OTP Morning Brief: The ceasefire in the Middle East has been extended

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

The ceasefire between the US and Iran has been extended for 60 days. However, this did not shield European stock markets from a decline. According to the ECB minutes, the Governing Council is considering a rate hike, while overall European sentiment has slightly improved. The domestic stock market edged slightly lower, while employment conditions continued to deteriorate. In the US, the S&P and Nasdaq closed at record highs. US data pointed to lower-than-expected CPI pressures and slower growth. Yields declined, while oil prices remained flat. Asian markets also continued to set new records. Today, attention will be on S&P’s credit rating decision.

The US and Iran agreed to extend the ceasefire by sixty days

The US and Iran agreed on Thursday to extend the ceasefire by 60 days, although the deal still awaits final approval from President Donald Trump. The development came after Iran targeted a US air base in Kuwait and following US strikes, which Washington described as a preemptive move against an Iranian drone operation. According to four sources familiar with the matter, the parties reached an agreement on the extension in a memorandum of understanding. The deal also states that the future of Iran’s highly enriched uranium stockpile will be the first issue to be addressed during the 60-day period. The White House declined to comment on the matter.

European equities declined on Thursday, the ECB’s Governing Council considered a rate hike, while domestic employment decreased

European equities declined on Thursday amid global uncertainties, although losses were partly capped by late-session news on the US–Iran ceasefire. Among the major indices, the FTSE 100 had the weakest performance, falling 0.8%, while the DAX slipped 0.3% and the CAC 40 edged down 0.2%, leaving the pan-European Stoxx 600 0.5% lower. Financials led the downturn, with banking and insurance stocks dropping 1.0% and 1.9%, respectively. Meanwhile, shares of French semiconductor materials producer Soitec soared 24.6% after its annual revenue beat market expectations. Within the sector, Infineon and STMicroelectronics also posted gains of 4.4% and 3.2%, respectively. Defense stocks moved higher as well: Renk surged 5.4%, Rheinmetall rose 4.1%, and Saab jumped 7.4% after Canada and Norway signaled plans to strike agreements with European firms.

