (+6.6%) rising to a record level above $1,000, while Qualcomm (-8.8%) and Intel (-4.7%) declined, and the SOX index tracking the sector closed overall 1.1% higher.

The rally in the software sector also continued, with ServiceNow (+9.2%) and IBM (+7.6%) both posting strong gains, partly supported by the market narrative that AI is not replacing but rather complementing and enhancing software services.

Hewlett-Packard reported stronger-than-expected earnings, sending its shares up by more than 9%.

WTI rose by nearly 6% and Brent by around 5% yesterday due to intensifying tensions in the Middle East.

Strengthening CPI concerns pushed yields higher again and weighed on the forint

The rise in oil prices once again fueled CPI concerns, pushing yields higher on bond markets after last week’s decline, with the US 10-year yield increasing by 3 basis points yesterday to approach 4.5%, while in Europe long-term yields moved even higher by 5–10 basis points, with the German 10-year once again nearing 3%, and the dollar strengthened against the euro by 0.3%, with EURUSD trading around 1.1625.

The Czech koruna was flat yesterday, the zloty weakened by 0.1%, while the forint depreciated by nearly 0.5% from last week’s four-year high of 353, approaching the 356 level, as domestic benchmark yields moved higher from four-year lows by around 5 basis points, with the long end of the yield curve standing near 5.35%, and at yesterday’s T-bill switch auction, HUF 22 billion worth of government securities changed hands amid solid demand.

Today, the Government Debt Management Agency (ÁKK) will offer HUF 30 billion worth of three-month T-bills.

Today's highlights

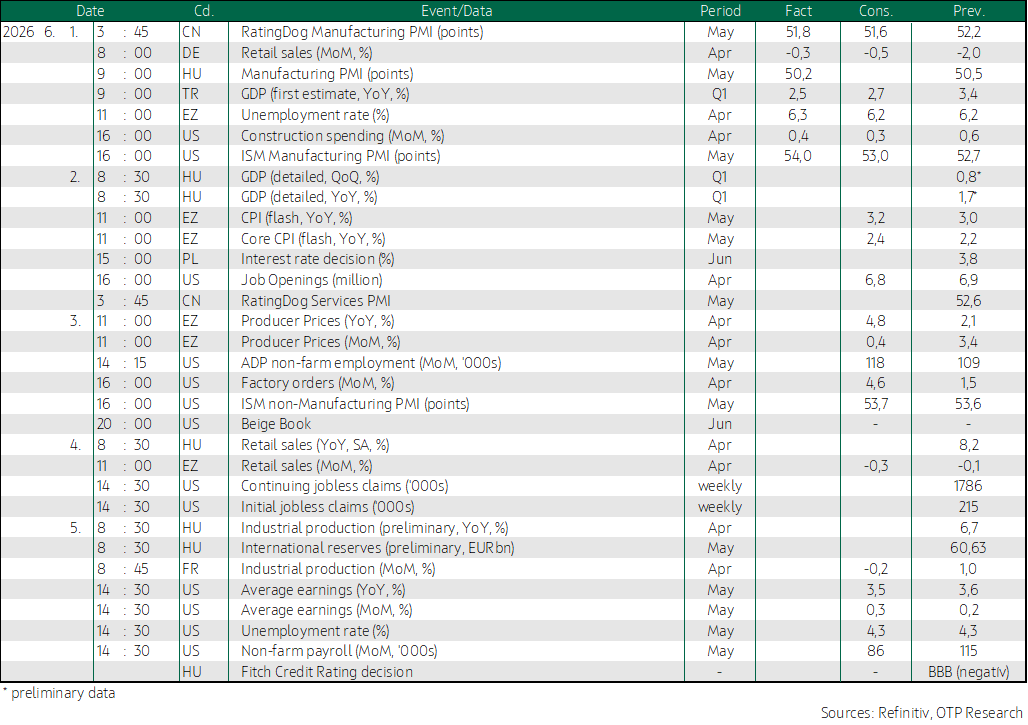

By this morning, a significant sell-off also unfolded across Asian markets, with both the Nikkei and South Korea’s Kospi down by more than 1.5%, driven partly by rising concerns related to the situation in Iran and partly by a broader wave of profit-taking in chipmakers; today brings the Polish rate decision, where the market expects no change, while the euro area will release its preliminary June CPI reading, with both headline and core measures expected to show acceleration, and in Hungary the detailed Q1 GDP data will be published, offering insight into what drove the stronger-than-expected growth and whether components beyond consumption also contributed on the demand side, while in the US the focus will be on job openings data.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more