OTP Morning Brief: European new car sales continued to rise

Related content

OTP Morning Brief: Crude oil prices plunged sharply as the Middle East conflict eased

The first trading day of the week brought modest gains to the major European stock markets, as sectors benefiting from the easing of the Middle East conflict offset declines in the technology and energy sectors. Stock markets across the CEE region also moved higher, with the BUX gaining 0.7%. Wall Street indices closed mixed with minor moves, as investors turned their attention to the Fed's upcoming interest rate decision later this week and earnings reports from major technology companies. WTI crude futures fell by more than 7%, while Brent crude declined by over 8%. Developed-market bond yields declined as easing concerns over CPI, driven by lower oil prices, boosted demand for fixed-income assets. Domestic long-term bond yields also moved markedly lower. The EURHUF exchange rate is trading around the 360 level. Today marks the start of the Fed's two-day rate-setting meeting, while the earnings season continues with reports from several major companies.

OTP Morning Brief: Airstrikes eased in the Middle East

European indices advanced on Friday, allowing them to end the week in positive territory once again. The July PMI data painted a positive picture of the eurozone outlook, although Trump imposed new tariffs, including measures affecting Europe. The BUX declined on Friday, but still ended the week in positive territory. According to the HCSO, employment declined while unemployment increased. Airstrikes between Iran and neighboring countries eased over the weekend. This pushed oil prices back below $100 per barrel. The S&P declined on Friday and posted a loss for the week as a whole. The composite PMI also increased in the US. Developed market government bond yields retreated from their local highs. Hungarian bond yields increased, while the forint strengthened slightly. Q2 GDP data will be released this week for Hungary, the eurozone, and the US. In addition, investors will be watching eurozone and US CPI data, as well as the Fed's interest rate decision.