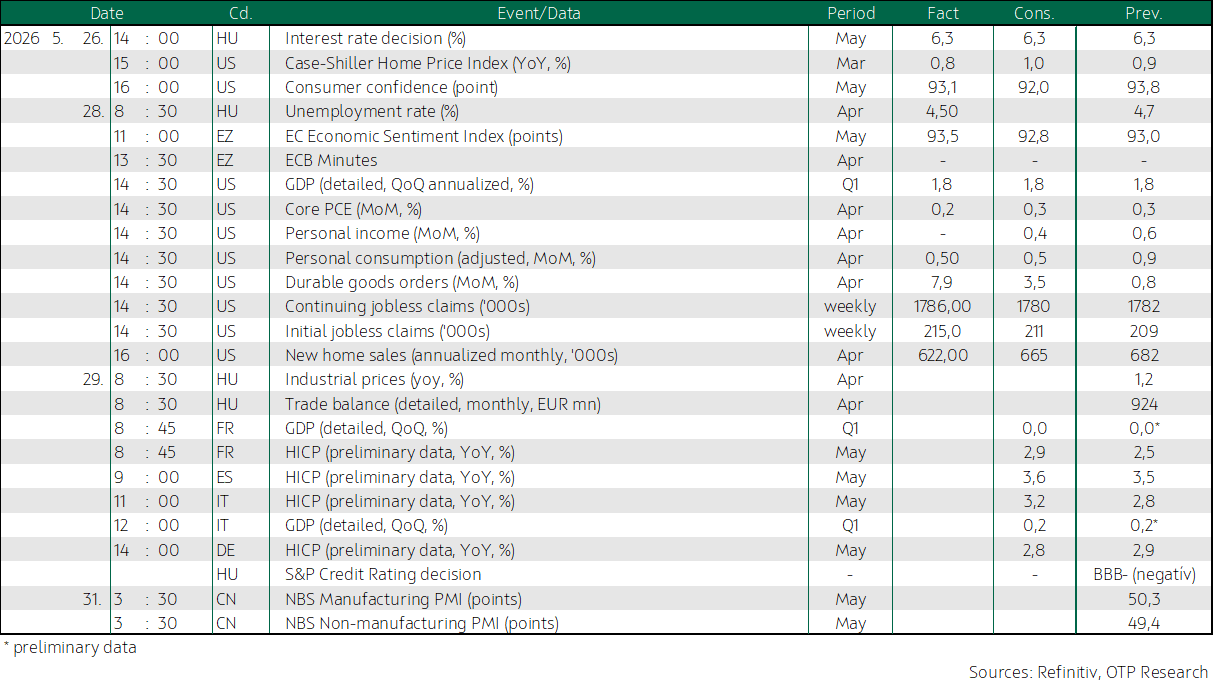

According to the minutes of the ECB’s April meeting, the Governing Council left rates unchanged after careful consideration, as persistently high inflation makes it increasingly difficult to ignore the shock caused by energy prices, with several policymakers already leaning toward a rate hike. The European Commission’s sentiment index rose by 0.5 points to 93.5 in May, exceeding market expectations that had pointed to a decline, although it remained below the key 100 threshold, signaling a still negative outlook.

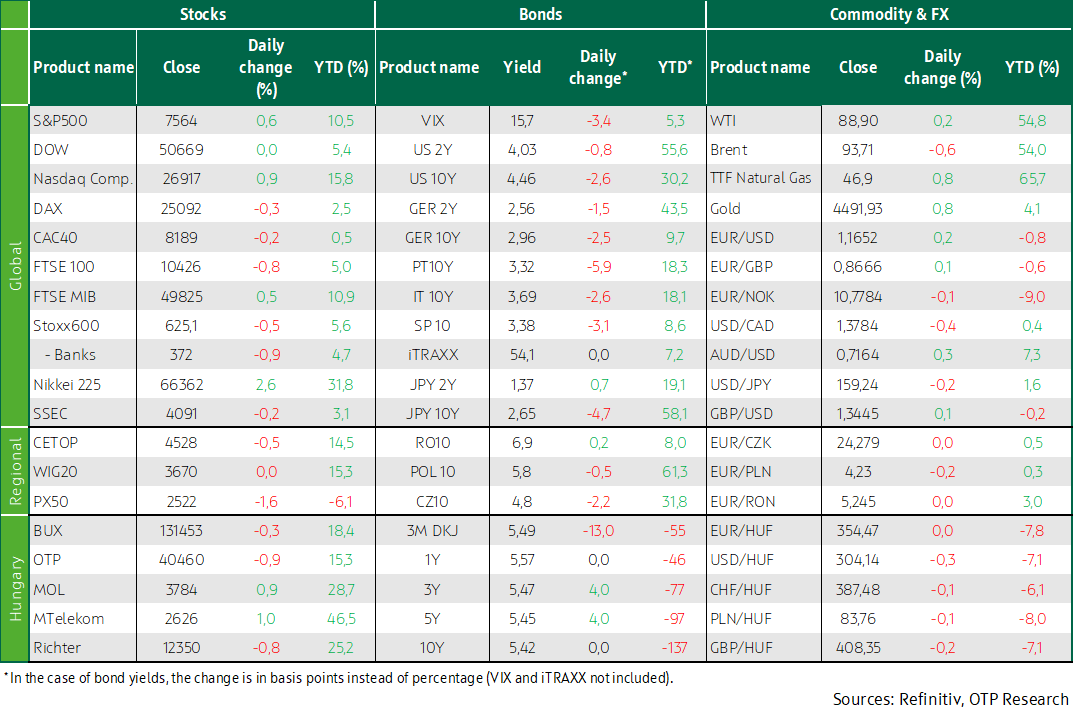

Regional indices followed a similar trajectory to their Western peers: the PX 50 fell 1.6% and the BUX declined 0.3%, while the WIG 20 remained flat. The domestic market was mainly weighed down by a 0.9% drop in OTP, while Mol gained 0.9% and Magyar Telekom rose 1.0%. Based on domestic employment data, employment continued to decline, falling by 55,000 in the February–April period compared to the same period a year earlier, while the unemployment rate stood at 4.5%.

