OTP Morning Brief: Investor sentiment continued to be dominated by developments in the Middle East

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

During the past week, news on the war sent mixed signals, and although a draft to extend the ceasefire surfaced on Thursday, reports ultimately pointed to military action rather than its finalization. European markets closed in positive territory both on Friday and for the month of May, while CPI pressures in key eurozone economies rose, albeit to a lesser extent than expected. In Romania, a residential building was hit, reportedly by a stray Russian drone. In Hungary, foreign trade performance continued to deteriorate, but the BUX delivered a strong performance, supported by the agreement on previously frozen EU funds. In the US, the major indices continued to rise, while fears of further rate hikes eased. China’s PMI declined less than expected, while Asian equity markets delivered a solid performance. This week, attention will be on Hungary’s detailed GDP data, eurozone CPI, and the US labor market report.

Investor sentiment continued to be driven primarily by developments in the Middle East

Throughout the week, sentiment was shaped by even more turbulent-than-usual news from the Middle Eastern conflict. The previously agreed ceasefire came under threat after the US carried out strikes on missile sites in southern Iran, while Iran targeted a US base in Kuwait. This was followed on Thursday by a leaked report suggesting that the draft to extend the ceasefire was awaiting only Trump’s signature, which helped calm markets toward the end of the week. However, on Saturday, an Iranian vessel attempted to pass through a US-enforced blockade and was struck after multiple warnings. Meanwhile, on another front of the conflict, Israel’s Prime Minister Benjamin Netanyahu on Sunday ordered troops to advance further into Lebanese territory in fighting against the Iran-backed Hezbollah armed group, despite a ceasefire having been announced more than six weeks earlier. Finally, according to Monday morning reports, the US stated that it had targeted Iranian military assets over the weekend, to which Iran’s Revolutionary Guard responded by striking a US base.

European markets closed May in positive territory, a drone struck a residential building in Romania, and Hungary’s trade balance deteriorated

European equities edged higher on Friday, closing the month with gains as investors priced in more favorable developments from the Middle East, with the pan-European STOXX 600 index rising 0.1%, resulting in a 1.3% weekly advance and a 2.4% increase over the month, while among major indices the DAX led with a 3.3% gain and most others also moved higher, and looking at Friday’s STOXX 600 performance, airline stocks—particularly sensitive to energy prices and geopolitical turbulence—performed well, with Lufthansa and Air France both climbing more than 2%, while the consumer discretionary sector, including luxury goods, rose by 1%, and the defense sector was also among the stronger performers with a 0.7% rise, supported by reports that a Russian drone struck a residential building in Romania during an assault on neighboring Ukraine, prompting NATO to accuse Moscow of reckless behavior and state it would “defend every inch of allied territory,” while at the individual stock level CTS Eventim stood out, with its share price surging 10.7% after the German ticketing company reported a 23% revenue increase in Q1 2026 driven by strong demand for live entertainment.

In terms of data, CPI in the eurozone’s four largest economies remained above the European Central Bank’s 2% target for a third consecutive month in May, although—excluding Italy—the figures came in below analysts’ expectations, as fuel price increases driven by the war involving Iran began to feed through into broader price levels, and readings from France (2.4% year-on-year), Italy (3.2%), Spain (3.2%), and Germany (2.6%) are likely to reinforce the case for an ECB rate hike next month, while also heightening concerns that elevated inflation could become entrenched across the eurozone.