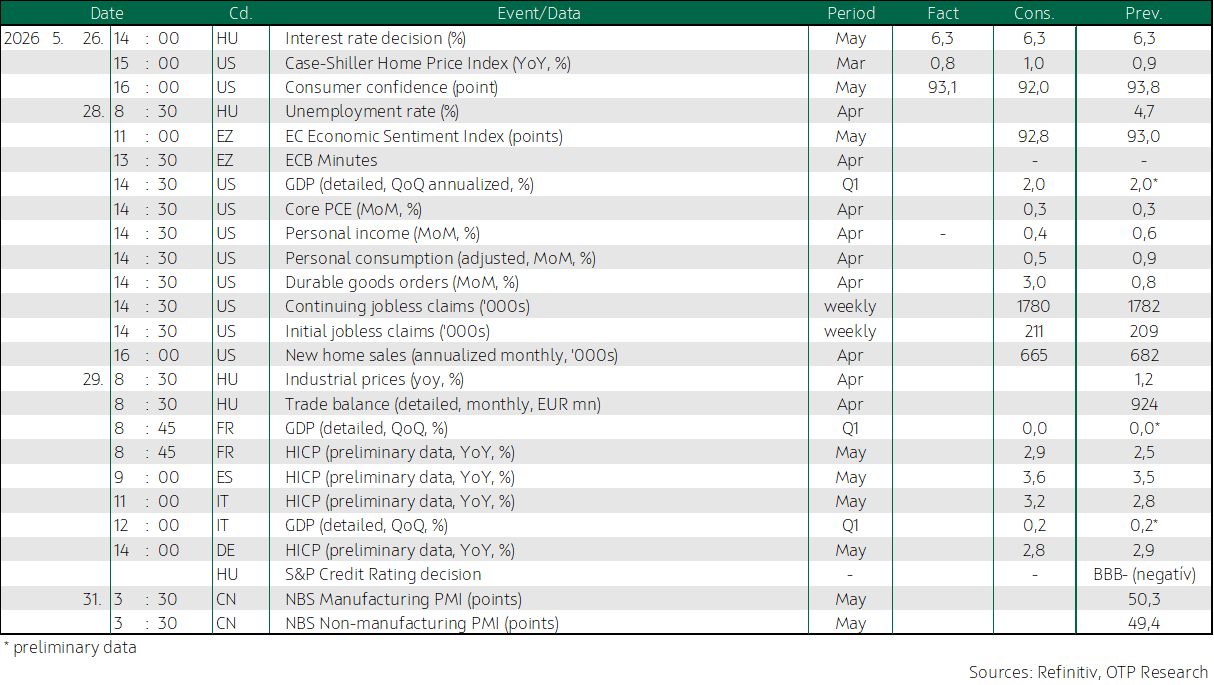

Western European indices closed mixed as uncertainty over the Iran conflict persists, while new car sales in the EU continued to rise.US indices mostly moved higher; Tuesday’s momentum in semiconductor stocks eased somewhat; Meta shares rose. Developed market long-term yields barely moved, while Hungarian yields fell; there was no clear direction in regional FX markets. Today brings the European Commission’s economic sentiment index and the minutes of the ECB’s latest rate-setting meeting. In the US, releases include CPI, GDP, housing, household consumption and income, as well as order book data. Hungary will publish unemployment figures.

Western European indices closed mixed as uncertainty over the Iran conflict persists, while European new car sales continued to rise

Western European equity markets closed mixed on Wednesday, as investors assessed military developments in the Middle East and declining oil prices. Market sentiment continued to be shaped by the evolution of the Iran conflict. Earlier in the week, progress in peace talks was reported, however tensions intensified after US forces—according to their statement acting in self-defense—carried out strikes in southern Iran against missile launch positions and naval units.

On the corporate front, AkzoNobel’s share price saw a significant surge, rising nearly 19.5% after the company rejected a joint takeover bid from Nippon Paint and Sherwin-Williams, and reiterated its support for a planned merger with Axalta. The automotive sector also delivered strong performance, supported by expanding new car sales in the EU: new passenger car registrations rose 5.1% year-on-year in April, marking the third consecutive monthly increase, although moderating from March’s 12.5%. Growth continues to be driven by strong demand for electric and other electrified vehicles, further reinforced by tax incentives and subsidy schemes across major European markets. The share of fully electric cars climbed to 19.7% of total sales in the first four months of the year, up from 15.3% a year earlier. The four largest markets showed a mixed picture: sales increased in Germany (+2.7%), Italy (+11.6%), and Spain (+8.4%), while France recorded a slight 0.3% decline. Overall, the EU new car market grew by 4.2% in the first four months of the year despite ongoing geopolitical tensions.