US equities at record highs, Q1 GDP revised lower, CPI pressures increased

News of significant de-escalation propelled the S&P and Nasdaq to record highs, with the former rising 0.6% and the latter adding 0.9%, while the Dow showed little movement relative to its opening level. The S&P 500 healthcare index posted notable gains, supported by a 4% advance in Eli Lilly after CVS Health announced it would reinstate coverage for the drugmaker’s weight-loss injection, Zepbound, and add its newly approved obesity pill, Foundayo. Technology stocks also moved higher, with Microsoft climbing 3.5% following a report by The Information that the company is set to unveil a new coding model next week. Shares of Marvell Technology rose 3% after UBS lifted its price target from $195 to $230. Meanwhile, Anthropic, the firm behind Claude AI, raised $65 billion in fresh capital at a valuation of nearly $965 billion, overtaking OpenAI as it strengthens its position in the AI race through rapid growth, strong demand, and IPO plans.

The picture was also nuanced by a series of data releases: US core PCE, a key measure of inflation, rose 0.2% month-on-month in April, missing analysts’ expectations of 0.3%, while on an annual basis it still increased at the fastest pace in three years, by 3.3%, driven by energy prices that surged due to the Iran-related conflict. Fresh GDP data showed that the US economy grew at a slower-than-previously-estimated annual rate of 1.6% in Q1, reflecting downward revisions to consumption and inventory investment, while growth is increasingly being driven by AI-related spending. Initial jobless claims in the US rose to 215,000 in the week ending May 23 from 210,000 previously, though the figure came in below expectations. New orders for durable goods soared by 7.9% month-on-month in April 2026, following an upwardly revised 1.3% increase in the previous month, significantly exceeding expectations of 3.5%, driven by a 21.5% surge in demand for transportation equipment. Monthly growth in both household consumption and income slowed in April, with the former at 0.5% and the latter flat at 0%, both falling well short of expectations.

Brent crude futures stood at $93.7 per barrel, while WTI was at $88.9, both remaining largely unchanged from Wednesday’s levels.

Bond yields declined in both Europe and overseas, while the forint strengthened to 354 against the euro

According to the European business sentiment survey, inflation expectations eased, while both business and consumer confidence showed a slight improvement. US data pointed to lower-than-expected CPI pressures and slower growth. Bond yields declined both overseas and in Europe, with the US 10-year yield falling to around 4.45% and the German equivalent to 2.95%, down 2–3 basis points from Wednesday’s levels. The dollar weakened slightly against the euro, with EURUSD at 1.165.

Among regional currencies, the Czech koruna remained unchanged against the euro, while the zloty and the forint strengthened slightly, with EURHUF at 354. In the domestic government bond market, following the significant decline in yields in recent days, rates essentially stagnated near a four-year low of around 5.5%, while the 10-year yield stood just above 5.4%. Demand at yesterday’s bond auction by the Government Debt Management Agency (ÁKK) was solid, though no longer overwhelming, with more than HUF 150 billion of three-, five-, and ten-year bonds sold at an average yield of around 5.4%.

Today's highlights

Positive sentiment also carried over to Asian markets, with both the Nikkei and Kospi reaching record highs, gaining 2.6% and 3.3%, respectively, while the Hang Seng rose by 1.0%. In contrast, China’s Shanghai Composite edged down 0.2%. Data from Japan showed that Tokyo core inflation slowed to 1.3% in May, remaining below the Bank of Japan’s 2% target and reinforcing expectations that the central bank will proceed cautiously with further monetary normalization.

Today, the focus domestically will be on S&P’s credit rating review, alongside data releases on industrial producer prices and foreign trade. In addition, several European countries will publish GDP and CPI figures.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more