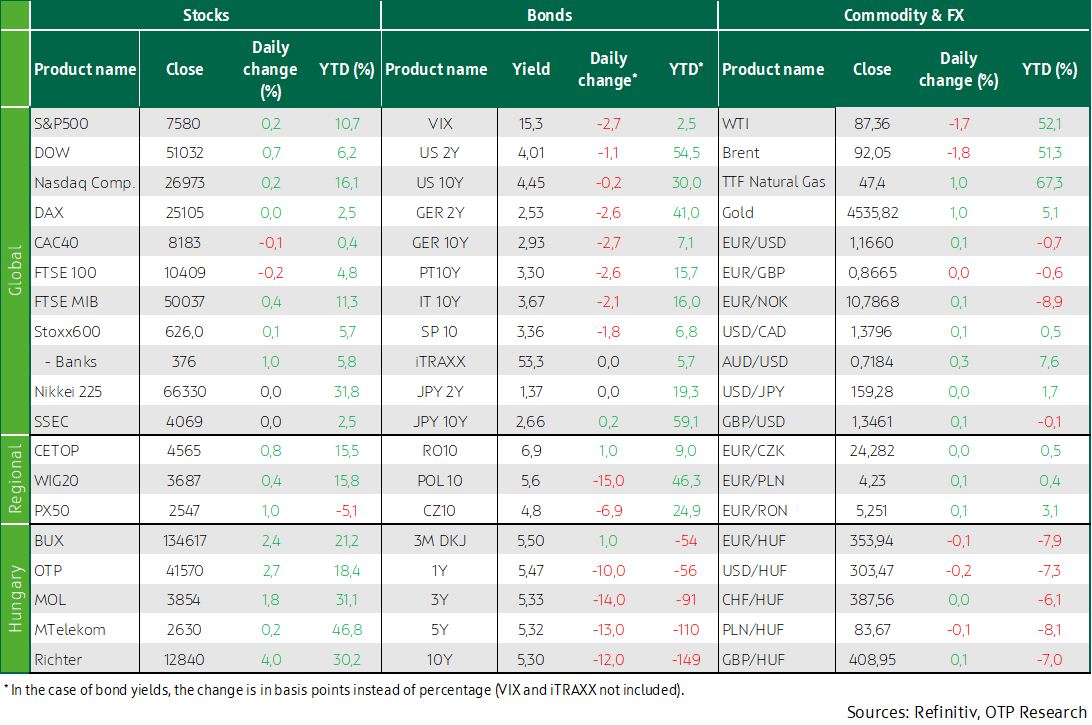

CEE markets delivered a particularly strong performance on Friday, with the WIG 20 rising 0.4%, the PX50 gaining 1%, and the BUX climbing 2.4%, primarily supported by a 2.7% surge in OTP, while Richter advanced 4.0% and MOL investors recorded gains of 1.8%, allowing the BUX to close the month with a 0.6% increase overall, where Magyar Telekom posted the strongest performance with a 7.1% rise, while the other three domestic blue chips ended in negative territory, and according to Hungary’s Central Statistical Office, the goods trade surplus stood at EUR 104 million in April, marking a deterioration of EUR 1,045 million compared to a year earlier, as export volumes declined by 4.9% year-on-year while imports rose by 10%, while S&P left Hungary’s sovereign credit rating unchanged at BBB- with a negative outlook.

US indices, which continue to hit record highs, closed May with strong gains

US indices also closed higher on Friday, with the S&P and Nasdaq both rising 0.2% and the Dow gaining 0.7%, allowing all three benchmarks to extend their previously reached record levels at the end of another positive week, while for May as a whole they posted gains of 5.1%, 9.3%, and 2.8%, respectively, and looking at Friday’s moves, the technology sector climbed 1.9%, driven primarily by strength in semiconductor stocks, while Dell shares surged 32.8% after the company raised its full-year profit and revenue guidance on Thursday, with peers also performing strongly as Hewlett Packard Enterprise and Super Micro Computer rose 12.6% and 11.6%, respectively, and Microsoft advanced 5.4%, while the software services index gained more than 6%, fully recovering losses seen since late January when concerns over disruption caused by AI weighed on the sector, however the S&P 500 communication services sector ended in negative territory following a 2.5% decline in Alphabet, and consumer staples stocks also underperformed, with Costco falling 3.9% and Walmart declining 2.6%, while the S&P automotive index moved lower after reports suggested that under the Trump administration vehicles produced in North America would need at least 82% regional content to qualify for preferential treatment under the US–Mexico–Canada agreement, pushing General Motors shares down 1.3% and US-listed Stellantis shares 2.7% lower, while several Fed policymakers have recently adopted a more hawkish tone.

Rate hike fears eased in the US, and an agreement was reached on previously frozen EU funds

Markets continued to be driven by news related to the war involving Iran, but optimism fueled by hopes of a swift agreement, which emerged two weeks earlier, remained the dominant theme, while oil prices declined sharply at the beginning of the week and then continued to ease gradually, with Brent falling from above USD 110 two weeks earlier and over USD 100 at the end of last week to around USD 90, and incoming macroeconomic data in the US pointed to slower-than-expected growth alongside more moderate CPI pressures, as Q1 GDP growth was revised down to an annualized 1.6% from 2%, while the April PCE price index, the Federal Reserve’s preferred inflation gauge, came in below expectations both in headline and core terms, yet still indicated price increases of around 3–4%, remaining meaningfully above target, while in Europe, business surveys showed easing inflation expectations alongside a slight improvement in both business and consumer confidence, and inflation data from larger member states suggested that euro area CPI may have risen to around 3.1% in May, falling short of the 3.3% forecast, as rate hike fears eased, with markets pricing roughly a 50% probability that the Fed will deliver at least one rate increase this year and around 66% next year, although on Friday Vice Chair for Supervision Michelle Bowman noted that a persistent energy shock could shift the direction of monetary policy, while markets expect the ECB to implement two 25 basis point hikes this year and one more next year, and bond yields declined significantly from prior peaks, with the US 10-year yield dropping from a recent high near 4.7% and 4.55% the previous Friday to below 4.45%, while the German 10-year yield fell from a 15-year peak of around 3.2% and 3.05% the previous Friday to below 2.95%, and amid the improved global sentiment the euro strengthened slightly against the dollar, with EURUSD rising from 1.16 to above 1.165.