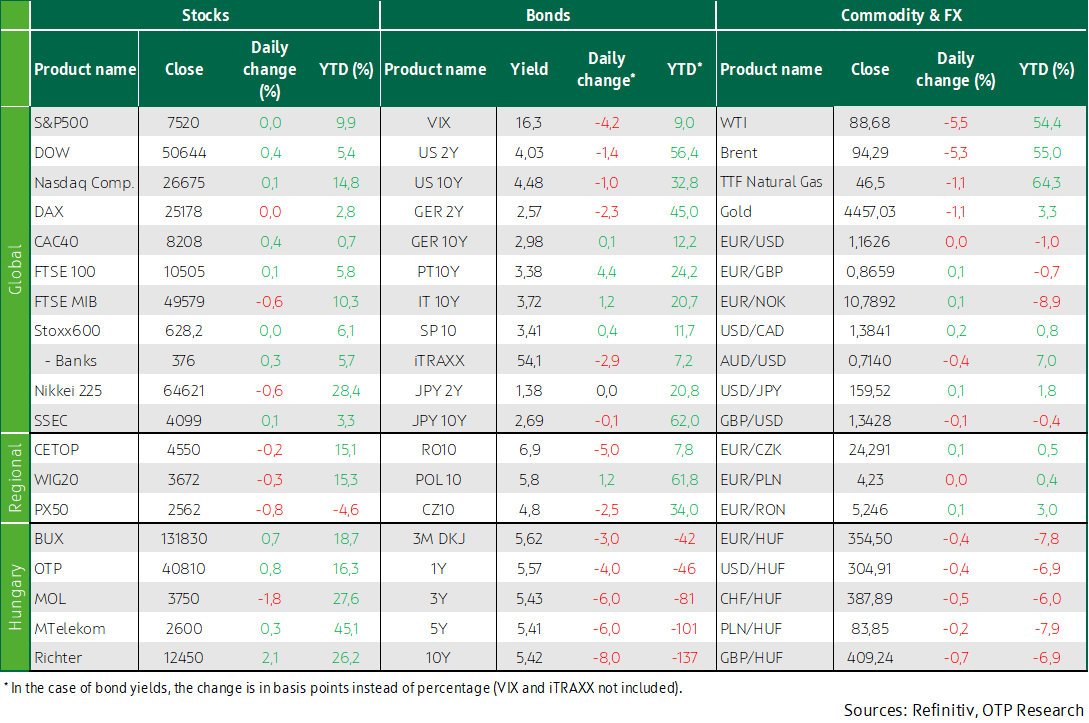

Regional indices declined yesterday, with the exception of the BUX: among domestic blue chips, only MOL shares fell, while the other three stocks moved higher.

US indices mostly moved higher; Tuesday’s momentum in semiconductor stocks eased somewhat; Meta shares rose

US equity markets mostly moved higher on Wednesday with modest moves, as momentum in semiconductor stocks eased. The Dow Jones was supported by a notable decline in oil prices, following reports from Iranian state media that the country is committed to a swift restoration of commercial traffic through the Strait of Hormuz. However, the White House dismissed the report as unfounded.

Within the technology sector, semiconductor manufacturers delivered mixed performance. Micron shares—following Tuesday’s more than 19% surge—closed with a more moderate gain of around 3.6%, while Intel and Qualcomm declined by 1.4% and 6.2%, respectively. In recent periods, memory chipmakers have become key beneficiaries of rising demand for artificial intelligence, although some market participants have pointed to stretched valuations and risks stemming from the sector’s cyclical nature. JPMorgan shares fell 2.4% after the CEO signaled that the bank could spend up to $20 billion on acquisitions in the coming years. Meta shares rose 3.7% following reports that the company plans to introduce subscription-based services across its Meta AI chatbot as well as Facebook, Instagram, and WhatsApp.

Developed market long-term yields barely moved, while Hungarian yields declined; regional FX markets lacked a clear direction

Despite conflicting reports on peace talks between Iran and the US, confidence in global capital markets strengthened further regarding a swift agreement. Oil prices declined by an additional 5%, with Brent crude falling to around $94 per barrel. No significant macroeconomic data were released. Bond and FX markets in developed economies reacted only modestly, with yields barely moving; the 10-year US Treasury yield closed at 4.5%, while the German equivalent ended below 3%. The EURUSD pair also showed little change from Tuesday’s 1.163 level.

There was no clear direction in regional FX markets yesterday: the Czech koruna weakened, the zloty traded sideways, while the forint strengthened to around 354.5 against the euro. In bond markets, the communication from the MNB’s rate-setting meeting—released after Tuesday’s benchmark fixing—triggered a decline in yields, with the segment of the curve beyond one year falling by 5–10 basis points, effectively flattening around the 5.4% level in the government bond market.

Today, the Government Debt Management Agency (ÁKK) will offer 3-, 5-, and 10-year fixed-rate bonds at auctions, with announced volumes of HUF 20bn, HUF 20bn, and HUF 25bn, respectively.

Today's highlights

Asian indices were in decline this morning, while oil prices rose again after US forces once more struck targets in Iran deemed to threaten their security, prompting Iran to retaliate by targeting US air bases.

Today, the European Commission will release its economic sentiment index, alongside the minutes of the ECB’s latest rate-setting meeting. In the US, CPI, GDP, housing data, as well as household consumption and income figures will be published, along with durable goods orders and the usual Thursday initial jobless claims. Hungary will release unemployment data.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more