In Hungary, attention was focused on the talks between Prime Minister Péter Magyar and Ursula von der Leyen, with an agreement reached on Friday to unlock previously frozen EU funds, enabling the use of EUR 16.4 billion, which is expected to support domestic growth, reduce the budget deficit and financing needs, and strengthen confidence in the Hungarian economy, while supported by the favorable external environment and positive domestic developments, the forint appreciated to levels not seen since 2021, strengthening to 353 against the euro, and bond yields continued to decline, with government bond yields falling to 5.3% by Friday, around 200 basis points below their local peak in March.

Today's highlights

Despite troubling headlines, sentiment across Asian markets was mostly positive, with South Korea’s equity market reaching a fresh all-time high on Monday as the Kospi index rose 1.3%, supported by a more than 3% gain in Samsung Electronics, whose shares also hit a record level, while Japan’s Nikkei edged up 0.2%, Hong Kong’s Hang Seng advanced 0.7%, and China’s SSEC increased by 0.1%.

China’s Caixin manufacturing PMI edged down to 51.8 in May 2026 from April’s more than five-year high of 52.2, while still exceeding expectations of 51.4, as growth in new orders and output slowed but remained solid overall, while export orders declined slightly, production continued to expand at a strong pace, employment shifted into a mild contraction, and CPI pressures eased.

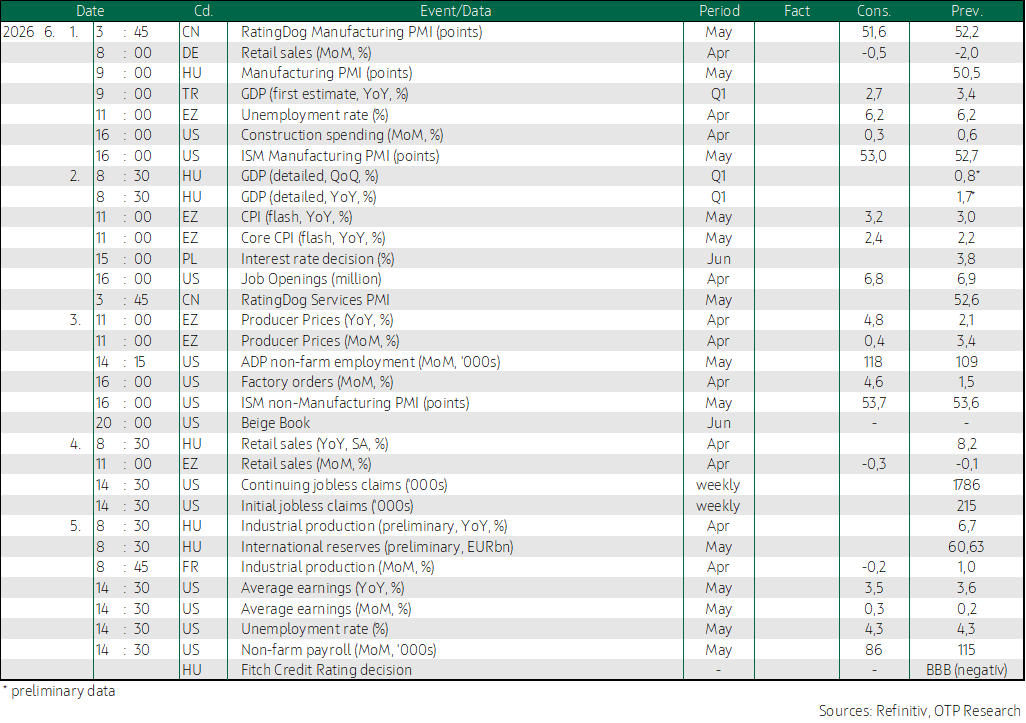

Today, Hungary will release manufacturing PMI data, Germany is set to publish retail sales figures, while in the US manufacturing PMI will be released alongside construction spending data, and later this week more detailed insights into Hungary’s 1.7% GDP growth will be available, while in the euro area, beyond labor market and confidence indicators, the May CPI reading will be the main focus, with data from major economies this week pointing to a rise in headline CPI to 3.2% year-on-year and core CPI to 2.4%, and according to our aggregated estimates—despite the war involving Iran—inflation likely showed only a moderate increase from 3.0% to 3.3%, a level that could be consistent with the ECB’s target under normal conditions but leaves little buffer against adverse shocks, while markets are now pricing in three rate hikes from the European Central Bank within a year, starting as early as June.

The latest labor market report from the US is due on Friday, with the key question being whether the momentum in employment growth was sustained in May, as in April nonfarm payrolls increased by a stronger-than-expected 115 thousand, reinforcing the narrative that the sharp decline seen in February was driven by one-off factors and that the labor market remains resilient, while the market consensus for the May report points to job growth approaching 100 thousand alongside a stable unemployment rate, and a robust labor market allows the Fed to prioritize price stability within its dual mandate when making policy decisions, which currently does not support rate cuts at all, with market pricing indicating no rate reductions this year and assigning nearly a 50% probability to at least one rate hike in 2026 and around 66% next year.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more